Canceling a credit card might seem like a minor decision, but it can significantly impact your credit score. For instance, did you know that even closing one credit card could affect your credit utilization ratio? It’s essential to approach this process with strategic steps to minimize any potential financial drawbacks.

One significant aspect to remember is to clear all outstanding balances before proceeding. According to a recent study, nearly 25% of individuals face issues with unpaid balances when closing their accounts. Additionally, it’s crucial to notify the card issuer and follow up to ensure the account is officially closed. This careful approach helps maintain your credit health and mitigates any adverse impact.

- Check your balance and ensure it is paid off.

- Redeem any remaining rewards points.

- Contact your card issuer to inform them of your decision.

- Get a confirmation of the account closure in writing.

- Monitor your credit report to ensure proper reporting.

Understanding the Implications of Canceling a Credit Card

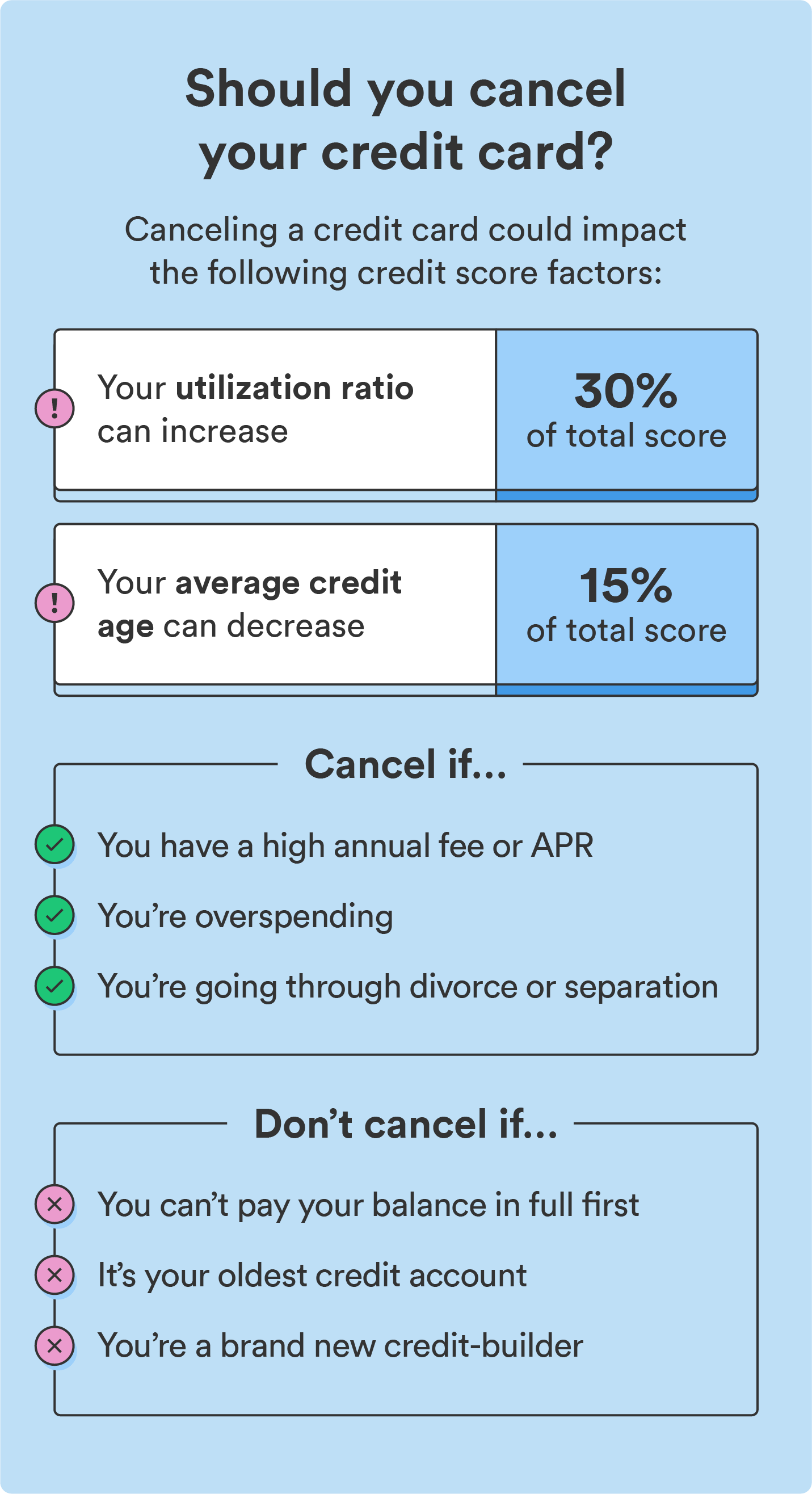

Canceling a credit card can significantly impact your financial health. One major effect is on your credit score, which might take a hit. This happens because you will have less available credit, which can increase your credit utilization ratio.

The Impact on Your Credit Score

Your credit score is an important metric that lenders use to evaluate your creditworthiness. Canceling a credit card reduces your total available credit. This makes your credit utilization ratio go up, negatively affecting your score.

Keeping your credit utilization below 30% is advisable. So, if you cancel a card, make sure your remaining cards are managed well. Maintaining low balances can help mitigate any adverse effects.

Also, remember that the length of your credit history matters. Old credit cards that have been in good standing contribute positively to your credit score. Canceling these can lower your average account age.

The Effect on Your Credit Utilization

Credit utilization ratio is the amount of credit you’re using compared to your total credit limit. A higher ratio suggests higher risk to lenders. Canceling a card reduces your total credit limit, which can increase this ratio.

For instance, if you have $10,000 total credit and use $3,000, your utilization is 30%. Canceling a card with a $5,000 limit would make your utilization 60% if your spending stays the same. This sharp increase can negatively impact your credit score.

Always monitor your credit reports to understand how cancellation affects you. Using credit wisely helps maintain a good score, even if you cancel a card.

Potential for Increased Interest Rates

