Ever noticed how that seemingly small coffee purchase can snowball into a surprising chunk of your monthly expenses? Understanding the triggers behind such impulse buying behaviors is critical. By recognizing these habits, you can devise strategies to mitigate their impact and start saving money more effectively.

Historically, impulse buying has been a challenge many have faced, exacerbated by the convenience of online shopping. Research from the Financial Planning Association reveals that 64% of consumers make spontaneous purchases. Setting a strict budget, and sticking to a grocery list can be practical steps towards curbing these urges, keeping your finances in check.

- Track your spending to identify areas of improvement.

- Create a realistic budget and stick to it.

- Make a shopping list before you buy anything to avoid impulse purchases.

- Use cash instead of cards to keep spending in check.

- Set financial goals to stay motivated and focused on saving.

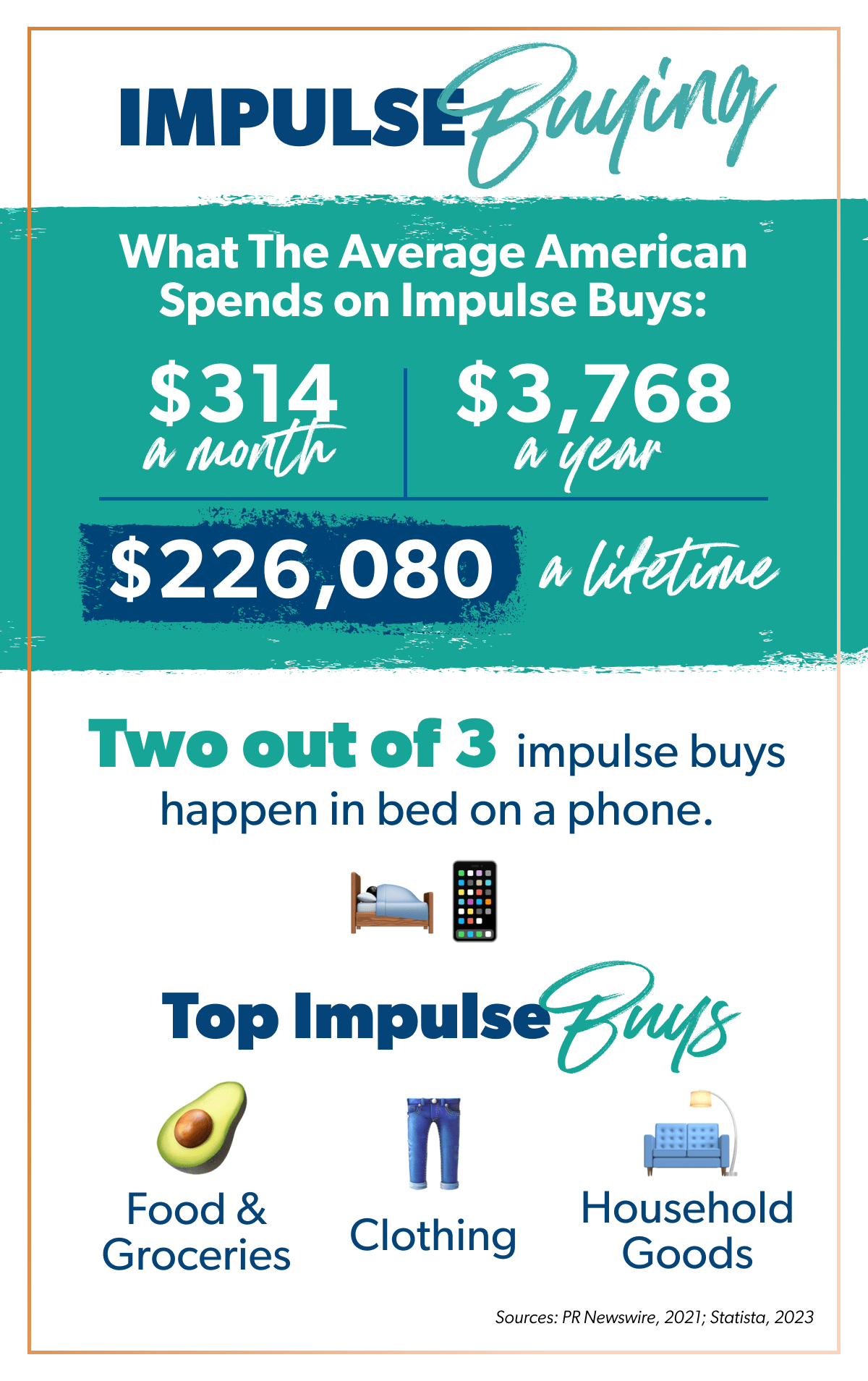

The Science Behind Impulse Buying

Psychological Triggers

Impulse buying often stems from emotional triggers such as stress or excitement. When feeling down, people tend to make purchases to boost their mood. Retailers understand this and create environments that encourage spontaneous purchases.

Store layouts are designed to attract your attention. For example, products at eye level or near checkout lanes draw you in. Understanding these tactics can help you make more conscious decisions.

