Credit card debt can snowball faster than you expect, leaving many to feel they’re drowning in financial quicksand. Shocking as it may sound, the average U.S. household carries over $6,000 in credit card debt. So how do you escape this cycle of high-interest payments and mounting balances?

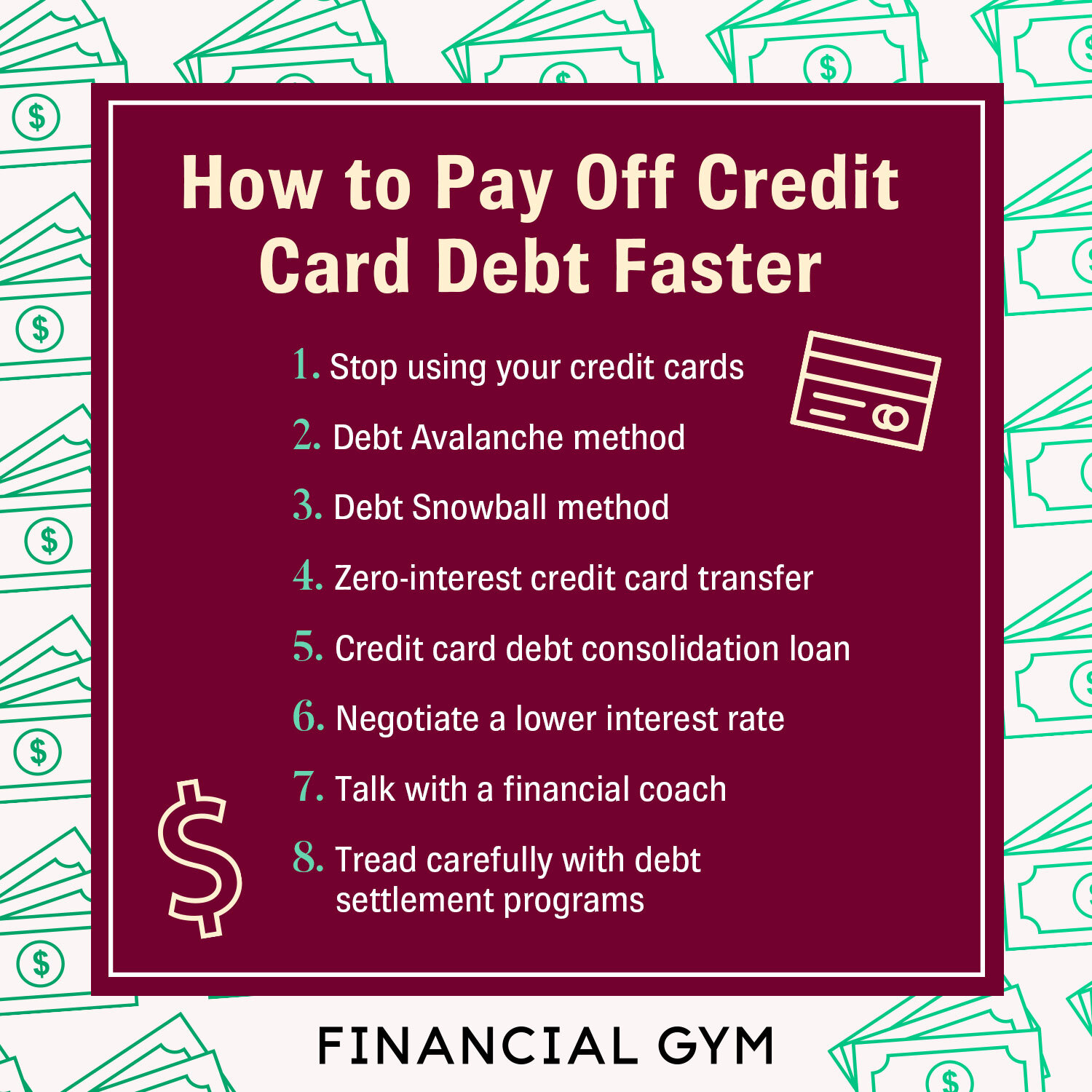

One effective method is to follow the debt avalanche strategy, where you focus on paying off the card with the highest interest rate first. This approach minimizes the interest you pay over time, accelerating your freedom from debt. Additionally, consolidating debt through a lower-interest personal loan can offer immediate financial relief and a clear path to being debt-free faster.

- Create a budget to track your expenses and identify areas for cuts.

- Pay more than the minimum payment each month.

- Use the debt avalanche method to target high-interest debts first.

- Consider a balance transfer credit card with a lower interest rate.

- Seek professional advice if needed to create a structured plan.

Understanding Credit Card Debt

Credit card debt can quickly spiral out of control if not managed properly. Many people use credit cards for daily expenses, thinking it’s convenient. However, it’s easy to lose track of spending and accumulate a large balance.

The interest rates on credit cards are often quite high. This means that even small unpaid balances can grow rapidly. Each month, if you don’t pay off your balance in full, you’ll incur interest charges that add up.

Understanding how interest works is crucial. Interest is the fee you pay for borrowing money, and it’s usually expressed as an annual percentage rate (APR). The higher the APR, the more you’ll end up paying over time.

