Consider this: nearly 78% of adults live paycheck to paycheck, highlighting a significant gap in financial literacy even among well-educated individuals. How did we get here, when financial tools and resources are more accessible than ever? The answer may lie in insufficient emphasis on practical financial training in personal finance management.

The evolution of financial training dates back to the early 20th century when formal education barely touched on money management skills. Today, though we have made strides, a staggering gap still exists, as evidenced by numerous studies showing only 24% of millennials demonstrate basic financial literacy. Effective financial training programs not only provide knowledge but also instill confidence and discipline, essential for managing personal finances effectively.

Exploring the Importance of Financial Training

Financial training is a crucial skill for navigating today’s complex economic landscape. Understanding how to manage money effectively can lead to better financial stability and peace of mind. Moreover, it helps individuals make informed decisions that affect their financial health.

Without proper financial training, many people struggle to save money and manage debt. This often leads to living paycheck to paycheck, which can be stressful and limiting. Financial literacy programs can dramatically change this scenario.

One of the biggest benefits of financial training is the ability to create and stick to a budget. A well-planned budget allows people to track their income and expenses, helping them prioritize their spending. Budgeting is a fundamental step towards achieving financial goals.

Financial training also educates people about investing and saving for the future. Learning about different types of investments can help build wealth over time. Knowledge about retirement plans ensures a comfortable and secure future.

Current State of Financial Literacy

Financial literacy is alarmingly low among adults worldwide, with many lacking basic money management skills. A study showed that only 24% of millennials are financially literate. This gap highlights the urgent need for financial education.

Many schools and universities do not prioritize teaching personal finance. This leaves young adults unprepared to handle real-world financial responsibilities. Integrating financial training into the education system can bridge this gap.

Online platforms and community programs have started offering courses to improve financial literacy. These resources aim to educate individuals about budgeting, saving, and investing. Making use of these tools can lead to better financial decision-making throughout life.

The Gap in Personal Finance Management

Many people lack the skills to manage their personal finances effectively. This can lead to unnecessary debt and financial stress. The gap exists because of insufficient emphasis on financial education from a young age.

Commonly, financial mistakes occur due to a lack of understanding of interest rates, loans, and credit scores. These errors can be costly and hard to fix. Financial training helps people avoid such pitfalls by educating them on essential financial concepts.

Employers are recognizing the importance of financial training for their employees. Companies that offer financial wellness programs see increased productivity and reduced stress among workers. Investing in employee education benefits both individuals and organizations.

Current State of Financial Literacy

Financial literacy is crucial for making informed decisions about money. However, many people lack basic financial knowledge. This knowledge gap affects financial well-being and stability.

Studies have shown that financial literacy rates are alarmingly low. For instance, only 57% of American adults can pass a basic financial literacy test. This highlights the need for better education and resources.

Online courses and community programs are trying to fill this gap. These resources offer lessons on budgeting, saving, and investing. Accessible financial education can help people make better decisions.

Ironically, while information is more accessible than ever, practical knowledge about personal finance remains low. This disconnect shows the need for more effective and engaging financial education programs. Helping people understand financial principles can lead to improved personal finance management.

Impact on Daily Life

Lack of financial literacy affects everyday choices. People often make poor decisions about credit cards and loans. This leads to high debt and financial stress.

Without financial knowledge, it’s hard to plan for the future. Many people don’t save enough for emergencies or retirement. Improving financial literacy can change this.

Schools and employers can play a role in educating individuals. Offering financial education programs can help people manage their money better. Knowledgeable individuals are more likely to make sound financial decisions.

Role of Technology

Technology has made access to financial information easier. Apps and online platforms offer valuable resources. These tools help people learn about budgeting, investing, and saving.

Many apps offer features like financial planning and expense tracking. This makes it easier for people to monitor their money. Using these tools can improve financial literacy over time.

However, not everyone utilizes these technological resources. There’s a gap between availability and usage. Efforts should focus on encouraging people to use these tools.

Community Efforts

Community programs play a vital role in improving financial literacy. Nonprofits and local governments often offer workshops and classes. These programs aim to educate people of all ages.

