A significant number of startups have taken their first steps using credit cards as a funding source. This unconventional approach leverages the flexibility and instant access to capital that credit cards provide, enabling founders to cover immediate expenses and invest in critical business needs. However, this route demands a meticulous strategy to avoid pitfalls and financial setbacks.

The history of using credit cards for business funding goes back decades, but it gained traction during financial crises when traditional funding sources dwindled. According to a 2022 Small Business Survey, approximately 29% of entrepreneurs have used personal credit cards to finance their ventures. This highlights the importance of understanding credit card management to optimize this financial tool while minimizing risks.

- Assess your financial needs and create a detailed budget.

- Improve your credit score to secure better interest rates and higher limits.

- Research and choose a credit card with favorable terms and rewards.

- Use the card responsibly for essential business expenses only.

- Regularly monitor expenses, maintain low credit utilization, and pay off balances promptly.

Evaluating the Option: Credit Cards for Startup Funding

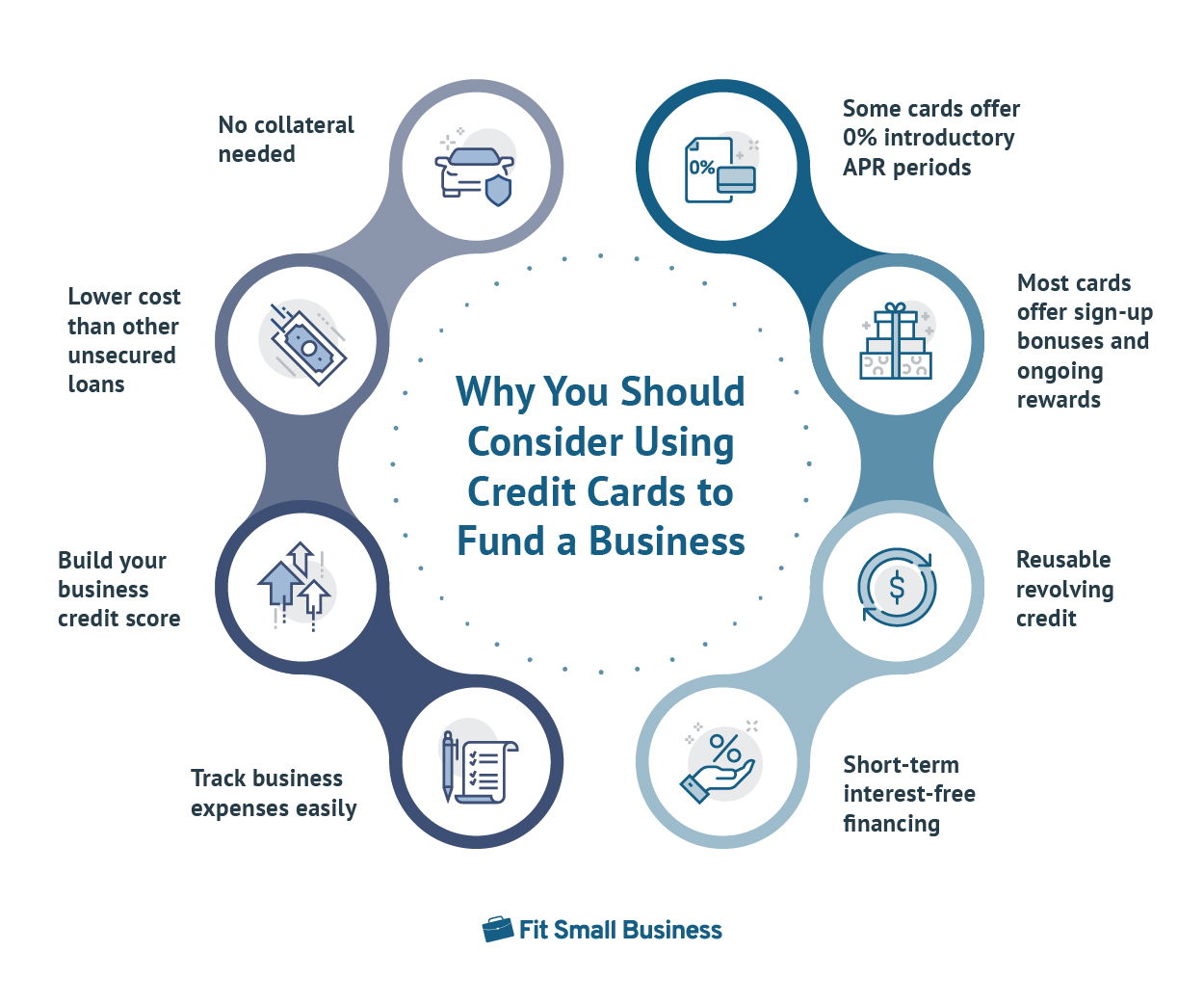

Using credit cards to fund a startup can be a quick way to access necessary capital. This method offers instant access to funds, which can be crucial for covering initial expenses. However, it’s important to weigh the pros and cons thoroughly.

Advantages of Using Credit Cards

One major advantage is the ability to make immediate purchases without waiting for loan approvals. Additionally, many credit cards offer rewards or cashback, which can provide added benefits for your business. These perks can help offset some costs.

Another benefit is the flexibility in managing cash flow. Credit cards can bridge financial gaps, especially during slow periods. This can keep your business running smoothly.

Some credit cards come with a low or 0% introductory APR. This allows startups to borrow without paying high interest rates initially. However, these terms are often temporary.

Disadvantages of Using Credit Cards

The biggest drawback is the potential for high interest rates. If balances are not paid off quickly, debt can accumulate rapidly. This can become a financial burden.

Credit cards also come with credit limits that might be lower than other funding options. This could restrict the amount of capital available. It’s essential to plan your expenses carefully.

Additionally, relying heavily on credit cards can affect your personal credit score. Any missed payments or high balances could lead to a lower credit rating, making future funding harder to secure.

