In 1936, John Maynard Keynes revolutionized economics with his seminal work, “The General Theory of Employment, Interest and Money.” Keynes challenged classical economics, emphasizing aggregate demand’s role in economic stability. Ever since, macroeconomics has evolved, encompassing various schools of thought and intricate models explaining economic fluctuations.

The advent of computational advances has allowed for more sophisticated economic modeling. For instance, real business cycle theory integrates technology shocks to explain economic cycles. Today, macroeconomists utilize dynamic stochastic general equilibrium models to provide a deeper understanding of economic phenomena, making cutting-edge analysis indispensable in policy formulation.

The Shift from Classical to Keynesian Economics

The Concept of Aggregate Demand in Keynesian Economics

Before Keynesian economics, classical economists believed that markets always clear, meaning supply always equals demand. However, during the Great Depression, this theory failed. Keynes argued that total spending, or aggregate demand, drives economic activity and unemployment.

According to Keynes, when aggregate demand is high, businesses produce more, creating jobs. Conversely, when demand is low, production slows, leading to high unemployment. This idea challenged the classical view that markets are always self-correcting.

To combat low demand, government intervention was deemed necessary. Keynes suggested that governments could spend money to stimulate economic activity. This was a radical shift from the classical belief in minimal government interference.

Keynesian Economics and its Emphasis on Macroeconomic Policy

Keynesian economics reshaped how governments approached economic policy. Prior, governments did very little to manage the economy. Keynes emphasized active fiscal policy, such as public spending and tax adjustments.

A key aspect of Keynesian economics is the focus on short-term goals, like reducing unemployment. This is different from classical economics, which focused more on long-term growth and stability. By using fiscal policy, governments could quickly respond to economic downturns.

Additionally, Keynesian economics led to the establishment of welfare programs. These programs aimed to support people during tough economic times. This approach also promoted a more stable and balanced economy.

The Introduction of Real Business Cycle Theory

Real Business Cycle (RBC) theory emerged as a response to Keynesian economics. This theory emphasizes technology changes as the primary driver of economic cycles. RBC theorists argue that economic fluctuations result from real, rather than monetary, shocks.

Unlike Keynesians, RBC proponents believe these fluctuations reflect efficient responses to changes. For example, a new technology could increase productivity, leading to economic growth. If technology fails, productivity might drop, causing a recession.

RBC theory has influenced modern macroeconomics through its emphasis on real factors. It sparked debates on the roles of technology and productivity in driving economic cycles. Despite its differences, RBC and Keynesian economics both aim to explain economic fluctuations.

Monetarism and its Differences from Keynesian Economics

Monetarism, popularized by economist Milton Friedman, focuses on the role of money supply in the economy. Unlike Keynesians, monetarists believe controlling the money supply is crucial for managing inflation. They argue that changes in money supply have short-term and long-term effects on output and prices.

Monetarists criticize Keynesian policies for potentially causing inflation. They advocate for a steady, small increase in money supply instead of large fiscal interventions. This approach aims to provide stability while avoiding the risks of inflation.

In practice, monetarist policies emphasize central bank independence. This allows central banks to focus on controlling inflation without political pressure. While different from Keynesian economics, monetarism has shaped modern economic policies.

The Concept of Aggregate Demand in Keynesian Economics

Aggregate demand is a key idea in Keynesian economics. Unlike classical economists, Keynesians believe that total spending drives the economy. When people spend more, businesses produce more, boosting employment.

Understanding Aggregate Demand

Aggregate demand includes all goods and services bought by households, businesses, and the government. When aggregate demand is high, the economy grows. Conversely, if demand drops, the economy can slow down, leading to unemployment.

Keynes argued that during a recession, businesses cut back on production. This creates a cycle where low demand leads to less production, which causes more unemployment. The government can step in to boost aggregate demand through public spending.

