Creating an Investment Policy Statement (IPS) is akin to designing the blueprint of your financial future— did you know that 90% of investors feel more confident when they have a clear investment strategy? An IPS serves as a comprehensive guide that aligns your investment goals with your risk tolerance and time horizon. Let’s delve into the nuances that make crafting an IPS both an art and a science.

The concept of an IPS has evolved significantly over the years, driven by the increasingly complex financial landscape. Originally designed for institutional investors, today it’s an indispensable tool for individual investors as well. According to a recent survey, portfolios with a well-articulated IPS tend to outperform those without by almost 2% annually, showcasing its effectiveness.

- Identify your financial goals to guide your investment decisions.

- Establish an investment timeframe, considering whether your goals are short-term or long-term.

- Determine your risk tolerance by assessing how much risk you can comfortably handle.

- Select diverse investment categories like stocks, bonds, and real estate to balance risk and reward.

- Set guidelines for regular portfolio rebalancing and review to maintain alignment with your objectives.

Decoding the Importance of an Investment Policy Statement

An Investment Policy Statement (IPS) is your financial roadmap. It helps you stay focused on your goals. Without an IPS, you might make decisions based on emotions, which isn’t always best for your investment future.

One crucial aspect of an IPS is that it clearly defines your investment strategy. This includes how much risk you’re willing to take and what types of investments you prefer. Clarity in your strategy ensures that your actions align with your long-term goals.

Having a well-structured IPS can also save you from impulsive decisions. For instance, during market downturns, an IPS guides you to stick to your plan rather than panic-selling. Sticking to a defined strategy often results in better long-term performance.

Another benefit is that an IPS provides a benchmark for evaluating your portfolio’s performance. It offers a set of guidelines for when to rebalance your portfolio. Regular reviews help keep your investments aligned with your evolving goals and market conditions.

The role of an Investment Policy Statement

An IPS acts as a safety net for your investments. It sets clear rules and expectations. This structure can bring peace of mind, knowing you have a plan in place.

It’s also essential for financial advisors who manage your investments. An IPS provides them a clear understanding of your preferences and goals. This ensures their decisions align with your objectives.

Furthermore, having an IPS helps in setting realistic expectations. It outlines potential returns and risks. Understanding these factors can prevent disappointment and keep you on track towards your financial goals.

Understanding the components of an Investment Policy Statement

An IPS typically includes several key components. First, it starts with your investment objectives. This can range from saving for retirement to buying a house.

Next, it outlines your risk tolerance. Knowing how much risk you can handle is crucial. Too much risk can lead to stress, while too little might mean not meeting your financial goals.

Finally, it will detail your asset allocation. This is how your money is divided among different investments. A diversified portfolio helps spread risk and can lead to more stable returns.

The benefits of utilizing an Investment Policy Statement

One of the main benefits of an IPS is the discipline it brings. It encourages consistent, goal-oriented investing. This approach helps in avoiding common pitfalls, like chasing hot stocks.

Another benefit is improved communication with your financial advisor. With a clear IPS, you’re both on the same page. This clarity can result in better investment decisions.

An IPS also allows for easier portfolio reviews. It offers clear criteria for assessing performance. Regular reviews ensure your investment strategy remains effective and aligned with your goals.

The role of an Investment Policy Statement

An Investment Policy Statement (IPS) is like a compass for your financial journey. It sets out the rules for making investment decisions. This helps you stay on course even when market conditions change.

One important role of an IPS is to clarify your financial goals. Whether you’re saving for retirement or a new home, knowing your goals is crucial. Clear goals guide your investment strategy.

Another key role is managing risk. An IPS outlines how much investment risk you are willing to take. This keeps you from making risky choices that could harm your portfolio.

Finally, an IPS is useful for communication. It ensures everyone involved in managing your money understands your preferences. This reduces misunderstandings and aligns efforts toward your financial objectives.

Defining Financial Goals

An IPS helps you set clear financial goals. These goals could include retirement, saving for education, or buying a home. Clear goals make it easier to plan your investments.

Without defined goals, it’s easy to get distracted. You might chase hot stocks or make impulsive decisions. An IPS keeps your focus on long-term objectives.

Clear goals also make it simpler to measure your progress. You can track how well your investments are doing. This helps you adjust your strategy when needed.

Managing Investment Risks

Risk management is crucial in investing. An IPS specifies your risk tolerance. This helps you avoid taking on more risk than you’re comfortable with.

Understanding your risk tolerance prevents panic during market downturns. An IPS outlines what to do when things go wrong. This prepares you for various market conditions.