Potential Risks Involved

Using credit cards involves significant financial risk. Mismanagement of funds can lead to overwhelming debt. This can jeopardize both personal and business finances.

There are also operational risks. High levels of debt can restrict your startup’s ability to grow. This can limit reinvestment opportunities and affect long-term sustainability.

It’s crucial to have a clear repayment plan. Without one, the financial risks can escalate quickly. This could lead to severe consequences for your startup.

Getting Started: How to Prepare Beforehand

Preparing before using credit cards to fund your startup is crucial. This ensures you manage your finances effectively. It can also help you avoid potential pitfalls.

Determining Your Financial Needs

First, you need to assess the amount of money your startup will require. List out all initial and ongoing expenses. This will provide a clear picture of your financial needs.

Be realistic about your projections. Overestimating can lead to unnecessary debt, while underestimating can cause financial strain. Accurate estimates are key.

Consider creating a detailed budget. This helps to plan for unforeseen expenses and ensures you have the necessary funds. Budgeting is a vital step in financial planning.

Improving Your Credit Health

Having a good credit score is essential when using credit cards for funding. It impacts the credit limit and interest rates you’ll receive. Aim to improve your score before applying.

Pay off existing debts to boost your credit health. Keep your credit utilization low. This makes you a more attractive borrower to credit card companies.

Review your credit report regularly. This helps you spot and correct errors. Maintaining a good credit score is beneficial for your startup.

Researching Suitable Credit Card Options

Not all credit cards are created equal. Research various options to find the one that best suits your needs. Consider factors like interest rates, fees, and rewards.

Some credit cards offer promotional 0% APR periods. These can be advantageous for making large purchases without immediate interest. However, be mindful of when the promotional period ends.

Check for additional benefits like cashback or travel rewards. These can add value to your business expenses. Choose a card that aligns with your spending habits.

Selecting the Right Credit Card

Choosing the right credit card is vital for your startup’s financial health. Different cards offer diverse benefits and terms. Selecting the right one can help maximize your cash flow and minimize debt.

Begin by looking at interest rates. Some cards come with high rates, while others offer lower rates depending on your credit score. Lower rates can help you save on interest payments.