Government’s Role in Managing Demand

Keynes believed that government intervention is crucial during economic downturns. By increasing spending or cutting taxes, the government can stimulate demand. This helps reduce unemployment and supports economic recovery.

For example, during a recession, the government might invest in infrastructure projects. These projects create jobs, putting money in people’s pockets, which they then spend. This spending helps boost aggregate demand, aiding the economy.

Another tool is monetary policy, where central banks might lower interest rates. Lower rates make borrowing cheaper, encouraging both consumers and businesses to spend more. This also helps increase aggregate demand.

Private Sector and Aggregate Demand

The private sector plays a crucial role in aggregate demand. Household spending on goods and services forms a large part of total demand. When consumers are confident about the economy, they tend to spend more.

Businesses invest in new projects and hire more workers when they expect higher demand. This increases aggregate demand further. However, during uncertain times, businesses might cut back, leading to a decrease in demand.

Therefore, government policies often aim to maintain consumer and business confidence. By doing so, they help stabilize aggregate demand, ensuring steady economic growth. This balance between the private sector and government intervention is essential for a healthy economy.

Keynesian Economics and its Emphasis on Macroeconomic Policy

Keynesian economics focuses heavily on **macroeconomic policy** to manage the economy. Unlike classical economics, which emphasizes laissez-faire approaches, Keynesians believe in active government intervention. This involves both fiscal and monetary policies to stabilize economic cycles.

Fiscal policy involves government spending and taxation to influence aggregate demand. For example, during a recession, the government might increase spending on public projects. This boosts employment and injects money into the economy, raising demand.

Monetary policy, on the other hand, is managed by central banks. They adjust interest rates and control the money supply to keep the economy stable. Lowering interest rates can encourage borrowing and spending, which again boosts demand.

Combining both fiscal and monetary policies helps manage economic fluctuations. During periods of high unemployment, these policies aim to increase spending and job creation. Conversely, during periods of inflation, policies might focus on reducing demand to stabilize prices.

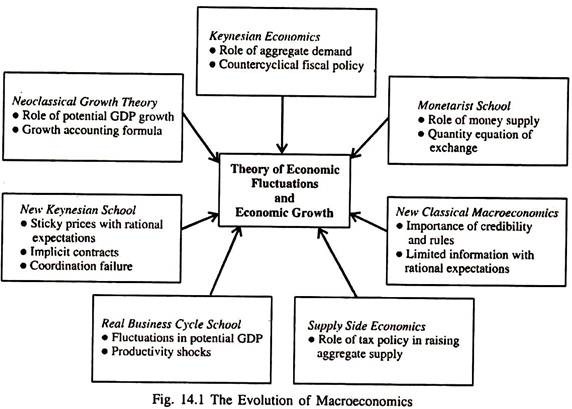

Contemporary Schools of Macroeconomic Thought

Modern macroeconomics includes several influential schools of thought. Each has its own ideas on how to manage the economy. Monetarism, for instance, emphasizes the role of money supply in controlling inflation.

Monetarists believe that stable growth in the money supply is key. They argue that too much money leads to inflation, while too little causes recession. Milton Friedman is one of the famous proponents of this theory.

New Keynesianism is another contemporary school of thought. It builds on Keynesian principles but incorporates modern elements like price and wage stickiness. This means prices and wages don’t adjust quickly to changes in supply and demand.

Real Business Cycle (RBC) theory takes a different approach. RBC theorists focus on real factors like technology changes as drivers of economic cycles. They argue that these changes explain why economies expand and contract.

While different, these schools all contribute to the broader understanding of macroeconomics. Policymakers often draw from multiple theories to create balanced economic policies. This blend of ideas helps in addressing complex economic issues.

Monetarism and its Differences from Keynesian Economics

Monetarism is a school of thought that focuses on the importance of the money supply in the economy. Milton Friedman, a key figure in monetarism, argued that **controlling the money supply is crucial to managing inflation**. Unlike Keynesians, monetarists believe that changing the money supply directly affects economic output and price levels.