The Role of Dopamine

Dopamine, a brain chemical, plays a significant role in impulse buying. When you see something new and exciting, your brain releases dopamine, making you crave the item. This chemical reaction can make it hard to resist buying immediately.

Recognizing this can give you control over your spending habits. Pause and reflect before making a purchase to combat this natural urge. Delayed gratification can be a powerful tool.

Influence of Marketing Tactics

Marketing tactics like limited-time offers and flash sales drive impulse buying. These methods create a sense of urgency, making you feel like you need to buy now or miss out. Retailers use vibrant colors and catchy slogans to grab your attention.

Being aware of these tactics can help you stay mindful. Always ask yourself if you really need the item or if you’re just caught up in the moment. Taking a moment to think can save you money.

Environmental Factors

Even your environment affects impulse buying. Bright lights and pleasant music in stores can make you feel more relaxed and open to buying. Online shopping also makes it easy with one-click purchases and targeted ads.

Consider creating an environment that discourages impulse buying. Unsubscribe from promotional emails and resist the urge to shop when feeling emotional. Small changes can lead to better spending habits.

Assessing Your Spending Habits

Understanding where your money goes is crucial for financial health. By assessing your spending habits, you can identify areas for improvement. It’s the first step towards better financial management.

Tracking Your Expenses

Start by keeping a daily log of all expenditures. This can be done manually or through budgeting apps. Monitoring your spending offers insights into how your money is used.

By categorizing expenses (e.g., groceries, entertainment), you can see where the bulk of your money goes. This step makes it easier to spot unnecessary spending. Consistent tracking helps in making informed decisions.

After a month, review your logs to identify patterns. Look for areas where you can cut back. This data-driven approach can be eye-opening.

Analyzing Monthly Statements

Review your bank and credit card statements regularly. These documents provide a clear picture of your spending habits. Identify recurring charges or subscriptions you may have forgotten.

Look for trends over several months. Check for erratic spending spikes and consider the reasons behind them. This helps in understanding seasonal or emotional spending.

Use this information to adjust your budget. Prioritize essential expenses and minimize non-essential ones. Continual assessment reinforces smarter spending.

Setting Financial Goals

Clearly defined financial goals motivate disciplined spending. Whether saving for a vacation or building an emergency fund, goals provide direction. Link your spending habits to these objectives.

Create a plan to allocate a certain portion of your income towards these goals. Track progress regularly to stay motivated. Achieving smaller milestones can inspire greater financial discipline.

If adjustments are needed, revise your spending and saving plans. Flexibility ensures you stay on track. Goals make the whole process more purposeful.

Crafting a Practical Budget

Building a practical budget is essential for financial stability. It helps you allocate money towards necessary expenses, savings, and wants. Creating a well-balanced budget enables you to live comfortably within your means.

Start by listing your income sources. Include your salary, bonuses, or any other earnings. Knowing your total income is the first step in setting up your budget.

Next, itemize your expenses. Break them down into categories like housing, food, transportation, and entertainment. This makes it easier to track spending and identify areas for adjustment.

Finally, compare your income to your expenses. If your expenses exceed your income, identify areas to cut back. A balanced budget ensures you can save while covering all necessary expenses.

Smart Shopping Strategies to Curb Impulse Buying

Creating a shopping list is one of the best strategies to avoid impulse buying. Before heading to the store, write down the items you truly need. Stick to this list to help you stay focused.

Avoiding shopping when you’re hungry can also prevent unnecessary purchases. Hunger can make everything look appealing, leading to impulsive buys. Eating beforehand keeps your mind clear and your decisions rational.

Taking a moment before checkout to review your cart is another good tactic. Ask yourself if you really need each item. This simple act can help you put back the things you don’t truly need.

Using cash instead of cards can limit overspending. When you physically see the money leaving your wallet, you’re more likely to think twice before making a purchase. This method can make your spending feel more real.

Another tip is to unsubscribe from retail emails and newsletters. These emails often include special deals that tempt you to buy things you don’t need. Reducing exposure to these offers helps you avoid unnecessary spending.

Plan your shopping trips and avoid window shopping. When you shop with a purpose, you’re less likely to make impulse purchases. Sticking to your plan can save you money and time.

The Role of an Emergency Fund

An emergency fund acts as a financial safety net. It provides quick access to cash during unforeseen situations like job loss or medical emergencies. This fund helps you manage unexpected expenses without falling into debt.

Saving three to six months’ worth of expenses is ideal for an emergency fund. This amount offers enough cushion to handle most financial setbacks. Start small if needed, then gradually build up your savings.

Keep your emergency fund in an easily accessible account. Consider using a high-yield savings account for this purpose. Easy access ensures you can quickly use the funds when required.

Replenish your emergency fund after using it. This ensures it’s always available for future needs. Make it a habit to contribute regularly, even if it’s a small amount.

Having an emergency fund provides a sense of financial security. It reduces stress during difficult times by covering surprise expenses. Peace of mind is one of the most valuable benefits of an emergency fund.