Being aware of your spending habits can help avoid debt. Track where your money goes each month and minimize unnecessary expenses. By doing so, you can keep your credit card balance manageable.

Planning Your Debt Payoff Strategy

Creating a plan is essential for paying off your credit card debt faster. It helps you stay organized and motivated. Let’s look at a few strategies.

Assessing Your Current Financial Situation

The first step is to know exactly how much you owe. Look at your credit card statements and add up all your balances. This gives you a clear starting point.

Next, list your monthly income and expenses. This helps identify areas where you can cut back. The goal is to free up more money for debt payments.

Set a realistic budget based on your income and necessary expenses. Make sure to include a portion of your income specifically for debt repayment. Stick to this budget to make steady progress.

Choosing the Right Debt Repayment Method

Two popular methods for paying off debt are the debt avalanche and debt snowball methods. The debt avalanche method focuses on paying off the card with the highest interest rate first. This can save you money on interest in the long run.

The debt snowball method, on the other hand, targets the smallest balance first. This can provide quick wins and boost your motivation. Choose the method that best fits your situation and personality.

Consistency is key. Regardless of the method, make sure you stick with it. Consistent payments will speed up the process.

Tracking and Adjusting Your Progress

Regularly track your progress to see how much you have paid off. This can be motivating and also highlight any areas where you need to adjust. Use a spreadsheet or a budgeting app to keep everything in one place.

If you find that your strategy isn’t working as expected, don’t be afraid to make changes. Life situations can change, and your plan should be flexible enough to adapt. Adjusting your strategy can help you stay on track.

Celebrate your milestones, no matter how small. This keeps you motivated and focused on your goal of becoming debt-free.

The Debt Avalanche Method

The Debt Avalanche Method targets your highest-interest debt first. This strategy helps you save money on interest over time. It’s particularly useful if you have several credit card debts with varying interest rates.

Start by listing all your debts, focusing on the interest rates. Make minimum payments on all debts except the one with the highest rate. Allocate any extra money to this high-interest debt until it’s paid off.

Once the highest-interest debt is cleared, move to the next highest. Repeat this process until all your debts are paid. This method not only pays off debt faster but also minimizes the money spent on interest.

Staying disciplined is crucial for the Debt Avalanche Method to work effectively. It requires patience and consistency. However, the long-term financial benefits make the effort worthwhile.

The Debt Snowball Method

The Debt Snowball Method focuses on paying off your smallest debt first. This approach can give you quick wins, which provide a psychological boost. Once a small debt is paid off, you can move on to the next smallest.

Start by listing all your debts from smallest to largest. Make minimum payments on all debts except the smallest one. Throw any extra money at the smallest debt until it’s paid off.

Once the smallest debt is paid, take the money you used for it and apply it to the next smallest debt. This creates a snowball effect, gradually increasing the amount of money available to pay off larger debts. This momentum can keep you motivated throughout the process.

One major advantage of this method is its simplicity. It doesn’t require complex calculations. You just need to follow the order you’ve set and stay consistent.

While the Debt Snowball Method may not save as much on interest as the Debt Avalanche Method, it’s beneficial for those who need motivational boosts. The satisfaction of seeing debts disappear quickly can be very encouraging. This can make the method particularly effective for people struggling to stay committed to long-term debt repayment plans.

Track your progress closely to stay motivated. Use a chart or a debt payoff app to visualize the declining balances. This visual aid can serve as a constant reminder of your achievements.

Consolidating Credit Card Debt

Consolidating credit card debt can simplify your financial life. By combining multiple debts into one, you reduce the number of payments you need to manage. This can also lower your overall interest rate.

One common method for consolidation is taking out a personal loan. The loan should have a lower interest rate compared to your credit cards. Use the loan to pay off all your credit card balances.

Another option is a balance transfer credit card. These cards offer low or 0% interest rates for a promotional period. Transfer your existing card balances to the new card and focus on paying it off before the promotional period ends.

Home equity loans can also be used for debt consolidation. They often have lower interest rates than credit cards. However, they put your home at risk if you can’t make the payments.

- Personal Loans: Lower interest rates, fixed terms

- Balance Transfer Cards: Promotional low rates

- Home Equity Loans: Use home’s equity, lower interest

Be aware of the fees involved in consolidation. Balance transfer cards may have transfer fees. Personal loans might come with origination fees. Calculate all costs to ensure that consolidation will actually save you money.

Negotiating Lower Interest Rates with Credit Card Companies

Negotiating lower interest rates can save you a lot of money. Many people don’t realize they can call their credit card companies and ask for a lower rate. It might sound daunting, but it’s worth the effort.

Start by gathering your account details. Know your current interest rate, outstanding balance, and payment history. This information will help you make a strong case.

Practice what you’ll say before making the call. Explain your reasons for requesting a lower rate, like being a loyal customer or experiencing financial hardship. Be polite but firm in your request.

If your initial request is denied, don’t give up. Ask to speak to a supervisor or call back later. Sometimes persistence pays off.

