How often do you skim your credit card statement without really understanding the details? It’s easy to overlook key sections, leading to missed opportunities for catching errors or understanding your spending habits. Mastering the skill of reading this document can significantly impact your financial health.

Credit card statements became common in the mid-20th century when plastic money started gaining traction. According to a recent survey, 42% of consumers find statements confusing. Knowing how to read sections like the statement balance, minimum payment, and transaction summary can offer a clearer financial picture and help avoid costly fees.

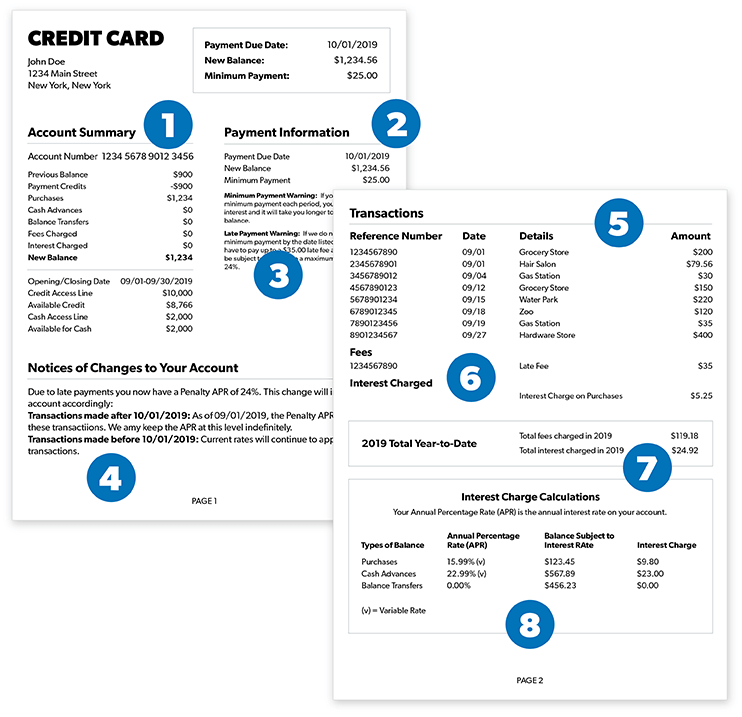

- Identify the statement period and check the opening and closing balances.

- Review the account summary for a snapshot of your current balance, credit limit, and available credit.

- Look at payment information to understand the minimum payment due and due date.

- Examine the transaction summary for detailed listings of all purchases, payments, fees, and credits.

- Analyze interest charges to see how they are calculated based on your APR and balance.

- Check the rewards summary to track earned points or cash back.

- Review any fees listed to ensure there are no unexpected charges.

Unraveling the World of Credit Card Statements

Your credit card statement offers a detailed record of your recent financial activities. Understanding it can help you manage your finances better and avoid unwanted fees. It’s not just a list of transactions but a snapshot of your financial health.

The statement includes several sections, each providing critical information. There’s the account summary, which shows your balance and available credit. Payment information tells you when and how much to pay.

The transaction summary lists all your recent purchases, returns, and payments. Carefully review this section for any errors or unexpected charges. This could save you from paying for something you didn’t buy.

Finally, interest and fees are detailed separately. This section explains how much interest you’re paying on overdue amounts. Knowing this can help you plan to pay off your debt faster.

Deciphering the Account Summary

The account summary is a crucial section of your credit card statement. It gives you a quick snapshot of your account’s status, including the balance and available credit. Understanding this part can help you manage your spending more effectively.

Balance Information

The balance shows how much you owe to the credit card company. This figure includes all your purchases, fees, and interest up to the statement date. Keeping track of this helps in avoiding debt.

If your balance is higher than expected, you might be spending too much. Review your expenses and find ways to cut back. This will help you maintain a healthy balance.

Regularly checking your balance also helps catch any errors. If you find any discrepancies, report them immediately. This ensures your statement is accurate.

Credit Limit

Your credit limit is the maximum amount you can borrow on your credit card. Exceeding this limit can result in additional fees and a negative impact on your credit score. Knowing your limit helps you stay within budget.

