Consider this: nearly 50% of adults admit to being concerned about their financial security as they approach retirement. Crafting a robust cashflow income plan can significantly alleviate these concerns. It’s a vital strategy to ensure a steady and reliable income stream that aligns with your future financial goals.

Historically, individuals relied heavily on pensions and social security for post-retirement income. However, with changing economic landscapes, developing a personalized income plan has become crucial. Integrating investments, savings, and other passive income sources is essential for sustained financial health and peace of mind.

Importance of a Cashflow Income Plan for Your Future

Planning your cashflow is like setting up a roadmap for financial success. It ensures you know where your money is coming from and where it’s going. This way, you avoid unpleasant surprises and can make informed decisions.

Without a solid cashflow plan, managing everyday expenses becomes challenging. Unexpected costs can derail your financial stability. A structured plan helps you navigate these challenges smoothly.

A good cashflow plan isn’t just about covering your immediate needs. It’s also about preparing for the future. By planning ahead, you can save for big milestones like buying a house or retiring comfortably.

Think of it as building a safety net. If an emergency arises, you’ll be prepared with a financial buffer. This decreases stress and allows you to focus on other important aspects of your life.

Role of Cash flow in Financial Planning

Cashflow plays a crucial role in effective financial planning. It helps you track income versus expenses, offering a clear picture of your financial health. Knowing this allows for better budgeting and saving strategies.

A well-managed cashflow can also lead to smarter investment decisions. When you know how much disposable income you have, investing becomes less risky. This accelerates wealth accumulation over time.

Moreover, consistent cashflow management builds creditworthiness. Good credit makes it easier to get loans with favorable terms for large purchases like a car or a home. This further secures your financial future.

Impact of Cashflow Planning on Future Financial Security

Cashflow planning directly impacts your future financial security. A reliable income stream ensures you can meet essential needs even during economic downturns. This makes your financial future more predictable and stable.

Planning your cashflow also helps in setting aside funds for retirement. A well-thought-out plan ensures you continue living comfortably even when you’re no longer working. This long-term thinking keeps you financially secure.

Furthermore, having a structured cashflow allows you to seize opportunities. Whether it’s a new investment or a spontaneous trip, you’re financially prepared to take advantage without disrupting your routine budget.

Role of Cashflow in Financial Planning

Cashflow management is essential to effective financial planning. It gives you a clear picture of your income and expenses, helping you make informed decisions. Without it, you might overspend and face financial trouble.

Good cashflow management means you have more money for investments. Investing wisely can help grow your wealth over time. It also reduces the risk of financial setbacks from unexpected expenses.

Effective cashflow planning helps you avoid debt. When you understand your cashflow, you can budget better. This helps you live within your means and save for future goals.

A stable cashflow enhances your creditworthiness. Banks and lenders see a well-managed cashflow as a sign of financial responsibility. This can lead to better loan terms and lower interest rates.

Tracking Income and Expenses

Tracking your income and expenses is the first step to managing your cashflow. It helps you see where your money is going. By categorizing expenses, you can identify areas to cut back on.

Use tools like spreadsheets or budgeting apps to stay organized. These can show you trends in your spending. They also make it easier to adjust your budget as your income changes.

Regularly updating your income and expense records is crucial. This keeps your financial planning current and accurate. It also helps you quickly spot any discrepancies or unexpected costs.

Benefits of Cashflow Forecasting

Cashflow forecasting helps you plan for the future. By predicting your income and expenses, you can prepare for upcoming financial needs. This foresight can prevent financial surprises.

Forecasting allows for better decision-making. You can plan for large purchases or investments without disrupting your financial stability. It also helps you set realistic financial goals.

Using online tools and software can make forecasting easier. They provide templates and automated calculations. This ensures your forecasts are accurate and up-to-date.

Adjustments and Flexibility

Adaptability is key in cashflow management. Your income and expenses can change, so your cashflow plan should be flexible. Regular reviews help keep your plan effective.

Set aside an emergency fund. This provides a cushion against unexpected expenses. It ensures your financial stability even in uncertain times.