Keynesian economics, on the other hand, focuses on aggregate demand. Keynesians believe that government intervention, through fiscal policy like spending and taxes, can stabilize the economy. They argue that during economic downturns, increased public spending can boost demand and reduce unemployment.

Monetarists criticize this approach by arguing that it can lead to inflation. They prefer a steady, predictable growth in the money supply to avoid economic instability. According to monetarists, too much government intervention distorts market signals and causes inflationary pressures.

Another key difference is how these schools view monetary policy. Monetarists place a lot of trust in central banks to manage the money supply. They believe that keeping inflation low and stable is the best way to ensure long-term economic growth.

Keynesians, however, often support a broader role for government policies. They believe that in addition to monetary policy, **fiscal measures** are essential to manage economic cycles. This includes government spending on infrastructure projects and social programs to boost demand.

Both theories have shaped modern economic policies, though they emphasize different aspects. Policymakers might use a blend of both approaches to address complex economic challenges. Understanding these differences helps in crafting balanced and effective economic policies.

The Advent of New Classical Macroeconomics

The emergence of New Classical Macroeconomics marked a significant shift in economic thought. This school of thought emphasizes rational expectations and market-clearing models. New Classicists argue that economic agents make decisions based on all available information.

A key component of New Classical Macroeconomics is the Rational Expectations Hypothesis. People anticipate the effects of economic policies and adjust their behavior accordingly. This means that policy interventions are often ineffective because individuals adapt.

The theory also focuses on how quickly markets adjust to changes. Unlike Keynesians, New Classical economists believe that markets clear quickly without prolonged periods of unemployment. They argue that prices and wages are flexible and respond rapidly to shifts in supply and demand.

One of the main critiques of this theory is its assumption of perfect information. Critics argue that not all economic agents have access to the same information. This can lead to discrepancies in how different groups respond to economic policies.

Despite this, New Classical Macroeconomics has influenced modern policy-making. For instance, it has reinforced the idea that monetary policy should be rules-based rather than discretionary. This minimizes the uncertainty in economic planning and helps stabilize markets.

Overall, the advent of New Classical Macroeconomics introduced key concepts that focus on individual decision-making and market efficiency. Its principles continue to shape how economists and policymakers understand and manage economic fluctuations.

The Role of Computational Advances in Economic Theory Evolution

Computational advances have revolutionized economic theory and practice. With the power of modern computers, economists can now analyze vast amounts of data quickly. This has led to more accurate models and predictions.

One significant development is the use of **dynamic stochastic general equilibrium (DSGE) models**. These models incorporate random fluctuations and predict how economies evolve over time. Policymakers rely on DSGE models to make informed decisions about monetary and fiscal policies.

| Advancement | Impact |

|---|---|

| Big Data Analytics | Helps in understanding consumer behavior and market trends |

| Machine Learning | Improves accuracy in forecasting economic variables |

| High-Performance Computing | Enables simulation of complex economic scenarios |

Big data analytics have also become crucial for macroeconomic analysis. By examining large datasets, economists can identify patterns that were previously impossible to see. This has improved our understanding of everything from consumer behavior to global trade dynamics.

The use of machine learning algorithms allows for better prediction of economic trends. These algorithms analyze past data to forecast future events with greater precision. For example, they can predict stock market movements or unemployment rates.

The integration of high-performance computing enables the simulation of intricate economic scenarios. Economists can test how different policies will affect an economy before implementing them in real life. This helps policymakers avoid mistakes and make better choices.

Merging these computational tools has transformed the field of economics, making it more precise and predictive. As technology continues to advance, we can expect even more innovative methods to understand and manage economies globally.

The Introduction of Real Business Cycle Theory

Real Business Cycle (RBC) theory is a significant development in macroeconomics. It emphasizes how real factors, like technology changes, influence economic cycles. Unlike Keynesian economics, RBC theory focuses on long-term economic behavior.

