Credit card debt can feel like a never-ending cycle, with the average American household carrying a balance of over $6,000. This financial burden can be overwhelming, leading to stress and potentially damaging one’s credit score. Breaking free from this cycle requires both determination and a strategic plan.

Historically, credit card debt has plagued many, but there are effective ways to manage and eliminate it. One significant approach is adhering to the snowball method, where you pay off smaller balances first to build momentum. Statistically, individuals who use this method are more likely to stay debt-free in the long term.

Recognizing the Signs of Growing Credit Card Debt

Changes in Spending Behavior

One of the first signs of growing credit card debt is subtle changes in your spending habits. You might start using credit for everyday purchases that you used to pay for with cash. This shift can easily go unnoticed but has a significant impact over time.

If you’re unsure whether your behavior has changed, look at your monthly credit card statements. Are you carrying a balance month to month? Increased reliance on credit could be a red flag.

Difficulty Meeting Minimum Payments

Struggling to meet only the minimum payment each month is another warning sign. Meeting minimum payments without making a dent in the principal balance can lead to a never-ending debt cycle. This habit can quickly increase your total debt due to interest charges.

Reviewing your payment history can help. If you’re consistently paying just the minimum, it might be time to reassess your financial situation.

Increasing Credit Card Balances

Credit card balances steadily climbing over time is a clear sign of trouble. Maxing out your credit cards or consistently nearing the credit limit indicates poor debt management. High balances can severely impact your credit score.

Regularly check your credit report to monitor your balances. Keep your credit utilization ratio below 30% to maintain a healthy credit score.

Using Credit to Pay Off Debt

Using one credit card to pay off another indicates a cycle of debt. This practice not only increases overall debt but also leads to higher interest rates and fees. This approach can trap you in an endless debt loop.

Create a budget to track your spending and find ways to cut costs. Avoid this practice to prevent falling deeper into debt.

The Impact of Credit Card Debt on Your Life

Credit card debt can have far-reaching effects on various aspects of your life. From financial stress to personal relationships, the impact is often profound. Below are three major areas affected by growing credit card debt.

Financial Consequences

One of the immediate impacts of credit card debt is on your finances. High interest rates can make it hard to pay off balances, leading to more debt. This creates a cycle that’s difficult to escape.

The financial strain can also affect your ability to save for the future. With a large portion of income going to debt repayment, you might find it challenging to build an emergency fund or save for retirement.

Additionally, credit card debt can hurt your credit score. A lower score affects your ability to get loans and might lead to higher interest rates on future borrowing.

Emotional and Mental Health

Credit card debt doesn’t just take a toll on your wallet; it also impacts your emotional well-being. The constant worry about payments can lead to stress and anxiety. This can severely affect your mental health over time.

Many people experience guilt and shame related to their debt. These feelings can lead to social withdrawal and affect your relationships.

Moreover, the emotional burden of debt can also lower your overall quality of life. Constant stress can make it hard to enjoy daily activities and can even affect sleep.

Relationship Strain

Debt can also strain personal relationships. Financial problems are one of the leading causes of conflicts in relationships. Arguments about money can lead to misunderstandings and added stress.

Transparency and open communication about finances can become challenging. Partners might avoid discussing their debt, which can create further tension.

Finally, the pressures of debt can impact your family life. Limited financial resources might affect your ability to provide for your family, leading to further strain.