Workshops cover topics like budgeting, credit scores, and retirement planning. They provide practical advice for managing finances. Accessible community programs can make a big difference.

Involving community leaders and local influencers can boost participation. When people see the benefits of financial education, they’re more likely to attend. Community efforts can lead to widespread improvements in financial literacy.

The Gap in Personal Finance Management

Many people find it challenging to manage their personal finances effectively. This can lead to high levels of debt and financial stress. Some struggle due to a lack of financial education.

Common mistakes include not saving for emergencies and mismanaging credit. These errors are often due to a lack of understanding of basic finance concepts. Financial training can help people avoid these pitfalls.

Limited access to financial education resources contributes to this gap. Not everyone knows where to find reliable information. Accessible financial tools and programs are essential.

Employers can help bridge this gap by offering financial wellness programs. These programs educate employees on budgeting, saving, and investing. Well-informed employees are more likely to achieve financial stability.

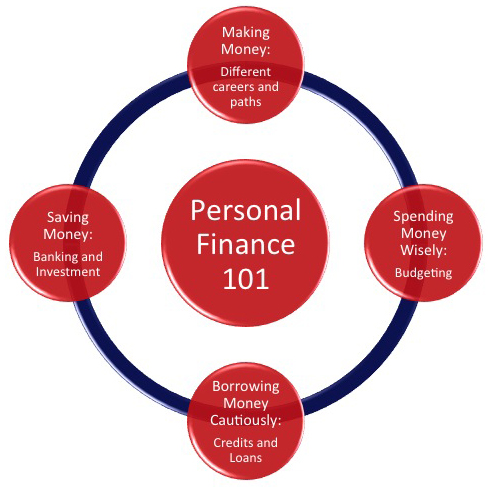

Building Blocks of Financial Training

Effective financial training starts with understanding budgeting. Creating a budget helps track income and expenses. It allows you to prioritize spending and save for the future.

Debt management is another crucial component. Knowing how to handle debt responsibly can prevent financial stress. Learning about interest rates and repayment strategies is essential.

Investing is a key element of financial training. It involves putting money into assets to grow wealth over time. Diversifying investments can reduce risk and increase returns.

Emergency savings should also be part of any training program. Having a financial cushion can help cover unexpected expenses. Aiming to save at least three to six months of living expenses is recommended.

Finally, understanding credits and loans is vital. Knowing how credit scores work and how to obtain favorable loan terms can save money. Maintaining a good credit score opens up better financial opportunities.

Many resources are available to learn these skills. Online courses, workshops, and books can provide valuable information. Utilizing these resources can dramatically improve financial literacy.

Budgeting Basics

Creating a budget is the first step to financial stability. It involves tracking your income and expenses. A budget helps you see where your money is going.

Start by listing all your sources of income. This could include your salary, freelance work, or any side jobs. Knowing your total income is essential for accurate budgeting.

Next, categorize your expenses. Break them down into fixed expenses like rent and variable ones like groceries.

- Fixed expenses: rent, utilities

- Variable expenses: groceries, entertainment

This helps you manage your spending better.

Once you’ve categorized your expenses, compare them to your income. If expenses are higher than income, it’s time to cut back. Identify areas where you can reduce spending.

Setting financial goals is also important. Goals can include saving for a vacation or paying off debt. Goals give you something to work towards and make budgeting more meaningful.

Review and adjust your budget regularly. Life changes, and so do financial needs. Keeping your budget updated ensures it stays effective.

Debt Management and Credit Understanding

Managing debt is a crucial part of financial health. It involves knowing how much debt you have and creating a plan to pay it off. This process helps you avoid falling into deeper financial trouble.

Start by listing all your debts, including credit cards, loans, and mortgages. Note the interest rates and minimum payments for each. Understanding these details helps you prioritize which debts to tackle first.

Consider the “avalanche” or “snowball” methods for paying off debt. The avalanche method focuses on high-interest debts first, while the snowball method pays off smaller debts first.

- Avalanche: Pay high-interest debts first

- Snowball: Pay smaller debts first

Choose the method that suits your situation.

Understanding credit scores is also essential in debt management. Credit scores affect your ability to get loans and the interest rates you’ll pay. Maintaining a good credit score can save you money in the long run.

