Over 50% of credit card users don’t know their interest rates, leading to debt spirals that are difficult to escape. How often have you glanced at your statement and winced at the charges piling up? Understanding how to use credit cards responsibly can transform these tools from debt traps into powerful financial assets.

Historically, credit cards became mainstream in the 1950s but with their rise came the lure of instant gratification. A key to responsible usage is paying off the full balance each month—data shows a significant drop in debt for those who do. Another vital aspect is keeping track of your spending, which helps avoid unpleasant surprises when the bill arrives.

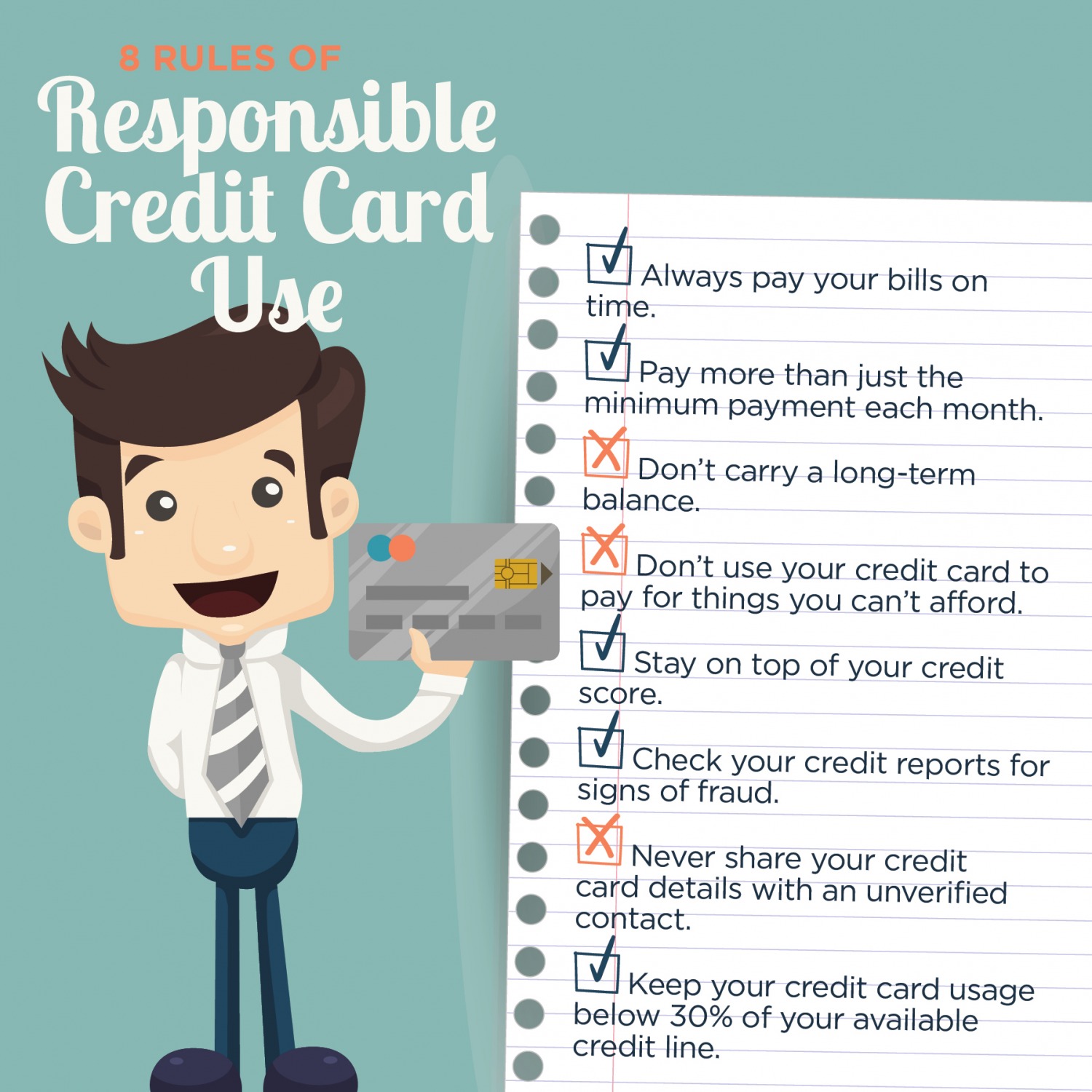

- Understand and adhere to your credit card terms and conditions.

- Pay off your balance in full each month to avoid interest charges.

- Keep your credit utilization ratio below 30%.

- Monitor your statements regularly for errors or unauthorized transactions.

- Avoid making only the minimum payment to prevent accumulating high-interest debt.

Recognizing the Purpose and Role of Credit Cards

Credit cards are not just for buying things; they offer several benefits when used correctly. For instance, they can help build your credit score, which is crucial for loans. By making timely payments, you show lenders that you’re responsible.

Credit cards also provide a safety net in emergencies. Imagine your car breaks down, and you don’t have cash on hand. A credit card can cover these unexpected expenses.