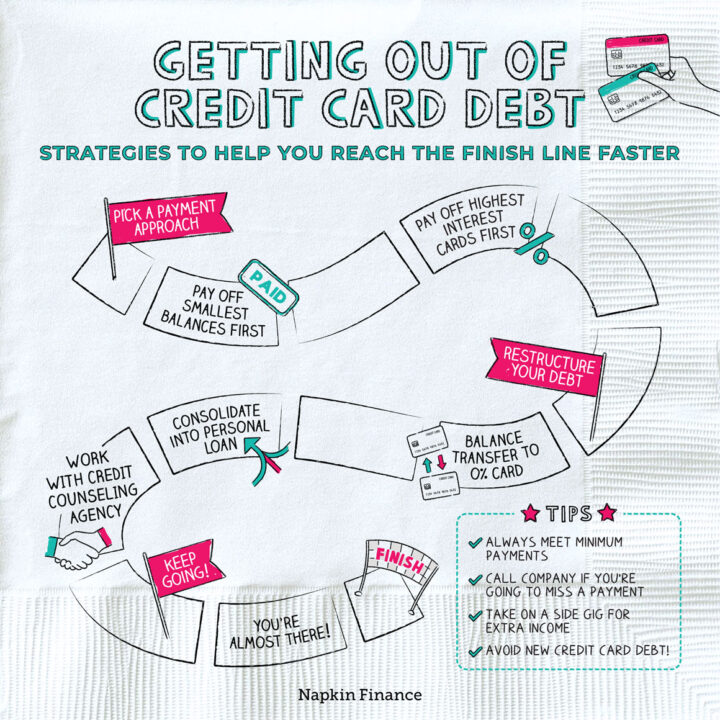

Strategies to Help You Get Out of Credit Card Debt

Breaking free from credit card debt requires a mix of determination and strategy. One effective approach is to create a strict budget. This helps you track your spending and find areas where you can cut back.

Another useful strategy is the Debt Snowball Method. Focus on paying off the smallest debt first while making minimum payments on other cards. This provides a sense of achievement and motivates you to keep going.

Consider the Debt Avalanche Method as well. Here, you tackle the debt with the highest interest rate first. This approach can save you money on interest in the long run.

Negotiating with your creditors can also be beneficial. Ask for lower interest rates or more manageable payment terms. This can make a huge difference in your ability to pay off your debt.

Implementing Debt Snowball Method

The Debt Snowball Method is a popular approach to tackling debt. It focuses on paying off your smallest debts first. This can give you a psychological boost and keep you motivated.

To start, list all your debts from smallest to largest. Make the minimum payments on all debts except the smallest one. Put any extra money toward the smallest debt until it’s paid off.

Once the smallest debt is paid, take the money you were using for it and apply it to the next smallest debt. This method creates a “snowball” effect, allowing you to gain momentum. As you eliminate each debt, you’ll have more money available for the next one.

- List debts from smallest to largest.

- Make minimum payments on all but the smallest debt.

- Use extra funds to pay off the smallest debt.

- Repeat until all debts are paid off.

This method works well for many people because it provides a series of small wins. These victories can keep you motivated to continue paying off your debts. It’s important to stay consistent and avoid adding new debt while using this method.

The Debt Snowball Method isn’t just about numbers; it’s about psychology. It helps you feel more in control of your finances. By celebrating small victories, you can stay committed to reaching your overall financial goals.

Implementing Debt Avalanche Method

The Debt Avalanche Method is another effective way to tackle credit card debt. Unlike the Debt Snowball Method, this strategy focuses on paying off debts with the highest interest rates first. This approach can save you more money in interest over time.

Start by listing all your debts and their respective interest rates. Make minimum payments on all your debts except the one with the highest interest rate. Put any extra funds toward that highest interest debt until it is paid off.

Once the highest interest debt is gone, move on to the next highest interest rate debt. By focusing on interest rates, you’ll reduce the amount of money you pay in the long term. This method helps to free up more of your budget for other financial goals.

- List debts by interest rate from highest to lowest.

- Make minimum payments on all debts except the highest interest rate debt.

- Allocate extra funds to the debt with the highest interest rate.

- Move to the next highest interest rate debt once the top one is paid off.

While this method might not offer the same quick psychological wins as the Snowball Method, it is often more financially efficient. You see faster progress in reducing overall debt because you minimize interest payments. The key is to stay disciplined and focused on the long-term benefits.

Choosing the Debt Avalanche Method requires patience and a clear understanding of your financial situation. It’s crucial to keep a close eye on your debts and stick to your repayment plan. This approach can lead to substantial savings and faster debt elimination.

Considering Debt Consolidation as a Solution

Debt consolidation involves combining multiple debts into a single, manageable loan. This helps simplify your monthly payments and can often result in a lower interest rate. This strategy can make it easier to stay on top of your debt repayment plan.

There are various types of debt consolidation loans, such as personal loans or balance transfer credit cards. Personal loans often provide a fixed interest rate and set repayment period. Balance transfer credit cards offer low or zero interest rates for a limited time.

- Personal loans

- Balance transfer credit cards

- Home equity loans

While debt consolidation can simplify your finances, it’s essential to use it wisely. Avoid accumulating new debt while paying off the consolidation loan. This will help you break the cycle of debt.

Before choosing a debt consolidation option, carefully compare the terms and conditions. Look for potential fees or early repayment penalties. It’s vital to ensure the new loan is advantageous.

Consult a financial advisor if you’re unsure which option to choose. They can help you evaluate your financial situation and select the best method. Professional advice can be invaluable in making the right decision.