To improve your credit score, make payments on time and keep credit card balances low. Regularly check your credit report for errors. Correcting mistakes can also boost your score.

Finally, consider speaking to a financial advisor if you’re overwhelmed. They can offer personalized advice and support. Professional guidance can make a significant difference in managing debt effectively.

Transforming Personal Finance through Financial Training

Financial training can significantly improve how individuals manage their money. By learning key financial skills, people can make better decisions. This leads to greater financial stability and confidence.

One important aspect is gaining knowledge about investments. Understanding where and how to invest can help grow wealth. Diversifying investments reduces risk and increases potential returns.

Financial training also covers retirement planning. Knowing how much to save and which accounts to use ensures a comfortable future. A well-planned retirement strategy is crucial for long-term security.

Additionally, these programs teach the importance of emergency funds. Having savings set aside for unexpected expenses gives peace of mind. Aim to save at least three to six months’ worth of living costs.

The impact of financial education extends beyond personal benefits. Communities become stronger when their members are financially literate.

- Stronger communities: Better financial health

- Increased economic stability: Reduced debt levels

Furthermore, employers benefit from having financially educated employees. Productivity tends to rise when workers are less stressed about money. Offering finance workshops at work can lead to a happier, more efficient workforce.

Tools for Financial Planning and Wealth Management

There are several tools available to help with financial planning. These tools can simplify budgeting, investing, and saving. Using the right tools can make managing money easier.

One popular tool is personal finance software. Software options include apps that track spending and alert you about bills. These apps help you stay on top of your financial activities.

Another useful tool is retirement calculators. They estimate how much you need to save for the future. These calculators can guide you in creating a solid retirement plan.

Investment platforms offer another valuable resource. They provide information on stocks, mutual funds, and other investment options. Using these platforms can enhance your investment strategy and grow your wealth.

Financial advisors are also important tools. They offer personalized advice and strategies for achieving financial goals. Consulting an advisor can provide tailored insights that fit your needs.

Online educational resources can further support financial planning. Websites and courses offer tutorials on various financial topics. Leveraging these resources can improve your financial literacy and management skills.

Investment and Retirement Planning

Planning for investments is a crucial part of long-term financial health. By putting money into stocks, bonds, or mutual funds, you can grow your wealth. Diversifying your investments helps reduce risk.

Many people use retirement accounts to save for the future. Options like 401(k)s and IRAs provide tax benefits. Consistently contributing to these accounts can ensure a comfortable retirement.

It’s important to start saving early. The power of compounding interest means that your money grows faster over time. Even small contributions can make a big difference in the long run.

Monitoring your investment portfolio is also key. Regularly reviewing your investments helps you stay on track with your goals. Adjusting your strategy as needed can optimize your returns.

Working with a financial advisor can provide personalized guidance. Advisors can help you choose suitable investments and retirement plans. Expert advice can be valuable in making informed decisions.

Ultimately, combining smart investments with consistent retirement savings strategies is essential.

- Start with small contributions

- Monitor and adjust your portfolio

- Seek expert advice

This approach ensures financial stability and a secure future.

Implementation and Outcome of Personal Finance Management

Implementing personal finance management starts with creating a plan. This plan should include budgeting, debt management, and savings. Having a clear plan helps guide your financial decisions.

Tracking expenses is crucial for successful management. By monitoring where your money goes, you can identify areas for improvement. This practice helps you stay within your budget.

Setting financial goals is another important step. Whether short-term or long-term, goals provide direction and motivation. Achieving these goals can give you a sense of accomplishment.

Using financial tools can make management easier. Apps and software can track expenses, remind you of due bills, and much more. Technology aids in maintaining financial discipline.

The outcomes of effective finance management are significant. They include reduced stress, increased savings, and greater financial stability.

- Reduced stress

- Increased savings

- Greater financial stability

These benefits improve overall quality of life.

Regularly reviewing your finances is essential to stay on track. Life changes, and so can your financial needs. Periodic reviews ensure your plan remains relevant and effective.

Financial Independence – From Dream to Reality

Financial independence means having enough money to cover your living expenses without relying on a job. This can be achieved through careful planning and smart investments. It’s a journey that requires dedication and patience.