Aside from affecting your credit score, canceling a card might lead to higher interest rates on other loans. Lenders often see higher utilization as increased financial risk. Consequently, they may offer loans or credit at higher interest rates to mitigate their risk.

If you’re planning to cancel a card, think about your future borrowing needs. A healthy credit score can get you better loan terms and lower rates. Therefore, managing your credit use effectively before and after cancellation is crucial.

Finally, your relationship with card issuers matters. Regularly updating them ensures they report accurate information to credit bureaus. This practice helps you maintain your credit health in the long run.

Pre-Cancellation Steps

Before canceling your credit card, it’s essential to take a few important steps. These steps can help you minimize the negative impact on your credit score. Proper planning ensures a smoother transition.

Checking Your Credit Card Balance

Always check your credit card balance before proceeding with cancellation. Make sure to pay off any remaining balances. This avoids complications and keeps your credit record clear.

Leaving an unpaid balance can lead to additional interest rates. Not to mention, it can affect your credit score negatively. So, ensure the account is fully settled.

Look out for any recent charges or payments not yet processed. These need your attention before you can close the card. Keeping a record of your final transaction helps in this regard.

Redeeming Any Remaining Points or Benefits

If you have accumulated rewards points, use them before canceling. Most credit card issuers will not allow you to redeem points after the account is closed. Take full advantage of the benefits you’ve earned.

Some cards offer cash back, travel points, or merchandise. Check your rewards balance to see what you can use. This is a good way to maximize your benefits before saying goodbye to the card.

If you’re unsure how to redeem these points, contact your card issuer. They can provide guidance on the best redemption options. Don’t lose out on rewards you’ve worked hard to earn.

Clearing All Pending Charges

Ensuring no pending charges exist is crucial before canceling. Sometimes purchases or automatic payments might take a few days to post. Wait until all transactions are fully processed.

If you cancel with pending charges, you might still owe money. This can complicate the cancellation process. Keeping an eye on your account activity helps avoid this scenario.

Cancel or transfer any recurring payments tied to the card. Doing this ahead of time ensures you won’t miss important obligations. This step streamlines the transition to a new card if needed.