Creating a Personalized Plan to Stay Out of Credit Card Debt

Staying out of credit card debt requires a personalized plan that suits your financial habits. Start by drawing up a comprehensive budget. This helps you track where your money goes every month and identify areas for savings.

Create categories for essential expenses like rent, groceries, and utilities. Set aside a portion for discretionary spending but keep it within limits. Save what you can from each paycheck to build an emergency fund.

- Rent/Mortgage

- Groceries

- Utilities

- Savings

- Entertainment

Automate your payments to minimize missed deadlines and late fees. Many banks and financial apps allow you to set up automatic transfers. This ensures timely payment, helping you maintain good credit.

Avoid impulse purchases by waiting 24 hours before buying non-essential items. This “cooling-off” period helps determine if the purchase is necessary. Over time, this habit can save significant amounts of money.

If possible, consider using cash for discretionary purchases. Swiping a card makes spending easier but also more deceptive. Using cash provides a tangible reminder of how much you’re spending.

Review your financial plan regularly to make adjustments as needed. Life changes such as job shifts or new expenses require updates to your budget. Staying flexible makes it easier to adapt and remain debt-free.

Maintaining Your Financial Stability and Health

Maintaining financial stability is key to staying out of credit card debt. One important step is to create and stick to a budget. A well-planned budget helps you manage your money wisely.

Setting financial goals is also crucial. These goals can be short-term like saving for a vacation, or long-term like building a retirement fund. Clear goals motivate you to stay on track.

- Short-term goals: Save for a vacation

- Medium-term goals: Pay off student loans

- Long-term goals: Build a retirement fund

Emergency funds act as a financial cushion during unexpected events. Aim to save at least three to six months’ worth of living expenses. This will help you avoid using credit cards for emergencies.

Regularly monitor your credit report to check for errors and stay aware of your credit status. Free online tools are available to help you monitor your credit score. Staying informed helps you maintain good financial health.

Seek professional advice if needed. Financial advisors can offer tips tailored to your specific situation. They provide valuable insights that can help you improve your financial stability.

Lastly, practice mindful spending. Consider needs versus wants before making a purchase. This habit will keep you from unnecessary spending and help maintain your financial health.

Frequently Asked Questions

If you’re looking to get out of credit card debt and stay out of it, you’re not alone. These frequently asked questions will help guide you through the process.

1. What is the Debt Snowball Method?

The Debt Snowball Method involves paying off your debts starting with the smallest balance first. After paying off the smallest debt, you then move on to the next smallest, gaining momentum and confidence along the way.

This method provides quick wins that can boost your motivation. It helps people stay committed to their debt repayment plan because they see regular progress.

2. How does debt consolidation work?

Debt consolidation involves combining multiple debts into one single loan, often with a lower interest rate. This makes it easier to manage your payments since you only have one payment date and amount to worry about.

You can consolidate debt using personal loans, balance transfer credit cards, or home equity options. It’s crucial to compare terms and understand any fees involved before choosing this route.

3. What are some common signs that my credit card debt is becoming unmanageable?

Common signs include only making minimum payments, using credit cards for everyday necessities, and having maxed-out cards. These behaviors indicate you’re struggling to pay down balances effectively.

Other signs include borrowing from one card to pay another or feeling stressed over finances regularly. Recognizing these signs early helps in taking proactive steps toward managing your debt better.

4. Are there any digital tools that can help me manage my debt?

There are several digital tools designed to assist with managing debt such as budgeting apps like Mint or YNAB (You Need a Budget). These apps help track spending habits and create personalized budgets that keep you on track.

Credit score monitoring services can also be beneficial in keeping an eye on changes in your financial health. Many banks offer free tools that show updated scores monthly or even weekly.

5. Can negotiating with creditors really make a difference?

Yes, negotiating with creditors can make a big difference in managing your debt more effectively. Creditors may lower interest rates or offer alternative payment plans if you explain your situation candidly.

This approach often reduces the overall cost of repayment and helps prevent accounts from going into default. It’s worth trying if you’re facing financial hardship and can’t meet existing payment terms.

Conclusion

Successfully exiting credit card debt and staying debt-free requires a mix of strategic planning and disciplined execution. Developing a budget, leveraging techniques like the Debt Snowball or Debt Avalanche methods, and considering debt consolidation are effective steps. Each strategy can be tailored to fit your unique financial situation.

Regularly monitoring your financial health, staying informed of your credit status, and seeking professional advice when needed are crucial. By implementing these actions consistently, you can manage your debt more efficiently and achieve long-term financial stability. Always remember, financial health is an ongoing journey.