Start by setting clear financial goals. Knowing what you want to achieve helps you stay focused. These goals might include paying off debt or saving for a house.

Next, create a budget that aligns with your goals. Track your income and expenses to identify areas for saving. A good budget helps you allocate money efficiently.

Investing is key to growing your wealth over time. Diversify your investments to minimize risk. Consider stocks, bonds, or real estate as options.

Here are some steps to achieve financial independence:

- Set clear financial goals

- Create and stick to a budget

- Invest wisely and diversify

- Save consistently and monitor your progress

Consistently saving money is essential. Aim to save a portion of your income every month. Automating your savings can make this easier.

Reaching financial independence takes time, but it’s possible with the right strategy. Stay committed to your goals and adjust your plan as needed. Small steps add up to big achievements over time.

Improving Financial Health with Regular Management

Regular financial management is key to a healthy financial life. By consistently monitoring your income and expenses, you can make better decisions. This practice helps prevent unexpected financial issues.

Start by setting up a monthly budget. Keeping track of what you earn and spend will show where adjustments are needed. A realistic budget helps you stay on track with your financial goals.

Saving regularly is another important aspect. Aim to save a portion of your income each month. Consistent savings can build a financial cushion for emergencies.

Investing wisely also improves financial health. Diversifying your investments can reduce risk and increase potential returns. Staying informed about market trends can guide your investment choices.

Here are some tools to help with financial management:

- Budgeting apps: Track income and expenses

- Saving plans: Automate your savings

- Investment platforms: Manage your portfolio

Review your finances regularly to stay updated. Life changes, and so do financial needs. Periodic reviews ensure your financial plan remains effective and relevant.

Frequently Asked Questions

Financial training for personal finance management equips individuals with essential skills for better financial health. These FAQs address common concerns and provide practical advice for effective money management.

1. How can financial training help with budgeting?

Financial training helps individuals understand how to create a realistic budget that tracks income and expenses. By learning to prioritize spending and save efficiently, people can achieve their financial goals faster.

A well-structured budget provides a clear picture of where your money goes each month. With this insight, you can make more informed decisions, reducing wasteful expenditures and increasing savings.

2. What are the key components of effective debt management?

Effective debt management involves understanding the total amount of debt, interest rates, and creating a repayment plan. Prioritizing high-interest debts first can save money in the long run.

Using strategies such as the “avalanche” or “snowball” methods helps streamline debt repayment. Financial training provides the knowledge tools needed to reduce or eliminate debt effectively.

3. Why is investing important in personal finance management?

Investing helps grow wealth over time by putting money into assets like stocks, bonds, or real estate. It’s an essential part of long-term financial planning because it allows funds to accumulate through returns and compounding interest.

Diversifying investments reduces overall risk while optimizing potential gains. Financial training educates individuals on different investment opportunities, making smart investment choices accessible to everyone.

4. How does emergency saving impact financial stability?

An emergency fund acts as a financial safety net for unexpected expenses like medical bills or car repairs. Saving three to six months’ worth of living expenses ensures you’re prepared for unforeseen events without going into debt.

This buffer provides peace of mind, allowing you to focus on long-term goals without constant worry about emergencies disrupting your plans. Emergency savings are fundamental in achieving financial security.

5. What role do financial advisors play in personal finance management?

Financial advisors offer personalized guidance tailored to individual needs and goals. They help create comprehensive plans covering budgeting, investing, retirement planning, and more.

Their expertise ensures clients make informed decisions that align with their objectives while avoiding common pitfalls. Accessing professional advice enhances overall financial well-being and confidence in managing finances independently.

Conclusion

Financial training for personal finance management is an invaluable tool that empowers individuals to take control of their financial future. By mastering budgeting, debt management, and investment strategies, people can achieve greater financial stability and peace of mind. The benefits extend beyond personal gain, contributing to a stronger and more resilient community.

For experts, advanced financial tools and knowledge provide deeper insights into wealth management and retirement planning. This comprehensive understanding allows for more effective resource allocation and long-term financial success. Investing in financial training is a step toward building a secure and prosperous future for all.