Next, consider the rewards and benefits. Many credit cards offer cashback, travel rewards, or points for spending. These perks can be valuable for your startup’s everyday expenses.

- Cashback on office supplies

- Travel rewards for business trips

- Points for everyday purchases

Lastly, be aware of any fees associated with the card. These can include annual fees, late payment fees, and balance transfer fees. Avoid cards with high fees as they can add significant costs.

Venture Capital vs. Credit Card: Making Informed Choices

Choosing between venture capital and credit cards for startup funding depends on your business needs. Each option has unique benefits and drawbacks. Weighing them carefully will guide your decision.

Venture capital involves getting investments from professional investors. These investors provide large amounts of funding but expect equity in return. This means they get a share of your startup.

| Venture Capital | Credit Cards |

|---|---|

| Large funding amounts | Quick access to funds |

| Equity required | No equity needed |

| Long-term partnership | Short-term, manageable debt |

Credit cards, on the other hand, provide immediate access to capital. No equity is involved, so you retain full ownership of your business. However, credit limits can restrict how much you can spend.

Consider the flexibility of credit cards. They allow you to cover daily expenses and take advantage of rewards programs. But, high-interest rates can create significant debt if not managed well.

Venture capital offers more than just money. Investors often bring valuable expertise and connections. This can help your startup grow more quickly than relying solely on credit cards.

Ultimately, your choice will depend on your business goals and financial situation. Assess both options thoroughly to determine which aligns best with your needs. Making an informed choice will set your startup on the path to success.

Responsible Card Usage for Business Expenses

Responsible credit card usage can ensure your startup remains financially healthy. It’s essential to keep track of all your expenses. This practice helps avoid unnecessary debt.

Always pay your credit card bill on time. Late payments can lead to high-interest charges and affect your credit score. Set reminders or automate payments to stay on track.

- Automate payments

- Set calendar reminders

- Avoid late fees

Limit the use of credit cards for essential business expenses only. This helps manage cash flow and prevents overspending. Focus on expenses that can generate revenue.

Take advantage of rewards programs offered by your credit card. Many cards offer cashback, travel points, or discounts. These rewards can offset some business costs.

It’s crucial to review your credit card statements regularly. This will help identify any unauthorized charges or errors. Address any discrepancies promptly to avoid issues.

Keep your credit utilization low. This improves your credit score and creates room for future expenses. Aim to use no more than 30% of your available credit.

How to Minimize Risks with Credit Cards

Minimizing risks with credit cards is crucial for financial health. Start by setting a budget for your expenses. This ensures you only spend what you can afford to repay.

Monitor your credit card activity regularly. Check for any unauthorized transactions immediately. This helps you catch and address issues quickly.

- Set spending alerts

- Review statements monthly

- Report any discrepancies

Keep your credit utilization ratio low, ideally below 30%. High utilization can negatively affect your credit score. This impacts your ability to get loans in the future.

Consider using credit cards with lower interest rates. Some cards offer promotional 0% APR periods, which can be beneficial. Switching to a lower APR card reduces the amount of interest you pay.

Avoid cash advances whenever possible. They come with high fees and interest rates. Instead, use your credit card for purchases and pay off the balance promptly.

Finally, have a clear repayment strategy. Paying more than the minimum balance helps reduce your debt faster. This minimizes interest charges and improves financial stability.

Strategies for Managing Credit Card Debt

Managing credit card debt effectively is vital to maintain financial health. Start by creating a repayment plan. This should include paying more than the minimum balance each month.

Consider consolidating your debts. By combining multiple balances into one low-interest loan, you can simplify repayments. Many financial institutions offer debt consolidation services.

- Simplifies repayment

- Often comes with lower interest rates

- Reduces stress by having a single payment

Use a balance transfer card if possible. These cards offer 0% APR for an introductory period, allowing you to pay off existing debt without accruing additional interest. Just be mindful of any transfer fees involved.

Create and stick to a budget to control spending. Track all income and expenses diligently. A detailed budget helps avoid unnecessary purchases and keeps your finances on track.