Be willing to adjust your spending habits. Cut back on non-essential expenses when needed. This helps maintain a balanced cashflow and prevents debt.

Impact of Cashflow Planning on Future Financial Security

Effective cashflow planning ensures you meet your daily expenses without stress. It creates a financial backbone that supports your essential needs. This stability gives you peace of mind.

Planning your cashflow helps you build a substantial savings account. These savings act as a safety net for unexpected expenses or future investments. This boosts your long-term financial security.

A well-thought-out cashflow plan allows you to invest wisely. Investments grow your wealth and provide additional income streams. This enhances your financial position over time.

By consistently managing cashflow, you avoid unnecessary debt. Avoiding debt means you pay less in interest, allowing you to save more. This strengthens your overall financial health.

Components of a Cashflow Income Plan

An effective cashflow income plan comprises various components. These elements work together to ensure financial stability. Understanding these components is key to crafting a robust plan.

Salary and Bonuses form the primary source of income for most people. Steady employment offers predictable cash inflows. Bonuses can provide an additional boost.

Investment Returns play a significant role in boosting your cashflow. These can come from stock dividends, bond interest, or real estate profits. Investments can offer passive income that grows over time.

Passive Income Streams include earnings from activities like renting property or selling digital products. These sources require minimal effort to maintain. They add a diversified income to your cashflow plan.

Another crucial component is savings and emergency funds. Setting aside a portion of income for unexpected expenses can prevent financial stress. This safety net is essential for long-term stability.

Lastly, consider potential side hustles. Taking on freelance work or part-time gigs can increase your income. Side hustles provide flexibility and extra cashflow.

Salary and Bonuses

Salary is the most reliable source of income for many households. It provides a steady stream of money. This stability helps in managing monthly expenses.

Bonuses act as an additional financial boost. They can be linked to performance, company success, or special projects. This extra income can be used for savings or investments.

Understanding your salary structure is important. Know if it’s fixed or includes commissions and overtime pay. This helps in accurate cashflow planning.

Bonuses are often given during specific times of the year. For example, end-of-year bonuses are common. Knowing when to expect these can help plan larger expenses.

Both salary and bonuses can be channeled into different financial goals. Use them to build an emergency fund, pay off debt, or invest for the future. Strategic allocation can maximize financial security.

Investment Returns

Investment returns are a vital part of your cashflow plan. They provide an additional source of income. This income can come from stocks, bonds, or real estate.

One way to earn investment returns is through dividends. Dividends are payments made by companies to shareholders. They can be a steady source of passive income.

Another source of investment returns is interest from bonds. Bonds are loans you give to companies or governments. In return, you earn interest over time.

Real estate investments also offer returns. You can earn rental income from property. The property value can also increase over the years.

Monitoring your investment portfolio is crucial. Keep track of market trends and adjust your investments accordingly. This helps in maximizing your returns.

Passive Income Streams

Passive income streams are earnings you get with little to no effort. They can significantly boost your cashflow. These sources of income allow you to make money while focusing on other activities.

One popular passive income stream is rental property. By renting out real estate, you earn monthly rental payments. This provides a steady and reliable source of income.

Investing in dividend-paying stocks is another great way to earn passive income. Companies distribute a portion of their profits as dividends. This offers regular returns without selling your shares.

Earnings from online sales, like e-books or digital courses, also count as passive income. Once created, these products continue to generate revenue. You earn money every time someone makes a purchase.

Create a YouTube channel or blog that generates ad revenue.

- This requires initial effort but pays off over time.

. As more people visit your site, your ad revenue increases.

Strategy for Creating a Cashflow Income Plan

Creating a cashflow income plan involves several key steps. First, assess your current financial situation. Knowing your income and expenses is crucial.

Set clear financial goals for the near and distant future. This includes saving for emergencies, retirement, or major purchases.

- Identify short-term and long-term targets.

Next, develop a realistic budget. Track your income and categorize your expenses.