Using the fund solely for emergencies is crucial. Avoid tapping into it for non-essential purchases. This discipline helps maintain its purpose and ensures you stay financially stable.

Slashing Unnecessary Expenses

Reducing unnecessary expenses can significantly improve your financial health. Start by identifying non-essential purchases you make regularly. Small savings can add up quickly over time.

Consider cutting back on dining out. Cooking at home is usually cheaper and can be healthier. Planning your meals in advance helps you avoid last-minute takeout temptations.

Review your subscription services. Ask yourself if you truly use them or can live without them. Canceling unused subscriptions can free up extra funds each month.

Avoid impulsive online shopping. Remove saved payment information from retail websites. This extra step gives you time to reconsider your purchase before completing the transaction.

Look for free or low-cost entertainment options. Enjoy outdoor activities like hiking or visiting local parks. Streaming services often have free trials or lower-cost options you can take advantage of.

Always compare prices before making a purchase. Use price comparison websites or apps to find the best deals. Being a smart shopper can help you save significantly on everyday items.

Making Saving Money a Habit

Developing a habit of saving money starts with setting realistic goals. Whether it’s saving for a new gadget or a future vacation, having clear objectives makes the process easier. Goals give you something to look forward to and work towards.

Automate your savings if possible. Set up automatic transfers from your checking account to your savings account. This way, you save without even thinking about it.

Create a budget and stick to it. Track your income and expenses to identify how much you can save each month. A consistent approach helps in building long-term saving habits.

Celebrate small milestones along the way. Reward yourself when you achieve short-term goals like saving $100 or $500. This positive reinforcement keeps you motivated.

Avoid making impulsive purchases that derail your savings plan. Think twice before spending on non-essentials. Delay gratification by reminding yourself of your financial goals.

Review your progress regularly and make adjustments as needed. Life circumstances change, so adapt your saving strategies accordingly. Regular reviews ensure you’re always on track.

Seeking Professional Financial Guidance

Sometimes, managing money can feel overwhelming. Seeking help from a financial advisor can provide clarity. Experts offer valuable insights on how to save money and avoid impulse buying.

Financial advisors help you create a personalized financial plan. They assess your income, expenses, and goals to suggest tailored strategies. This ensures your plan is both realistic and achievable.

Consider asking about budgeting tips and investment opportunities. Advisors often have access to resources and tools that can optimize your financial health. Using these resources can accelerate your money-saving efforts.

Regularly consult with your advisor to track your progress. They can help adjust your plan as needed, ensuring you stay on course. Life changes, so should your financial strategies.

Professional guidance also provides accountability. Knowing you have someone to report to can motivate you to stick to your budget. Accountability boosts your commitment to saving and reducing unnecessary expenses.

Finding a reputable advisor is crucial. Look for certifications and positive reviews. Trustworthy advisors offer the peace of mind that your finances are in good hands.

Frequently Asked Questions

Here are some common questions about saving money and avoiding impulse buying. These answers provide practical tips and strategies to help you manage your finances better.

1. What is the best way to start a budget?

The best way to start a budget is by tracking your current spending. Before setting limits, understand where your money goes. This helps identify areas for adjustments.

Next, categorize your expenses such as housing, groceries, and entertainment. Set realistic limits based on past spending and income. Regularly review and modify your budget to ensure it stays effective.

2. How can I curb my impulse purchases online?

Curbing online impulse purchases can be challenging but manageable with discipline. Remove saved payment methods from accounts, creating an extra step before buying.

Also, use browser extensions that block certain shopping sites during specific times. Consider waiting 24 hours before making a purchase decision. This delay often reduces the urge to buy impulsively.

3. Why is it important to have an emergency fund?

An emergency fund provides financial security during unexpected events like medical emergencies or job loss. It helps you avoid relying on credit cards or loans.

Aim to save three to six months’ worth of living expenses in an easily accessible account. Having this buffer reduces stress, knowing you’re prepared for sudden costs.

4. What tools can help me track my spending effectively?

Several tools can help track spending effectively, from traditional pen-and-paper methods to modern apps. Budgeting apps like Mint or YNAB offer automated tracking and categorization of expenses.

You can also use spreadsheets for a more customized approach if tech isn’t your thing. Regardless of method, consistent tracking is key to understanding and controlling spending habits.

5. How do financial goals influence saving habits?

Financial goals act as motivating targets that guide your saving habits over time. Goals like buying a house or retiring early give purpose to your savings efforts.

Create both short-term and long-term goals for balanced motivation. Regularly revisit these goals to adjust contributions as needed, keeping you focused and committed on saving regularly.

Conclusion

Incorporating strategies to save money and avoid impulse buying isn’t just wise; it’s essential for long-term financial health. By tracking your expenses and creating a realistic budget, you set a strong foundation for better money management. These steps can significantly improve your financial stability and peace of mind.

Additionally, utilizing smart shopping strategies and building an emergency fund can safeguard against unexpected expenses. Seeking professional financial guidance when needed ensures you stay on the right path. Taking these proactive measures will help you achieve your financial goals more effectively.