Important Do’s and Don’ts of Canceling a Credit Card

When canceling a credit card, there are key actions you should take. Do make sure to notify your card issuer and get confirmation of the cancellation. This step is crucial to ensure the account is officially closed.

It’s important to verify that the final balance is zero before proceeding. Don’t leave any unpaid balances on the card. Unpaid balances can still accrue interest and fees, complicating the process.

Another important consideration is checking your credit report. Do review your credit report after the card is canceled to ensure everything is reported correctly. This helps you address any inaccuracies that may arise.

Avoid canceling multiple cards at once. Don’t close several accounts simultaneously as this can significantly impact your credit score. Take a slow and thoughtful approach to avoid financial hiccups.

How to Cancel a Credit Card: A Step-by-Step Guide

Canceling a credit card involves a few straightforward steps. Taking these steps helps ensure the process is smooth and without negative effects. Here’s a guide to assist you.

Step 1: Review Your Account

Start by checking your current balance and transactions. Make sure there are no pending charges or automatic payments. Clearing these first avoids any complications down the line.

Step 2: Pay Off Balances

Ensure the full remaining balance is paid off. Leaving unpaid balances can result in additional fees. Once the balance is zero, you’re ready to proceed to the next step.

Step 3: Contact Your Card Issuer

Call the customer service number on your credit card. Inform them that you wish to cancel the card. They may ask you to confirm details for security purposes.

- Be polite and clear about your request.

- Ask for a confirmation number or email.

- Verify that the account is marked closed.

Step 4: Double-Check Your Credit Report

After canceling, check your credit report to ensure the account is reported as closed. Reviewing your credit report helps catch any errors. This step ensures your records are accurate.

Following these steps helps protect and maintain your financial health. Properly canceling your credit card minimizes risks and keeps your credit profile in good standing. Always keep a copy of any communications for your records.

The Role of Credit Bureaus in Credit Card Cancellation

Credit bureaus play a crucial role when you cancel a credit card. They are responsible for updating your credit report. Proper reporting ensures your credit history reflects the closed account accurately.

What Credit Bureaus Do

When you cancel a credit card, the card issuer informs the credit bureaus. This information is then recorded on your credit report. It’s essential for your credit report to show the account as “closed by consumer.”

- Equifax

- Experian

- TransUnion

Each bureau will update their records based on the information received from the card issuer. This helps in maintaining consistency across all your credit reports. Monitoring these updates can help identify any discrepancies quickly.

Ensuring Accurate Reporting

Once you cancel your card, double-check your credit report. Make sure it reflects the change accurately. Errors can impact your credit score negatively.

If you find any mistakes, contact the credit bureaus to dispute them. Use the confirmation number from the card issuer to support your claim. Correcting errors ensures your credit profile remains strong.

How This Affects Your Credit Score

Credit bureaus use the updated information to calculate your credit score. Canceling a credit card can affect your score, particularly your credit utilization ratio. Keeping an eye on your credit report helps you manage any changes effectively.

Regularly reviewing your credit report is a good practice. This helps you stay on top of any changes and ensures accurate reflection of your financial activities. Maintaining a clean credit profile is essential for future financial endeavors.

Post-Cancellation Tips

After canceling your credit card, it’s crucial to monitor your credit report. Ensure the account shows as “closed by consumer.” Regularly checking helps spot any errors or issues early.

Maintain a low credit utilization ratio by managing your remaining cards wisely. A low ratio positively impacts your credit score. Avoid maxing out your other cards.

Set up a budget to stay on top of your finances. This helps in managing your spending and ensures you don’t rely too much on other cards. Budgeting can lead to healthier financial habits.

- Track your expenses

- Set savings goals

- Avoid new debt

Consider your future credit needs carefully. Having good credit is essential for loans and mortgages. Active financial management keeps your credit profile in good health.

Finally, keep all documentation related to the cancellation. This includes confirmation numbers and any correspondence with your card issuer. Such records are useful in case of any disputes or discrepancies.

Alternatives to Canceling a Credit Card

If you’re considering canceling your credit card, explore other options first. One alternative is to downgrade your card. Many issuers offer no-annual-fee versions of their cards.