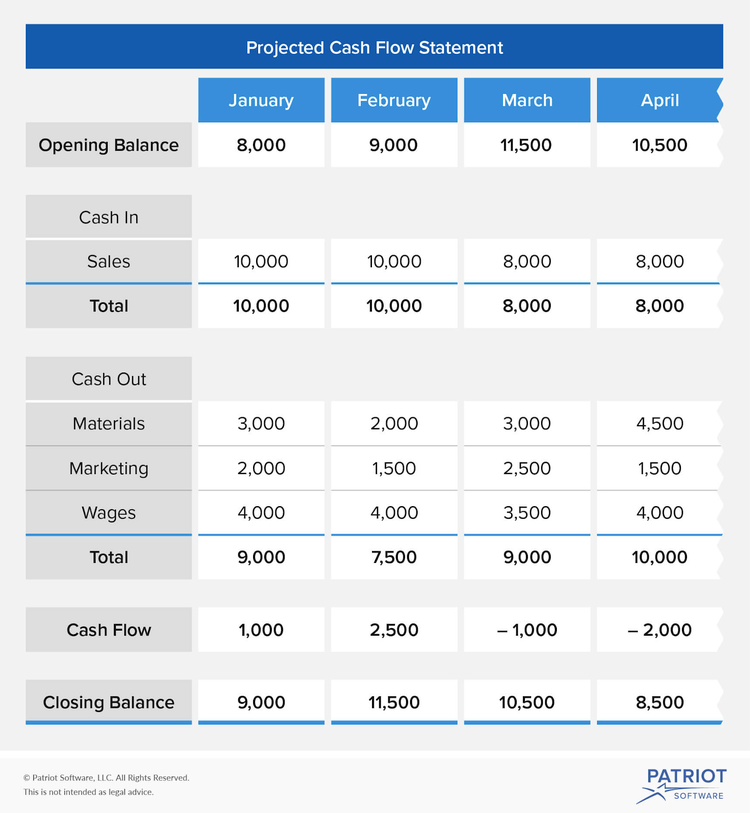

| Income | Expenses |

|---|---|

| Salary | Rent |

| Dividends | Utilities |

Diversify your income sources. Don’t rely solely on your primary job. Consider passive income streams, investments, and side hustles.

- Rental properties

- Dividend-paying stocks

Regularly review and adjust your plan. Life changes can affect your cashflow. Stay flexible to adapt to these changes. This ensures ongoing financial stability and success.

Setting Financial Goals for the Future

Setting financial goals is an important step in managing your money. It helps provide direction and focus. This makes your financial journey clearer and more attainable.

Start by identifying your long-term and short-term goals. Long-term goals might include buying a house or saving for retirement.

- Short-term goals could be building an emergency fund or paying off debt.

Break your goals into actionable steps. For example, if your goal is to save $10,000, determine how much to save each month. This makes big goals seem less overwhelming.

It’s essential to prioritize your goals. Focus on immediate needs first, like an emergency fund. Then, move on to future goals like investing or purchasing a home.

Regularly review your goals and progress. Life changes can affect your financial plans. Being flexible allows you to adjust as needed to stay on track.

Building a Budget Based on Cashflow Projections

Building a budget based on cashflow projections is a smart way to manage your finances. It allows you to plan your spending and saving effectively. This makes sure your money lasts longer.

Start by estimating your income. Include all sources like your salary, bonuses, and passive income. Make sure to account for any irregular income like freelance work or seasonal jobs.

List your fixed expenses first. These include rent, utilities, and loan payments.

- These costs remain constant each month.

Next, list your variable expenses. These can change each month, like groceries and entertainment. Keeping track of these helps you adjust your budget as needed.

Compare your total income to your total expenses. If expenses exceed income, find areas to cut back. Adjusting your budget ensures you stay financially stable.

Regularly review and update your budget. Life events and income changes can affect your cashflow. Updating your budget keeps it accurate and useful.

Maintaining and Adjusting your Cashflow Income Plan

Keeping your cashflow plan up to date is crucial. Life changes, and your plan needs to change with it. Regular reviews ensure it stays relevant.

Start by setting a schedule for reviews. Check your plan monthly or quarterly. This helps you spot issues early and make adjustments as needed.

Be ready to adjust your income sources. If you get a raise or pick up a side gig, update your plan. Extra income can help you reach your goals faster.

