Surprisingly, nearly 20% of teens hold credit cards before they reach adulthood, according to recent studies. This statistic raises important questions about financial literacy and the responsibilities tied to credit card usage. How can parents ensure their teens are prepared for this financial milestone?

Credit cards for teens are not merely modern conveniences but instruments of lasting financial education. Originally designed to help young adults build credit, these cards now also serve as critical tools for teaching fiscal responsibility. With proper guidance, teens can leverage credit cards to learn budgeting, the impact of interest rates, and the benefits of timely payments.

The Role of Credit Cards in Financial Literacy

Credit cards can be powerful educational tools for teens. They offer an opportunity to learn how to manage money and understand debt. Early exposure to credit card use can set the foundation for responsible financial habits.

Understanding how credit cards work teaches teens the value of budgeting. It also helps them grasp the implications of spending and borrowing. They learn about interest rates and how to avoid unnecessary debt.

Today’s teens often lack financial literacy, which can lead to poor money management in adulthood. Credit cards, when used correctly, can address this gap. They serve as real-life lessons in managing finances efficiently.

Parents play a crucial role in guiding their children’s credit card use. They can set spending limits and monitor transactions. This oversight ensures that teens learn to use credit cards safely and responsibly.

Responsibility Tied to Credit Cards

Credit cards come with great responsibilities that teens must learn. They need to understand the repercussions of overspending. Failure to manage credit properly can lead to significant debt and financial strain.

The Importance of Financial Responsibility

Teens should learn that credit cards are not free money. Every dollar spent needs to be repaid, often with interest. Understanding this helps them develop a sense of financial responsibility.

Financial responsibility also involves making timely payments. Delays can affect their credit scores, impacting future borrowing. Teaching teens to prioritize payments is crucial.

Moreover, responsible credit use can build a positive credit history. This benefits teens when they apply for loans in the future. Good credit opens doors to better financial opportunities.

Danger of Credit Card Debt

Accumulating debt is a significant risk tied to credit card misuse. Teens may not realize how quickly small purchases add up. Providing clear examples can illustrate this danger effectively.

Credit card debt often comes with high-interest rates. These rates can make repaying the debt challenging. Explaining interest rates helps teens understand the real cost of borrowing.

High debt can also lead to stress and financial insecurity. It’s vital to teach teens the importance of staying within their budget. Repeated overspending can lead to a cycle of debt that’s hard to break.

Strategies for Promoting Responsible Credit Card Use

Parents can set spending limits to guide responsible use. This helps teens understand the boundaries of their financial freedom. Monitoring transactions also provides an opportunity to discuss spending habits.

Using credit cards for specific purposes, like emergencies, is another strategy. This teaches teens to differentiate between needs and wants. Encouraging saving for large purchases can foster better financial planning.

Involving teens in monthly budget meetings can also be beneficial. They can see firsthand how their spending fits into the family’s financial health. This practical experience is invaluable for learning money management.