- Downgrade instead of canceling.

- No-annual-fee alternatives.

- Keep the account active.

Another option is to request a lower interest rate. If high-interest rates are a problem, contact your bank. Many issuers may reduce your rate if you have a good payment history.

If you’re overwhelmed by debt, consider a balance transfer. Transferring your balance to a card with lower interest can help save money on interest charges. This allows you more time to pay off the debt at reduced rates.

Temporarily freezing the account is another possible route. Some banks allow you to suspend an account for short periods without closing it entirely. This can be useful if you need a break from spending but don’t want to lose the credit history tied to the card.

Cancelling is not always necessary when there are alternative solutions available. Explore these options before deciding, as they might better suit your financial needs while keeping your credit score intact.

Consulting a Credit Advisor

When considering canceling a credit card, consulting a credit advisor can be beneficial. Credit advisors offer expert guidance on how to manage your credit effectively. They can help you understand the implications and plan accordingly.

An advisor will assess your financial situation. They look at your credit score, debt, and spending habits. This analysis allows them to provide personalized advice that suits your needs.

- Evaluate your financial health

- Offer customized strategies

- Provide long-term credit planning

Advisors can also help you identify alternatives to canceling your card. They may suggest options like balance transfers or lowering your interest rate. These alternatives often come with fewer risks to your credit score.

If you decide to proceed with cancellation, an advisor helps you navigate the process. They ensure you take all necessary steps to minimize negative effects. Their support leads to better financial outcomes.

Finally, advisors serve as a resource for ongoing credit management. They offer tips and strategies to help maintain a good credit score. Consulting a credit advisor can be a smart move for anyone looking to make informed financial decisions.

Frequently Asked Questions

Canceling a credit card involves several steps and considerations. Below are some common questions and answers to help you understand the process better.

1. What are the potential impacts of canceling a credit card on my credit score?

Canceling a credit card can affect your credit utilization ratio, which measures how much of your available credit you’re using. A higher ratio can negatively impact your score. Additionally, it might lower the average age of your accounts, another factor in calculating your score.

Experts recommend monitoring these changes closely to manage their effects properly. Maintaining low balances on other cards helps minimize any negative impacts on your overall financial health.

2. Should I pay off my balance before canceling my credit card?

Absolutely, paying off any remaining balance is a crucial step before canceling your card. Unpaid balances can accumulate interest and fees, complicating the closure process and potentially damaging your credit score.

Ensure all pending charges are cleared as well. This will make sure there are no lingering issues after the cancellation, allowing for an easier and cleaner closure of the account.

3. How do I ensure my rewards points don’t go to waste when I cancel my card?

You should redeem all accumulated rewards points before closing your account. Most card issuers won’t allow point redemptions after the cancellation is complete, so it’s best to use them up while you still can.

If you’re unsure how to redeem them, check with your issuer for various redemption options like cash back or travel points. This way, you make full use of all benefits earned from having the card.

4. Can I downgrade my credit card instead of canceling it?

Yes, many issuers offer lower-fee versions of their cards that you can downgrade to instead of canceling outright. This allows you to maintain the account’s history while avoiding high annual fees associated with premium cards.

This option helps keep your total available credit high, benefiting your credit utilization ratio and overall score positively. Contact your issuer to explore this more manageable alternative.

5. Is there any paperwork involved in canceling a credit card?

Although most cancellations start with a phone call or online request, some issuers may require written confirmation or additional forms for official closure procedures. Make sure to ask if such documentation is needed when contacting customer service.

This added step ensures there’s no miscommunication between you and the issuer about closing the account safely and properly documented in their records and yours as well.

Conclusion

Canceling a credit card requires careful planning and strategic steps to minimize negative impacts. From reviewing your account balance to notifying your card issuer, every step ensures a smooth process. Being informed helps you protect your credit score.

Exploring alternatives like downgrading your card or consulting a credit advisor can provide valuable insights and options. With thorough preparation and the right approach, you can safely navigate the complexities of canceling a credit card. This process helps maintain your financial well-being.