Expense tracking is also key. Identify areas where you can save more.

- Maybe you can cut back on dining out.

Small changes add up over time.

Use technology to help manage your cashflow. Budgeting apps and online tools can simplify the process. They provide clear visuals and alerts.

Communicate with family about your cashflow plan. Everyone should be on the same page about financial goals and plans. This teamwork ensures smoother adjustments.

Regular Review and Assessment of Cashflow Plan

Regularly reviewing your cashflow plan is essential for staying financially healthy. It helps you identify issues before they become major problems. This keeps your finances on track.

Set a timeline for these reviews. Monthly or quarterly checks work well for most people. Frequent reviews lead to better adjustments and financial decisions.

Use spreadsheets or budgeting tools to track your income and expenses. These tools make it easier to see trends and changes.

| Month | Income | Expenses |

|---|---|---|

| January | $3,000 | $2,500 |

| February | $3,200 | $2,700 |

During each review, assess your progress toward financial goals. Are you saving enough? Are you overspending? Answering these questions helps you stay on track.

Adjust your plan based on your findings. If expenses are rising, find ways to cut back.

- Maybe cook at home more often.

Small changes can have a big impact.

Finally, stay flexible. Life is unpredictable. Being willing to adjust keeps your plan effective and relevant.

Adapting Your Plan to Changes in Income or Lifestyle

Life is full of changes, and your cashflow plan should adapt to them. Whether it’s a new job or a new baby, these changes impact your finances. Being prepared helps you stay financially secure.

First, identify the change in your income or lifestyle. This could be a raise, job loss, or even moving to a new city. Understanding the change is crucial for making the right adjustments.

Next, revisit your financial goals. Adjust them based on your new situation.

- Maybe you need to save more for a bigger home.

Realign your goals to fit your new reality.

Update your budget to reflect these changes. If your income increases, decide how to best use the extra money. Extra income could go toward saving, investing, or paying off debt.

If your income decreases, find areas to cut back. Focus on essential expenses first. Reducing non-essential spending helps keep your budget balanced.

Keep your cashflow plan flexible. Life will continue to change, and your plan should evolve with it. Regular adjustments keep your finances on track and help you achieve your financial goals.

Frequently Asked Questions

Cashflow income planning is crucial for securing your financial future. Here, we answer common questions to help you understand how to create and maintain an effective plan.

1. What is the importance of diversifying income sources?

Diversifying income sources reduces financial risk. If one source dries up, you have others to rely on. This stability allows for more confident planning.

Having multiple streams can also accelerate wealth growth. Whether it’s investments, side hustles, or rental income, these contribute to a stronger financial foundation.

2. How often should I review my cashflow plan?

Review your cashflow plan at least once every quarter. Regular reviews help catch issues early and allow timely adjustments.

If major life events occur, such as a job change or new expenses, review it immediately. Keeping your plan updated ensures ongoing accuracy and relevance.

3. Can technology assist in managing my cashflow plan?

Yes, many apps and software tools are available for this purpose. They can track income and expenses automatically, making management easier.

These tools often provide insights into spending patterns and offer suggestions for budgeting improvements. Using technology can enhance the efficiency of your financial planning.

4. What steps should I take if my income decreases suddenly?

If your income drops unexpectedly, first assess non-essential expenses you can cut back on immediately. This quick action helps stabilize your budget short-term.

Next, consider temporary ways to boost income like freelancing or part-time work until things improve. Staying flexible helps navigate financial downturns effectively.

5. How do I factor large purchases into my cashflow plan?

Plan for large purchases by setting aside funds well in advance. Allocate a portion of your monthly savings toward this goal to make it manageable over time.

This method prevents sudden strain on your finances and allows you to achieve big goals without disrupting other financial commitments.

Conclusion

Creating a cashflow income plan is essential for long-term financial security. It requires assessing your income, setting goals, and regularly reviewing your plan. This helps you stay on track and adapt to financial changes.

By diversifying income sources and using technology, you can enhance your planning. Regular adjustments ensure your plan stays effective. This proactive approach protects your financial health and helps achieve your future goals.