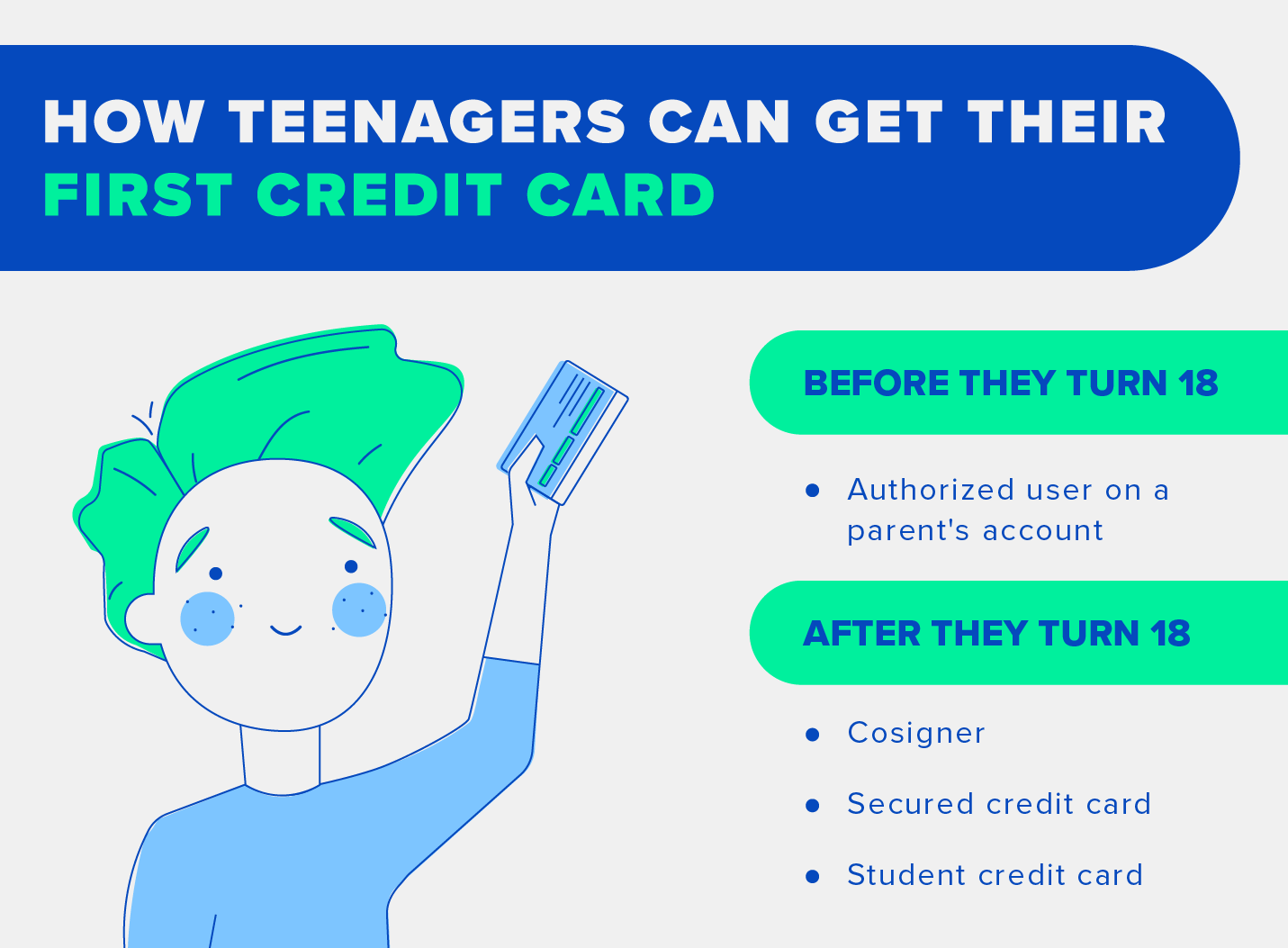

Prepaid vs. Secured Credit Cards: What’s the Difference?

Prepaid and secured credit cards are both designed to help manage and build credit, but they operate differently. A prepaid card requires users to load money onto the card before using it. This means spending is limited to the amount available on the card.

In contrast, a secured credit card requires a cash deposit upfront. This deposit acts as collateral and determines the credit limit. The card functions like a regular credit card, but the deposit secures payment.

Using a prepaid card won’t impact credit scores since no credit is extended. It’s more like a debit card and doesn’t report to credit agencies. This makes it a safer but less impactful choice for building credit.

Secured credit cards, on the other hand, report payment history to credit bureaus. This can help users build or improve their credit scores. Timely payments on a secured card can lay the groundwork for upgrading to a regular credit card.

How can Parents Monitor their Teen’s Credit Card Usage?

Monitoring your teen’s credit card usage is essential for preventing financial mistakes. Parents can start by setting up alerts for transactions. This way, they receive real-time notifications on their teen’s spending.

Many credit card companies offer online account management tools. These tools allow parents to review detailed statements. Parents can easily track where and how much their teen is spending.

Another useful feature is setting spending limits. Many cards let parents set thresholds to prevent overspending. This helps teens learn to manage within a budget.

Monthly budget meetings can also be highly effective. During these meetings, parents can go over the credit card statement with their teen. This open dialog fosters understanding and promotes financial education.

Using financial apps tailored for family use adds another layer of control. These apps often come with features to monitor and limit spending. They make tracking finances easy and accessible for both parents and teens.

Parental involvement in credit card use helps build trust. It teaches teens the importance of fiscal responsibility. Monitoring ensures that teens make smart financial choices while learning valuable life skills.

Teaching Teenagers About Interest Rates and Credit Scores

Interest rates are a crucial concept for teenagers to grasp. When teens understand how interest works, they can see how it affects what they owe. Interest can quickly increase the amount that needs to be paid back.

Parents can explain interest rates by using simple, relatable examples. For instance, comparing the cost of borrowing $100 at different interest rates. This helps teens visualize how interest accumulates over time.

Credit scores are another vital topic. A credit score reflects how well someone manages their debt. Maintaining a good credit score opens doors to better financial opportunities.

- Paying bills on time improves credit scores.

- Keeping credit card balances low is essential.

- Avoiding too many new credit inquiries helps as well.

Understanding credit scores can prevent future financial troubles. Teach teens that a low score can lead to higher interest rates on loans. This means paying more money over time.

Using online credit score simulators can be an engaging way to show how different actions affect scores. These tools allow teens to see the direct impact of their financial decisions. Practical tools make the learning process interactive and meaningful.

Things to Consider Before Giving Teens a Credit Card

There are several factors to weigh before giving your teen a credit card. First, assess their level of financial responsibility. Are they good at managing their allowance or saving money?