According to RBC theory, economies experience fluctuations due to **real shocks** rather than just monetary factors. These real shocks include changes in technology, resources, or productivity. For example, a technological advancement can boost productivity, leading to economic growth.

RBC theorists argue that individuals and firms optimize their decisions based on these real factors. They believe that markets are always clear, meaning supply and demand balance out naturally. This leads to efficient outcomes even during economic fluctuations.

The theory also introduces the concept of dynamic programming in economics. This method helps in creating models that predict how economies evolve over time. These models take into account various real factors and their impact on the economy.

Critics argue that RBC theory overlooks the role of demand-side factors. They believe that it doesn’t fully explain why economies experience prolonged periods of high unemployment. Despite this, RBC theory has shaped the way economists analyze economic cycles.

Understanding RBC theory provides valuable insights into how economies respond to real-world changes. It helps in crafting policies that consider both supply and demand factors. This balanced approach aids in managing economic stability more effectively.

The Impact of Dynamic Stochastic General Equilibrium Models

The introduction of Dynamic Stochastic General Equilibrium (DSGE) models has transformed macroeconomic analysis. These models help economists understand how economies evolve over time. They incorporate random shocks, making them more realistic.

DSGE models are essential for studying how policies impact the economy. Governments and central banks use them to predict the effects of monetary and fiscal policies. This helps in making informed decisions.

One of the key features of DSGE models is their ability to incorporate various types of data. This includes information on consumer behavior, investment, and international trade. Economists can simulate different scenarios to see how the economy would react.

Using DSGE models, policymakers can better manage economic stability. These models highlight potential risks and allow for the testing of policy changes before implementation. As a result, mistakes and negative impacts can be minimized.

Creating a DSGE model involves complex computations and programming. Despite their complexity, these models provide accurate and detailed insights. They are a testament to how far economic analysis has come with the help of technology.

The impact of DSGE models is significant in both academic and practical applications. Economists continue to refine these models for even better predictions. Overall, DSGE models play a crucial role in understanding and managing economic fluctuations.

Future Trends in Macroeconomics and Economic Theory

Macroeconomics is set to evolve significantly in the future. Technological advancements will play a major role. More advanced computational models will enhance the accuracy of economic forecasts.

Behavioral economics is gaining traction as a key area of focus. This field examines how psychological factors influence economic decision-making. It challenges traditional theories that assume people always act rationally.

Sustainability and environmental concerns are also becoming central to economic theory. Green economics, which emphasizes eco-friendly policies, is expected to grow. This shift will affect how governments and businesses approach economic growth.

The rise of digital currencies like Bitcoin is creating new avenues for economic research. Economists are beginning to explore how these currencies impact traditional financial systems. This will likely result in new monetary policies and regulations.

Globalization will continue to shape economic theory. Trade policies and international relations will impact how economies interact. Economists will need to focus more on global interdependencies.

Overall, the future of macroeconomics will involve a blend of traditional theories and new approaches. As technology and societal values evolve, so will economic theories and policies. These changes aim to create a more inclusive and sustainable global economy.

The Rise of Behavioral Macroeconomics

Behavioral macroeconomics blends psychology with economic theory. Unlike traditional economics, it explores how people actually behave. This includes emotions, biases, and other psychological factors.

One key idea is that people don’t always act rationally. They may make decisions based on emotion or incomplete information. This affects spending, saving, and investing, which in turn impacts the broader economy.

Behavioral economists study patterns to predict economic outcomes. They look at how people react to news, changes in policy, and even advertising. This helps in creating policies that are more effective and realistic.

- Overconfidence can lead to risky investments.

- Loss aversion means people fear losses more than they value gains.

- Herd behavior occurs when people follow the actions of a larger group.

Governments are using these insights to design better policies. For example, they might create nudges that encourage saving for retirement. By understanding human behavior, they can better influence economic decisions.