Regularly monitoring your available credit is also wise. This is the amount you have left to spend. Keeping this in mind can prevent overspending.

If your available credit is low, it might be time to pay off some of your balance. This will free up more credit for future use. It’s a good practice to pay off your balance in full whenever possible.

Minimum Payment Due

The minimum payment due is the smallest amount you must pay by the due date. Failing to pay this can lead to late fees and a higher interest rate. Always aim to pay at least this amount to avoid penalties.

Paying only the minimum can keep you in debt longer. Interest will accumulate on the remaining balance. It’s better to pay as much as you can afford to reduce your debt faster.

Setting up automatic payments can ensure you never miss the minimum payment. This simple step can help you maintain a good credit history. Always review your statement even if you have auto-pay set up.

Breaking Down the Payment Information

Payment information on your credit card statement is essential for managing your finances. It includes details such as the payment due date, total amount due, and minimum payment required. Understanding these can help you avoid late fees and interest charges.

The **payment due date** is crucial. This is when your payment must be received by the credit card company. Missing this date can result in late fees and a negative impact on your credit score.

**Total amount due** is the complete balance you owe. Paying this amount helps you avoid interest and keeps your debt under control. If you can’t pay in full, try to pay as much as possible.

**Minimum payment required** is the smallest amount you must pay by the due date. Paying only this keeps your account in good standing but can lead to more interest charges. Always aim to pay more than the minimum to reduce your debt faster.

Reading the Transaction Summary

The transaction summary is a key part of your credit card statement. It lists all purchases, payments, and credits during the billing period. Reviewing it helps ensure all charges are correct.

Different types of transactions are usually categorized. You’ll see labels like purchases, payments, fees, and interest charges. This breakdown makes it easier to spot any discrepancies.

Each transaction includes essential details. Information like the date, merchant name, and amount spent is provided. Double-check these details to catch any unfamiliar charges.

If you notice an error, contact your credit card issuer immediately. Prompt action can help resolve mistakes quickly. Most companies have a formal dispute process for incorrect charges.

A clean transaction summary also shows how you’re spending your money. Use this data to analyze your spending habits. This can help you better manage your budget and save more efficiently.

Regularly reviewing your transaction summary is a healthy financial practice. It keeps you informed and helps prevent fraud. Staying vigilant with your transactions safeguards your financial well-being.

Importance of Interest Charge Calculation

Interest charges are a critical aspect of credit card management. They can significantly affect how much you pay over time. Understanding how these charges are calculated is vital to managing your debt.

Interest is usually calculated based on your average daily balance. This means your balance at the end of each day is used to compute your interest. Higher daily balances result in higher interest charges.

Knowing your Annual Percentage Rate (APR) is essential. The APR is the interest rate charged over a year. It allows you to compare costs between different credit cards easily.

Most credit card companies offer a grace period. If you pay your balance in full by the due date, you can avoid interest charges. This is a great way to use your credit card without incurring extra costs.

Setting up automatic reminders for payments is helpful. This way, you can avoid late fees and additional interest. Staying on top of your payments keeps your financial health in check.

For those carrying a balance, consider using a credit card with a lower APR. This can save you money over time. Small changes in interest rates can lead to big savings.

Taking a Closer Look at Rewards Summary

The rewards summary is a valuable part of your credit card statement. It shows how many points, miles, or cash back you’ve earned. Understanding this can help you maximize your benefits.

Most credit cards offer different types of rewards. These can include points for travel, cash back on groceries, or miles for flights. Knowing what your card offers lets you make the most out of every purchase.

Check the expiration dates on your rewards. Some points or miles will expire if not used within a specific time frame. Keep track of these dates to avoid losing rewards.

The rewards summary often includes ways to redeem your points. Options might range from travel bookings to statement credits. Understanding how to use your rewards effectively can offer significant savings.

Some credit cards offer bonuses for reaching spending milestones. Paying attention to these opportunities can boost your rewards quickly. For example, spending a certain amount in the first three months might earn you additional points.