Legal considerations also come into play. Some credit cards have age restrictions. Ensure your teen meets the minimum age requirement before applying.

Understanding the purpose of the credit card is crucial. Is it for emergencies only, or to help them build credit? Clear guidelines can help avoid future misunderstandings.

- Discussing spending limits upfront is essential.

- Explain the importance of timely payments to avoid interest.

- Make sure they understand the impact on their credit score.

Another useful approach is starting with a secured or prepaid card. These options limit the risk while still teaching valuable lessons. They provide a controlled environment for learning about credit.

Consider setting up a monitoring system. Tools that allow you to track spending and set alerts can be very helpful. This will enable you to step in and offer guidance when needed.

Practical Ways to Teach Teens About Credit Cards

Teaching teens about credit cards can be done through practical methods. Start with real-life examples that they can relate to. Show them how buying something on credit results in additional costs due to interest.

Hands-on experience is invaluable. Consider giving them a low-limit, secured credit card. This allows them to practice managing expenses within a safe limit.

- Set specific goals like paying off small monthly balances.

- Review the statements together to discuss spending habits.

- Praise responsible behavior to reinforce positive actions.

Discuss the importance of timely payments regularly. Explain how missing payments can affect credit scores and lead to penalties. These discussions should be part of an ongoing conversation about financial health.

Create simulated scenarios where they have to make purchasing decisions. Make use of online games or apps that teach financial literacy in an engaging way. This makes learning fun and memorable for teens.

Encourage open communication about finances at home. Sharing your own experiences, both good and bad, can offer invaluable lessons. Teaching by example often has a lasting impact on teens’ understanding of credit.

Guide to Finding the Best Credit Cards for Teens

Finding the best credit card for your teen involves several considerations. First, look at cards with no annual fees. This makes it easier to manage costs while they learn.

Another key feature is a low-interest rate. Cards that offer lower rates can help minimize the cost of carrying a balance. This is especially important if your teen is just learning how to manage credit.

- Consider cards with rewards programs.

- Look for cards that offer cashback on everyday purchases.

- Rewards can encourage smart spending habits.

It’s also important to choose a card that reports to the credit bureaus. This helps your teen build a credit history. Building good credit early on sets them up for future financial success.

Secure credit cards are another excellent option. These require a deposit upfront, which helps limit spending. It’s a safer way to teach credit management.

Read reviews and compare different card options before making a decision. Many websites offer side-by-side comparisons to help you choose. Ultimately, the best credit card for your teen should suit their unique needs and financial responsibility level.

Frequently Asked Questions

Managing credit cards for teens comes with many questions. Here are answers to some common concerns parents may have about their teen’s credit card use.

1. What is the best type of credit card for a teenager?

The best type of credit card for a teenager is often a secured credit card or a prepaid card. Both options limit spending and help teach financial discipline without significant risk.

A secured credit card requires an upfront deposit that acts as collateral, making it safer for young users. Prepaid cards work like debit cards but still offer valuable lessons in budgeting and spending.

2. How can I monitor my teen’s credit card usage?

You can monitor your teen’s credit card usage by using online account management tools and setting up transaction alerts. These features allow you to track spending in real-time and ensure they stay within set limits.

Monthly reviews of the statements together can also foster open conversations about responsible spending habits. This helps your teen understand areas where they might need to improve or stay vigilant.

3. Why is it important for teens to learn about interest rates?

Learning about interest rates is crucial because it teaches teens the cost of borrowing money. Understanding how interest affects overall debt helps them make more informed financial decisions.

Teens who grasp the concept of interest rates are less likely to accumulate costly debt. They’ll realize the importance of timely payments and avoiding high-interest loans, which can protect their financial future.

4. Can using a credit card help my teen build their credit score?

Yes, using a credit card responsibly can help your teen build a positive credit score. Regular, on-time payments are reported to credit bureaus and contribute positively to their credit history.

This early start in building good credit will benefit them later when applying for car loans or renting an apartment. It sets them up for better financial opportunities as adults.

5. What should I consider before giving my teenager a credit card?

You should assess your teen’s maturity level and financial responsibility before giving them a credit card. Evaluate if they understand basic money management principles like saving, budgeting, and not overspending.

You’ll also want to consider starting with lower-risk options like secured or prepaid cards first. Setting clear rules and guidelines will help ensure they use the card wisely while learning effective money management skills.

Conclusion

Providing teens with credit cards, when done thoughtfully, can be a powerful tool in teaching financial responsibility. By starting with options like secured or prepaid cards, parents can guide their children through the intricacies of money management. Regular monitoring and open discussions about spending habits are essential for success.

Ultimately, the goal is to equip teens with the knowledge and skills needed for responsible financial behavior. Understanding interest rates, staying within spending limits, and making timely payments are critical lessons. With proper guidance, teens can build a solid foundation for their financial future.