Avoid using your credit card while you focus on paying down your debt. Using cash or debit for daily expenses can prevent further accumulation of debt. It’s essential to live within your means during this period.

Seek professional advice if needed. Credit counseling services can provide customized plans and negotiations with creditors. Professional help ensures you get back on the right financial path efficiently.

Monitoring and Improving Your Credit Health

Keeping an eye on your credit health is crucial when using credit cards for startup funding. Regularly checking your credit report helps you spot errors and discrepancies. Correcting these promptly can improve your credit score.

Use tools and apps to monitor your credit score. Many services offer free credit score checks and updates. This keeps you informed about any changes affecting your score.

- Free credit monitoring tools

- Regular updates and alerts

- Access to detailed credit reports

Paying off debts on time is essential for a good credit score. Late payments can significantly harm your credit health. Set up automated payments to ensure you never miss a due date.

Limit new credit applications. Each application results in a hard inquiry on your report, which can lower your score. Apply for new credit cards only when necessary.

Consider diversifying your credit mix. Having a variety of credit types, like loans and credit cards, can positively impact your score. This shows that you can manage different forms of credit responsibly.

Lastly, keep your credit utilization ratio low. Aim to use less than 30% of your available credit limit. Lower utilization demonstrates good credit management and boosts your credit score.

Frequently Asked Questions

Using credit cards to fund a startup is a common approach but comes with its own set of complexities. Here, we address some frequently asked questions to help you make informed decisions.

1. What are the main advantages of using credit cards for startup funding?

The primary advantage is the immediate access to capital. Credit cards allow you to make essential purchases swiftly, eliminating delays that can hinder business operations. Additionally, many credit cards offer rewards and cashback programs that can offset some of your expenses.

Another benefit is flexibility in managing short-term cash flow issues. Unlike traditional loans, which may have stringent approval processes and terms, credit cards offer more immediate solutions for smaller funding needs without needing collateral or extensive paperwork.

2. Are there specific types of credit cards suited for startups?

Yes, business credit cards are often tailored for startups with features that separate them from personal credit cards. These include higher spending limits, enhanced tracking tools for expenses, and better rewards relevant to business spending categories like office supplies and travel.

Some business credit cards also offer 0% APR introductory periods on purchases and balance transfers. This can provide an interest-free period useful for making large initial investments or consolidating existing debts into one manageable payment plan.

3. How can I improve my chances of getting approved for a business credit card?

A strong personal credit score is crucial as most issuers consider it during the application process. Regularly checking and improving your score by paying off existing debts timely and keeping your credit utilization low will help.

You also need a well-documented plan showing your startup’s potential revenue streams and operational plans. Lenders favor businesses with clear strategies since they indicate lower risk and higher likelihood of timely payments.

4. What risks should be considered when using a personal credit card instead of a business one?

Using a personal card mixes business expenses with private ones, complicating financial management and tax filing. Poor separation could lead to inaccurate record-keeping, increasing audit risks.

This approach affects your personal liability because defaults will impact your private finances directly; jeopardizing both household budget stability and your individual credit score.

5: What strategies can I use to manage high-interest rates on my credit card debt successfully?

Minimizing high-interest rate burdens involves promptly paying down balances each month beyond minimums due whenever feasible-to reduce carryover amount subject securing favorable refinanced terms at lower lender-borrowing costs may provide relief.

Consider transferring higher-rate balances temporarily onto zero/ low-rate promotional accounts strictly adhered repayment schedules manageably ease pressure while addressing outstanding owed funds effectively proactively caution maintain disciplined approached throughout duration period necessary stabilized reduced levels attained avoiding exacerbation scenarios..

Final ThoughtsUsing credit cards to fund your startup can provide immediate financial flexibility. However, it’s crucial to approach this method with a solid plan. Weigh the benefits against the risks to make informed decisions that suit your specific needs.

Proper management of credit card debts and regular monitoring of your credit health will ensure sustainable growth. By applying the strategies discussed, your startup can gain the financial footing it needs without falling into the pitfalls of overwhelming debt. Your diligence today sets the stage for a thriving business tomorrow.