Moreover, your IPS can include steps for diversification. Spreading your investments across different assets can minimize risk. This approach can make your investment journey smoother.

Improving Communication

Effective communication is key when multiple people manage your money. An IPS serves as a written document that everyone can refer to. This ensures all parties are on the same page.

A financial advisor can better tailor advice if they understand your IPS. They will know your risk tolerance and goals. This alignment makes for more coherent and effective advice.

Additionally, having an IPS reduces the chances of misunderstandings. Clear guidelines mean fewer conflicts about investment decisions. This leads to a more harmonious investment experience.

Understanding the components of an Investment Policy Statement

An effective Investment Policy Statement (IPS) includes several key components. First, you need to define your investment objectives. These are your financial goals, like retirement or buying a house.

Another crucial component is your risk tolerance. This measures how much risk you’re willing to take with your investments. Knowing your risk tolerance helps prevent panic during market downturns.

You’ll also need to specify your asset allocation. This outlines how you’ll divide your money among different types of investments. Diversification helps spread risk and can lead to more stable returns.

Finally, the IPS should include guidelines for portfolio rebalancing. This means adjusting your investments to maintain your desired level of risk. Regular reviews ensure your portfolio remains aligned with your goals.

The benefits of utilizing an Investment Policy Statement

One major benefit of an Investment Policy Statement (IPS) is the discipline it brings to your investing process. It sets clear guidelines for your investment decisions. This helps you avoid making impulsive choices based on market fluctuations.

An IPS also provides a structured approach to achieving your financial goals. By outlining your objectives and risk tolerance, it ensures your investments align with your long-term plans. This structured approach often results in better performance over time.

Furthermore, an IPS enhances communication with your financial advisor. It serves as a reference point that both you and your advisor can consult. This ensures consistency in the investment strategy.

Another advantage is that an IPS helps in monitoring and reviewing your investment performance. Clear benchmarks allow you to measure progress effectively. This makes it easier to identify when adjustments are needed.

An IPS can also reduce stress during market volatility. Knowing you have a plan in place can be reassuring. Sticking to your pre-defined strategy helps you stay calm and focused.

Finally, an IPS offers flexibility for future adjustments. Financial goals and market conditions can change over time. Regular reviews and updates ensure your IPS remains relevant to your evolving needs.

Guiding Steps to Design an Investment Policy Statement

Designing an Investment Policy Statement (IPS) involves several crucial steps. First, identify your financial goals. These could range from saving for college to preparing for retirement.

Next, establish an investment timeframe. Your goals might be short-term or long-term. Knowing the timeframe helps in choosing the right investment types.

Another important step is asserting your risk tolerance. Consider how much risk you’re willing to face. This will guide your asset allocation.

Once you’ve set your risk tolerance, select your investment categories. Diversifying your portfolio is key. It helps in spreading risk and maximizing returns.

Portfolio rebalancing and review should also be part of your IPS. Market conditions change, and so could your goals. Regular reviews ensure your portfolio stays aligned with your objectives.

- Identifying financial goals

- Establishing an investment timeframe

- Asserting risk tolerance

- Selecting investment categories

- Portfolio rebalancing and review

Step 1: Identifying Your Financial Goals

Identifying your financial goals is the first step in creating an effective Investment Policy Statement (IPS). These goals will guide every investment decision you make. Clear, specific goals provide direction and purpose for your investments.

Start by asking yourself what you want to achieve financially. Are you saving for retirement, a new home, or your child’s education? Understanding your objectives will help shape your investment strategy.

Financial goals can be categorized into short-term and long-term objectives. Short-term goals might include things like saving for a vacation. Long-term goals could be getting ready for retirement or buying a house.

It’s essential to quantify your goals. Specify the amount of money you need and the timeline for achieving it. Having measurable goals makes it easier to monitor your progress.

Once your goals are clear, write them down. This makes your objectives tangible and easier to stick to. Written goals serve as a constant reminder of what you’re working towards.

- Define specific financial goals

- Classify into short-term and long-term

- Quantify your goals

- Write them down for reference

Step 2: Establishing an Investment Timeframe

Establishing an investment timeframe is crucial for your Investment Policy Statement (IPS). Your timeframe will impact your investment choices and strategies. Knowing how long you have to meet your goals helps in selecting appropriate investments.

An investment timeframe can be short, medium, or long-term. Short-term usually refers to less than three years, medium-term is between three and ten years, and long-term exceeds ten years. Different timeframes suit different types of investments.