- Prepare your account details: Interest rate, balance, and payment history

- Practice your request: Explain your reasons clearly

- Persist if denied: Ask for a supervisor or call back

Even a small reduction in your interest rate can make a big difference. Lower interest means more of your payments go toward reducing the principal balance. This helps you pay off your debt faster.

Staying Out of Credit Card Debt

Maintaining discipline with your spending habits is key to staying out of credit card debt. Start by creating a monthly budget and sticking to it. This will help you manage your expenses and avoid unnecessary purchases.

Avoid carrying a balance on your credit cards. Pay off the full amount each month if possible. This prevents interest from accumulating and keeps your debt manageable.

If you tend to overspend, consider using cash or debit cards instead of credit cards. These payment methods limit you to spending only what you have. It’s a simple but effective way to control your finances.

- Create a monthly budget: Track income and expenses

- Pay in full: Avoid carrying balances on credit cards

- Use cash or debit: Limit spending to available funds

Emergency funds can be a lifesaver in unexpected situations. Set aside some money each month for emergencies. This helps prevent the need for using credit cards when surprise expenses occur.

Regularly review your financial situation. Keep an eye on your spending patterns and adjust as needed. Staying proactive helps you catch potential issues before they become big problems.

Seeking Professional Help

If you’re struggling to pay off credit card debt, seeking professional help can be a wise choice. Credit counseling agencies offer advice on managing debt and finances. These services are often free or low-cost and can provide personalized guidance.

Debt management plans (DMPs) are another option offered by credit counseling agencies. In a DMP, the agency negotiates with your creditors to lower interest rates and monthly payments. You then make a single payment to the agency, which distributes the funds to your creditors.

- Credit counseling: Expert financial advice

- Debt management plans: Negotiated lower rates

- Single monthly payment: Simplifies debt repayment

For more severe debt situations, you might consider debt settlement. Debt settlement companies negotiate with creditors to reduce the total amount you owe. Keep in mind this can affect your credit score and may have fees.

Bankruptcy should be a last resort but is sometimes necessary. Consulting a bankruptcy attorney can help you understand your options. Bankruptcy has long-term effects on your credit, so it’s important to fully understand the consequences.

Be cautious of scams. Always research any company or service thoroughly before committing. Seeking help can put you on the fast track to becoming debt-free and regaining control of your financial life.

Frequently Asked Questions

Managing credit card debt can be challenging, but understanding different strategies can help you become debt-free faster. Here are some commonly asked questions to guide you through the process.

1. What is the difference between the Debt Avalanche and Debt Snowball methods?

The Debt Avalanche method focuses on paying off debts with the highest interest rates first, which saves you money on interest over time. In contrast, the Debt Snowball method targets the smallest balances first, providing quick wins to boost motivation.

Both methods have their advantages. The Avalanche method is more cost-effective in terms of interest savings, while the Snowball method can be more motivating for those needing immediate progress. Choose the one that best fits your financial goals and personality.

2. Are balance transfer cards a good option for reducing credit card debt?

Balance transfer cards can be an effective way to reduce your credit card debt if used wisely. These cards often come with low or 0% introductory interest rates for a specific period, allowing you to pay down your principal faster without accruing new interest.

However, it’s essential to read the fine print and be aware of any balance transfer fees or terms. Ensure you pay off your transferred balance before the introductory period ends; otherwise, you could face high regular interest rates.

3. Should I close old credit card accounts after paying them off?

While it might seem logical to close old accounts once they’re paid off, it’s usually best to keep them open. Closing a credit card account can negatively impact your credit score by reducing your available credit limit and changing your credit utilization ratio.

If you’re concerned about overspending, consider keeping the account open but cutting up the physical card or storing it securely. This way, you’ll benefit from a better credit score without the temptation to incur more debt.

4. How do I deal with creditors if I can’t make my payments?

If you’re struggling to make minimum payments on your credit cards, contact your creditors immediately. Many companies offer hardship programs or other solutions like temporarily reduced payments or waived fees to assist customers facing financial difficulties.

A proactive approach can prevent further damage to your credit score and pave the way for manageable repayment plans tailored to your situation. Document all communications and agreements with creditors for future reference.

5.How often should I review my budget when trying to pay off debt?

If you’re focused on paying down debit quickly It’s wise to review budget monthly regularly looking” new opportunities cut cost redirect funds toward debit reduction aims ensuring stay track achieving goals seamlessly effectively satisfying avoiding as possible distraction inhibiting progress earned so far.< / p >

< p > A balanced budget takes into consideration anticipated upcoming expenses annual periodic allow diligent then both covering essentials remaining room productivity milestones celebrated benchmarks enhancing overall morale necessary tackling tasks associated rapidly timely basis ful-filingly impeccably admins completing end relieving burden fast .

Final Thoughts

Paying off credit card debt faster requires a well-thought-out strategy and consistent effort. Whether you choose the Debt Avalanche, Debt Snowball, or seek professional help, each method has its benefits. The key is to stay disciplined and monitor your progress.

Taking proactive steps like negotiating lower interest rates or consolidating debt can also significantly impact your repayment journey. By understanding and applying these strategies, you can achieve greater financial freedom and peace of mind.