Overall, behavioral macroeconomics is a growing field. It adds depth to how we understand economic activities. As more research is conducted, it promises to make economic policies more effective and humane.

Macroeconomics and Economic Sustainability in the Future

Economic sustainability is an increasingly important goal for future macroeconomics. It means balancing economic growth with environmental protection and social well-being. Future policies will aim to achieve this balance in various ways.

Green investments are one way to promote sustainability. These investments focus on renewable energy and eco-friendly technologies. They aim to reduce environmental harm while promoting economic growth.

- Solar and wind energy projects

- Electric vehicle infrastructure

- Energy-efficient buildings

Another important area is inclusive growth. This means ensuring that all segments of society benefit from economic progress. Policies will need to address income inequality and provide opportunities for marginalized groups.

Governments may also use carbon taxes to reduce pollution. These taxes make it more expensive to emit greenhouse gases, encouraging businesses to adopt cleaner practices. This approach aims to protect the environment while generating revenue for green initiatives.

Sustainable economic policies must balance short-term needs with long-term goals. Immediate actions may focus on job creation and economic recovery. However, they must also consider the environmental and social impacts to ensure lasting sustainability.

Overall, achieving economic sustainability requires the cooperation of multiple sectors. Businesses, governments, and communities must work together. By integrating economic, environmental, and social goals, future policies can create a more balanced and sustainable world.

Frequently Asked Questions

Delve into the fascinating world of macroeconomics and how economic theories have evolved over time. Here are some commonly asked questions on this dynamic topic.

1. How did Keynesian economics revolutionize macroeconomic thought?

Keynesian economics introduced the idea that government intervention is crucial in managing economic activity. It shifted focus from self-regulating markets to active policies aimed at influencing demand and reducing unemployment.

This approach became particularly influential during economic downturns, such as the Great Depression. Governments began adopting fiscal policies like public spending and tax cuts to stimulate aggregate demand.

2. What is the significance of real business cycle theory?

Real Business Cycle (RBC) theory emphasizes how real shocks, such as technology changes, impact economic cycles. Unlike other theories, RBC focuses on supply-side factors rather than demand-side factors like government spending.

Proponents argue that economies naturally respond to real changes with efficient adjustments in labor and production. This offers a different lens for understanding fluctuations compared to traditional Keynesian models.

3. Why are dynamic stochastic general equilibrium models important?

Dynamic Stochastic General Equilibrium (DSGE) models are vital for predicting how economies react over time to various shocks and policies. They incorporate random elements, making them highly realistic for analyzing complex scenarios.

Used extensively by policymakers, these models help simulate different outcomes before implementing measures in the real world. This reduces uncertainty and improves decision-making processes in macroeconomic planning.

4. How does behavioral economics differ from traditional macroeconomics?

Behavioral economics examines psychological influences on economic decisions, unlike traditional theories assuming rational behavior. It studies how biases and emotions affect spending, saving, and investing patterns.

This field provides insights into more realistic human behaviors, aiding in designing effective policies that account for actual decision-making processes instead of purely theoretical ones.

5. What role do technological advancements play in modern economic theory?

Technological advancements have significantly enabled more accurate data analysis, intricate modeling, and better forecasts in economics. Tools like big data analytics and machine learning offer deeper insights into market trends and consumer behavior.

The integration of high-performance computing has also allowed for simulating complex scenarios rapidly. These computational tools keep evolving economic theories aligned closely with real-world developments.

Conclusion

The evolution of macroeconomic theories, from classical to Keynesian, and now to more advanced models like DSGE and behavioral economics, reflects our growing understanding of complex economic systems. These advances have enabled policymakers to make more informed decisions, balancing immediate needs with long-term stability.

As technology continues to progress, the future of macroeconomics looks promising. Combining traditional theories with cutting-edge computational tools will offer even deeper insights, ensuring more sustainable and inclusive economic growth. The continued evolution of economic theory will be essential in meeting the challenges of a dynamic, ever-changing world.