Regularly reviewing your rewards summary helps you plan your spending. This ensures that you’re using your credit card strategically. Being proactive about your rewards can lead to better financial decisions.

Ensuring Financial Health with Fee Summary

The fee summary on your credit card statement shows various charges. These can include late fees, over-limit fees, and foreign transaction fees. Understanding these fees is crucial for maintaining financial health.

Identifying different types of fees helps you know what you’re paying for. Common fees are listed clearly in this part of the statement. By knowing these details, you can make smarter financial choices.

Avoiding unnecessary fees can save you money. For instance, always pay on time to avoid late payment charges.

- Set reminders for due dates.

- Consider automatic payments.

If traveling abroad, watch out for foreign transaction fees. Using a travel-friendly credit card might be a better option. It’s an easy way to avoid extra costs while spending internationally.

Regularly reviewing the fee summary helps you understand your spending habits better. Seeing recurring fees might prompt changes in behavior to reduce them. Your goal should be to minimize or eliminate these extra costs.

This section also aids in budgeting for future months by understanding past expenses. Keeping an eye on your fee summary ensures you’re not caught off guard by unexpected charges.This proactive approach keeps your finances healthy.

Using the Statement as a Budgeting Tool

Your credit card statement provides valuable insights for budgeting. By analyzing your spending, you can create a more effective budget. This helps you manage your finances better and avoid unnecessary expenses.

Start by reviewing the transaction summary. This section lists all your purchases, payments, and fees. Group similar expenses to identify areas where you can cut costs.

Using a credit card statement as a budgeting tool lets you see spending patterns.

- Track your monthly expenses.

- Compare spending with your budget.

- Adjust as necessary to stay on track.

The statement also shows how much you’re paying in interest and fees. This information is crucial for understanding the full cost of using credit. Reducing these expenses can free up more money for savings and other goals.

Finally, set spending limits based on past statements. Knowing your spending habits allows you to allocate funds more wisely. This proactive approach ensures a healthier financial future.

Regularly reviewing your statement helps you stay disciplined. Automated tools and alerts can assist in tracking your budget. Utilize these features to maintain control over your finances.

Frequently Asked Questions

Credit card statements can be confusing, but understanding them is essential for managing your finances. Here are some common questions and answers to help you navigate through your credit card statement effectively.

1. What is the billing cycle on a credit card statement?

The billing cycle is the period between billings, typically lasting about a month. It includes all transactions, fees, and interest charges made during that time.

The start and end dates of the billing cycle are usually listed at the top of your statement. Knowing this helps you understand which transactions are included in your current bill.

2. How can I avoid paying interest on my credit card?

You can avoid paying interest by paying off your full balance each month by the due date. This ensures you’re only using credit temporarily without incurring extra costs.

If you carry a balance month-to-month, you’ll be charged interest based on your APR. Set reminders or automate payments to ensure timely and full payments.

3. Why is there a discrepancy between my available credit and my account balance?

The available credit subtracts any pending transactions from your total credit limit, giving you a more accurate picture of what’s still spendable. While the account balance shows what you owe up till now.

This discrepancy can help prevent overspending by alerting you to pending bills that haven’t yet appeared in your account summary but will reduce your available funds soon.

4. How do foreign transaction fees appear on my statement?

Foreign transaction fees usually appear as separate line items in your transaction summary alongside each international purchase made with the card.

These fees might look small individually but can add up over multiple purchases. Reviewing this section ensures transparency in international spending costs.

5. Are annual fees worth it on credit cards?

The value of an annual fee depends on whether you maximize the card’s benefits—like rewards, travel points, or cash back—to outweigh the cost of the fee itself.

If you don’t use these perks often enough to justify yearly expenses, consider switching to a no-annual-fee option for potential savings and better financial management.

Final Thoughts

Mastering your credit card statement is a key aspect of financial health. By understanding each section, you can make informed decisions that benefit your wallet. It’s more than just reading numbers; it’s about taking control of your finances.

Regularly reviewing and comprehending your statement helps avoid fees and maximize rewards. It also keeps you alert to any errors or fraudulent activity. Stay proactive in managing your credit card, and it will serve you well in your financial journey.