If you have a short-term goal, like buying a car next year, safer investments are recommended. These might include savings accounts or short-term bonds. They offer lower returns but are less risky.

For medium-term goals like saving for a child’s college fund, moderate-risk investments may be suitable. This could include balanced mutual funds or a mix of stocks and bonds. These options aim for growth while managing risk.

Long-term goals such as retirement allow you to take more risks for potentially higher returns. Stocks or real estate are popular choices. Over time, these investments usually offer higher returns despite market fluctuations.

- Short-term: less than 3 years

- Medium-term: 3-10 years

- Long-term: more than 10 years

Step 3: Asserting Risk Tolerance

Asserting your risk tolerance is a critical step in creating an Investment Policy Statement (IPS). Risk tolerance refers to how much risk you’re willing to take with your investments. Knowing this helps you make informed decisions that align with your comfort level.

Your risk tolerance can be influenced by various factors, including age, financial situation, and investment goals. For example, younger investors might have a higher risk tolerance. They have more time to recover from potential losses.

On the other hand, older investors might prefer safer investments. They are closer to retirement and can’t afford significant losses. Choosing low-risk investments like bonds might be more suitable for them.

To assess your risk tolerance, consider your emotional reactions to market fluctuations. If you find yourself stressed during market downturns, you might have a low risk tolerance. Conversely, if you’re comfortable with volatility, a higher risk tolerance may suit you.

Understanding your risk tolerance helps in diversifying your portfolio effectively. Diversification spreads out risk by investing in different asset types. This strategy can lead to more stable returns over time.

- Consider your age and financial situation

- Factor in your investment goals

- Assess your emotional reactions to market changes

- Use risk tolerance to diversify your portfolio

Step 4: Selecting Investment Categories

Selecting the right investment categories is pivotal in your Investment Policy Statement (IPS). Investment categories help diversify your portfolio and manage risk. They ensure you have a balanced approach to meeting your financial goals.

Stocks are a common investment category. They offer high returns but come with higher risk. Stocks are ideal for long-term goals where you can tolerate short-term volatility.

Bonds are another popular option. They are generally safer than stocks but provide lower returns. Bonds are suitable for short to medium-term goals.

Real estate is also a valuable investment category. It provides steady income through rents and can appreciate over time. However, it may require more initial capital and management.

Mutual funds and ETFs (Exchange-Traded Funds) offer a mix of assets. They provide diversification in a single investment. These are suitable for investors looking for a balanced approach.

- Stocks: High return, high risk

- Bonds: Lower return, lower risk

- Real estate: Steady income, potential for appreciation

- Mutual funds and ETFs: Diversification in one investment

Step 5: Portfolio Rebalancing and Review

Portfolio rebalancing and review are essential for maintaining your investment strategy. Over time, market fluctuations can shift your asset allocation. Rebalancing helps you stay on track with your original goals.

Rebalancing involves buying and selling assets to restore your desired portfolio mix. For example, if stocks outperform bonds, you might need to sell some stocks and buy bonds. This keeps your risk level consistent.

Regular review of your portfolio is also important. Set a schedule to review your investments, such as quarterly or annually. This helps you catch any imbalances early and make necessary adjustments.

During your review, compare your portfolio’s performance against your IPS. Check if your investments are meeting your financial goals. If not, consider making changes to your strategy.

Rebalancing and review can be automated or done manually. Some financial advisors offer rebalancing services. Automated tools can simplify the process and ensure it happens on schedule.

- Determine a rebalancing schedule (quarterly, annually)

- Buy and sell assets to maintain target allocation

- Check portfolio performance against goals

- Consider automated tools or advisor services

Common Mistakes to Avoid While Creating an Investment Policy Statement

One common mistake is failing to clearly define your financial goals. Without clear goals, it’s hard to measure progress. Make sure your goals are specific and achievable.

Another mistake is not considering your risk tolerance. Ignoring risk can lead to investments that make you uncomfortable. Assess your risk tolerance honestly to make appropriate choices.

Many people forget to review and update their IPS regularly. Life changes and so do financial goals. Review your IPS at least once a year to ensure it stays relevant.

Some investors overlook the importance of diversification. Putting all your money in one type of investment can be risky. Diversify to spread out the risk and achieve more stable returns.

Another mistake is not involving all stakeholders, like financial advisors or family members, in the IPS creation. Their input can provide valuable insights. Collaborating ensures everyone is on the same page.