Additionally, many credit cards offer rewards programs. These might include cash back, travel points, or discounts at your favorite stores. Using these rewards can save you money on everyday purchases.

Understanding your credit card’s purpose helps you use it wisely. It’s not just for buying now and paying later. It’s a tool that, when managed properly, can enhance your financial stability.

Understanding Credit Card Terms and Conditions

Before using a credit card, it’s essential to read and understand its terms and conditions. These terms outline important details like interest rates, fees, and repayment schedules. Knowing these can save you from unpleasant surprises down the road.

Interest Rates

Interest rates determine how much extra you’ll pay if you don’t clear your balance each month. They are often expressed as an annual percentage rate (APR). It’s crucial to understand how the APR works for different transactions like cash advances and purchases.

Some cards offer introductory rates that may be lower but increase after a certain period. Always check the length of this introductory period. A higher APR can significantly increase your debt if you’re not careful.

To find the best card for you, compare interest rates across multiple options. Websites like [NerdWallet](https://www.nerdwallet.com/) offer easy comparisons. Being informed can help you avoid high-interest traps.

Fees and Penalties

Credit cards often come with various fees that can add up quickly. These may include annual fees, late payment fees, and over-limit fees. Avoiding these charges starts with understanding them.

Some credit cards waive certain fees, but you need to know the conditions. Always read the fine print to see if these benefits apply to you. This can save you money and stress in the long run.

If you are hit with a fee, sometimes contacting customer service can result in a one-time waiver. Explaining your situation politely can often yield positive results. It’s always worth asking.

Rewards and Points

Many credit cards offer rewards programs to incentivize their use. These rewards can include cashback, travel miles, or points for spending. Understanding how to maximize these rewards can turn them into significant savings.

Look for cards that match your spending habits. For instance, if you frequently travel, a card with travel rewards might be ideal. Matching the card to your needs ensures you’re getting the most benefit.

Also, be aware of the expiration dates for points or miles. Not using them on time can result in losing valuable rewards. Regularly monitor your rewards balance to make the most of your credit card’s benefits.

The Role of Credit Limits and Their Management

Credit limits play a significant role in how you use your credit card. They represent the maximum amount you can borrow at any time. Staying within this limit shows responsible usage and can positively impact your credit score.

It’s crucial to know that credit limits are set based on various factors, including your income and credit history. Lenders assess these elements to determine a safe borrowing limit. If your limit is too low, you might request an increase as your financial situation improves.

Managing your credit limit involves keeping track of your spending. Exceeding your limit can lead to penalties and higher interest rates. Utilizing tools like budgeting apps can help you stay within your limit and avoid unnecessary fees.

Avoid maxing out your credit card frequently, as this can lower your credit score. Higher credit utilization rates are seen as risky by lenders. Aim to use only a small portion of your available credit to maintain a healthy financial profile.

Proactive and Timely Bill Payments

Paying your credit card bill on time is crucial for maintaining a good credit score. Late payments can lead to hefty fees and negatively impact your credit history. Setting up alerts or reminders can help you avoid missing payment due dates.

One effective method is to set up automatic payments. Many credit card companies offer this service, withdrawing the amount directly from your bank account. This ensures that your bills are paid even if you forget.

Another approach is to pay your bill in full each month. This way, you avoid paying interest on the carried-over balance. It also keeps your overall debt level manageable.

- Set up payment alerts

- Utilize automatic payment options

- Strive to pay in full monthly

It’s also beneficial to review your billing statement regularly. Checking for errors or possible fraudulent activities keeps your account secure. Addressing any discrepancies immediately ensures accurate billing and protects your finances.

Lastly, if you’re unable to pay the full amount, at least make the minimum payment. This can prevent late fees and a serious drop in your credit score. However, aim to pay more than the minimum whenever possible to reduce your debt faster.

Balancing Spending and Repayment Strategies

Managing how much you spend on your credit card is essential for financial health. Always spend within your means to avoid accumulating debt. Creating a budget can help you track your spending and stay within limits.

Paying your balance in full each month is a wise strategy. It prevents interest from piling up and keeps your debt manageable. If paying in full isn’t possible, always aim to pay more than the minimum amount due.

Using credit cards for essential, planned purchases rather than impulsive buys is key. This approach ensures you can repay what you owe easily. It also avoids the temptation of unnecessary spending.

Setting financial goals can help balance spending and repayment. For example, save up for a big purchase rather than using your credit card. Always prioritize needs over wants to maintain a healthy financial status.

- Create a monthly budget

- Use credit cards for planned purchases

- Set financial goals to manage spending

Lastly, continuously monitor your credit card statements. Checking your statements regularly prevents fraud and helps you stay aware of your spending habits. Being mindful of your expenses is crucial for balancing spending and repayment effectively.

Maintaining a Low Credit Utilization Ratio

Your credit utilization ratio is a key factor in your credit score. It represents the percentage of your credit limit that you’re using. Keeping this ratio low shows lenders that you’re financially responsible.

Ideally, you should aim to use no more than 30% of your available credit. For example, if your credit limit is $1,000, try to keep your balance below $300. This low utilization can help boost your credit score.

One way to manage this is by paying off your balances in full each month. This not only avoids interest but also keeps your utilization low. If you can’t pay the full amount, try to at least make multiple payments throughout the month.

- Aim for a utilization ratio below 30%

- Pay off balances in full monthly

- Make multiple payments to manage balance

Requesting a credit limit increase can also help lower your utilization ratio. Just make sure you don’t increase your spending after getting a higher limit. Maintaining your spending habits and keeping your balance low will benefit your financial health.

Lastly, regularly monitor your credit card statements. This helps you keep track of your spending and ensures you stay within your target ratio. Regular checks make it easier to adjust your habits if needed.

Avoiding the Temptation of Minimum Payments

Minimum payments might seem like a tempting option when you’re low on cash. However, sticking to just the minimum can lead to accumulating high-interest debt. Paying only the minimum increases the amount of interest you owe.

It’s crucial to pay more than the minimum whenever possible. This will help reduce your overall debt faster and save you money on interest. Even small additional payments can make a significant difference over time.

Developing good payment habits is essential for financial stability. Start by setting up automatic payments that exceed the minimum amount due each month. This ensures you’re consistently reducing your balance.

- Set automatic payments above the minimum

- Make extra payments whenever possible

- Avoid using your card for non-essential purchases

If you find it challenging to pay more, consider reviewing your spending habits. Cutting down on unnecessary expenses can free up funds for higher credit card payments. Focus on needs over wants to help divert funds toward paying off debt.

Regularly reviewing your monthly statements can also keep you informed about how much you’re paying in interest. Knowing these details helps you stay motivated to clear your balances faster. Awareness promotes responsible spending and repayment behaviors.

Benefits of Regularly Monitoring Credit Card Statements

Regularly checking your credit card statements is crucial for responsible credit card use. It helps you keep track of your spending and ensures you’re staying within your budget. Monitoring your statements can prevent overspending and accumulating unnecessary debt.

By reviewing your monthly statement, you can also detect any fraudulent activities. Catching unauthorized transactions early can save you a lot of trouble. Report any suspicious charges to your credit card company immediately.

Monitoring statements allows you to verify that all charges are accurate. Sometimes errors can occur, and you might be charged for something you didn’t purchase. Regular checks help you catch these mistakes and resolve them promptly.

- Track your spending

- Detect fraudulent activities early

- Verify charges for accuracy

Another benefit is understanding your spending habits better. Reviewing your statements can reveal patterns in your expenses. This insight can help you make informed decisions and adjust your budget as needed.

Lastly, keeping an eye on your statements can aid in managing your credit utilization ratio. You can see how much of your available credit you’re using and make payments accordingly. Maintaining a low credit utilization ratio is vital for a healthy credit score.

Frequently Asked Questions

Credit cards can be powerful financial tools if used responsibly. Below are some common questions and answers to help you understand how to make the best use of your credit card.

1. What is a credit utilization ratio?

The credit utilization ratio is the percentage of your total available credit that you’re currently using. It’s calculated by dividing your total credit card balances by your total credit limits. A lower ratio, ideally below 30%, is better for your credit score.

Maintaining a low utilization ratio shows lenders that you manage your finances well. Regularly monitoring this ratio can help you make smart spending decisions to keep it low, thus improving or maintaining a good credit score.

2. Why is it important to pay more than the minimum payment?

Paying only the minimum will result in high-interest charges accumulating over time. This increases the amount you owe significantly and can take years to pay off even small amounts.

By paying more than the minimum, you reduce your principal balance faster and save on interest costs. This not only helps clear your debt quicker but also positively impacts your credit score.

3. How can automatic payments help with managing my credit card?

Setting up automatic payments ensures that you never miss a payment due date, which helps avoid late fees and penalties. It also contributes positively to your payment history, which is a big factor in calculating your credit score.

You can usually specify an amount higher than the minimum for these payments. This strategy ensures you’re consistently reducing debt while avoiding late charges and maintaining good standing with creditors.

4. What should I do if I notice unfamiliar charges on my statement?

If you spot unfamiliar charges on your statement, contact your credit card issuer immediately to report them. They can investigate those charges and may suspend or close the compromised account.

Your issuer might provide a temporary refund while investigating, which protects you from paying for fraudulent transactions out of pocket. Always monitor statements regularly to catch such issues early.

5. Are rewards programs worth it?

If used wisely, rewards programs can offer substantial benefits ranging from cashback to travel points and discounts on everyday purchases. To maximize these rewards, ensure that you’re not spending more than usual just to earn points or bonuses.

Selecting a rewards program that aligns with your regular spending habits maximizes benefits without overspending or incurring extra fees. This approach enables you to gain additional value from everyday transactions while keeping within budget limits.

Conclusion

Effectively using credit cards can significantly benefit your financial health. By understanding terms, managing credit limits, and making proactive payments, you can avoid common pitfalls. Regularly monitoring statements also helps in safeguarding against fraud.

Balancing spending and repayment is key to maintaining a low credit utilization ratio and avoiding debt accumulation. Applying these tips ensures that your credit card remains a valuable tool rather than a financial burden.