- Clearly define financial goals

- Consider risk tolerance

- Regularly review and update your IPS

- Diversify your investments

- Involve all stakeholders

Getting Professional Help in Formulating an Investment Policy Statement

Seeking professional help can make creating an Investment Policy Statement (IPS) easier. Financial advisors have the expertise to guide you. They can help you define clear financial goals and assess your risk tolerance.

A professional can also assist in selecting the right investment categories for you. They understand market trends and can make informed recommendations. This ensures your portfolio is well-balanced and aligned with your goals.

Financial advisors also help with regular reviews and rebalancing of your portfolio. They will monitor your investments and suggest adjustments when necessary. This ongoing support keeps your investments on track.

An advisor can also save you time and reduce stress. Managing investments can be overwhelming. Having a professional on your side lets you focus on other important aspects of your life.

Engaging a professional can provide a fresh perspective. They can uncover opportunities you might have missed. This outside viewpoint adds value to your investment strategy.

- Expert guidance in defining goals

- Informed investment recommendations

- Regular reviews and rebalancing

- Time-saving and stress reduction

- Fresh perspective on opportunities

Frequently Asked Questions

Creating an Investment Policy Statement (IPS) can seem complicated, but it doesn’t have to be. Below are some common questions and their answers to help guide you through the process.

1. What is an Investment Policy Statement?

An Investment Policy Statement (IPS) is a document that outlines your investment goals and strategies. It also includes guidelines for how your investments should be managed over time.

Having an IPS helps keep you focused on your long-term objectives, even during market fluctuations. It’s crucial for both individual investors and financial advisors to ensure alignment with financial goals.

2. Why is risk tolerance important in an IPS?

Your risk tolerance determines how much market volatility you can handle without panicking or making poor decisions. Knowing this helps shape your portfolio in a way that matches your comfort level with risk.

A well-balanced IPS considers your risk tolerance, ensuring you’re not taking unnecessary risks or being too conservative. This balance aids in achieving stable long-term returns while minimizing stress during volatile periods.

3. How often should I review my Investment Policy Statement?

You should review your IPS at least once a year or whenever significant changes occur in your life, like getting married or retiring. Regular reviews ensure that your investment strategy remains aligned with your changing needs and goals.

This practice helps identify any imbalances in your portfolio early on, allowing for timely adjustments. Staying updated ensures that you’re always moving towards your financial objectives effectively.

4. Can I create an IPS without professional help?

Yes, you can create an IPS on your own by following structured guidelines and utilizing online templates. However, consulting a financial advisor can add value by providing expert insights tailored to your specific situation.

An advisor’s experience can help identify opportunities and potential pitfalls you might miss. Their guidance assures that all critical aspects of the IPS are covered comprehensively.

5. What are the main components of a good IPS?

A solid IPS includes defined financial goals, asset allocation strategy, risk tolerance assessment, and guidelines for regular review and rebalancing of the portfolio.

These components work together to form a roadmap for managing investments effectively over time. By addressing each area carefully, an IPS enhances the likelihood of achieving long-term success in meeting financial objectives.

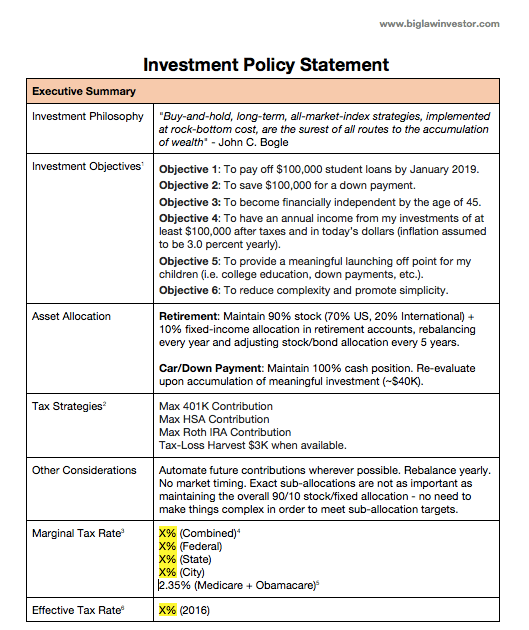

Investment Policy Statement – What, Why, and How To Write

Conclusion

Creating an Investment Policy Statement is essential for aligning your financial goals and strategies. It provides a clear framework for investment decisions, ensuring consistency and focus. For both individual investors and advisors, an IPS serves as a reliable guide through market fluctuations.

Regularly reviewing and updating your IPS ensures it remains relevant and effective. By defining objectives, assessing risk tolerance, and selecting appropriate investments, you set a strong foundation for financial success. An IPS not only helps in achieving goals but also offers peace of mind.