Starting early in life, where individuals usually have fewer financial commitments, investment strategies can hinge on higher risk and higher growth potential. Have you ever considered that millennials are projected to inherit over $68 trillion from baby boomers and Gen-X? This immense wealth transfer underscores the importance of tailored investment strategies at various life stages.

In the early career phase, aggressive portfolio allocations dominate, with an emphasis on equities. However, as one transitions into mid-career, risk management begins to take precedence. Interestingly, retirees may allocate up to 80% in fixed-income securities to preserve capital while ensuring steady returns. These shifts showcase the dynamic nature of investment strategies across different life stages.

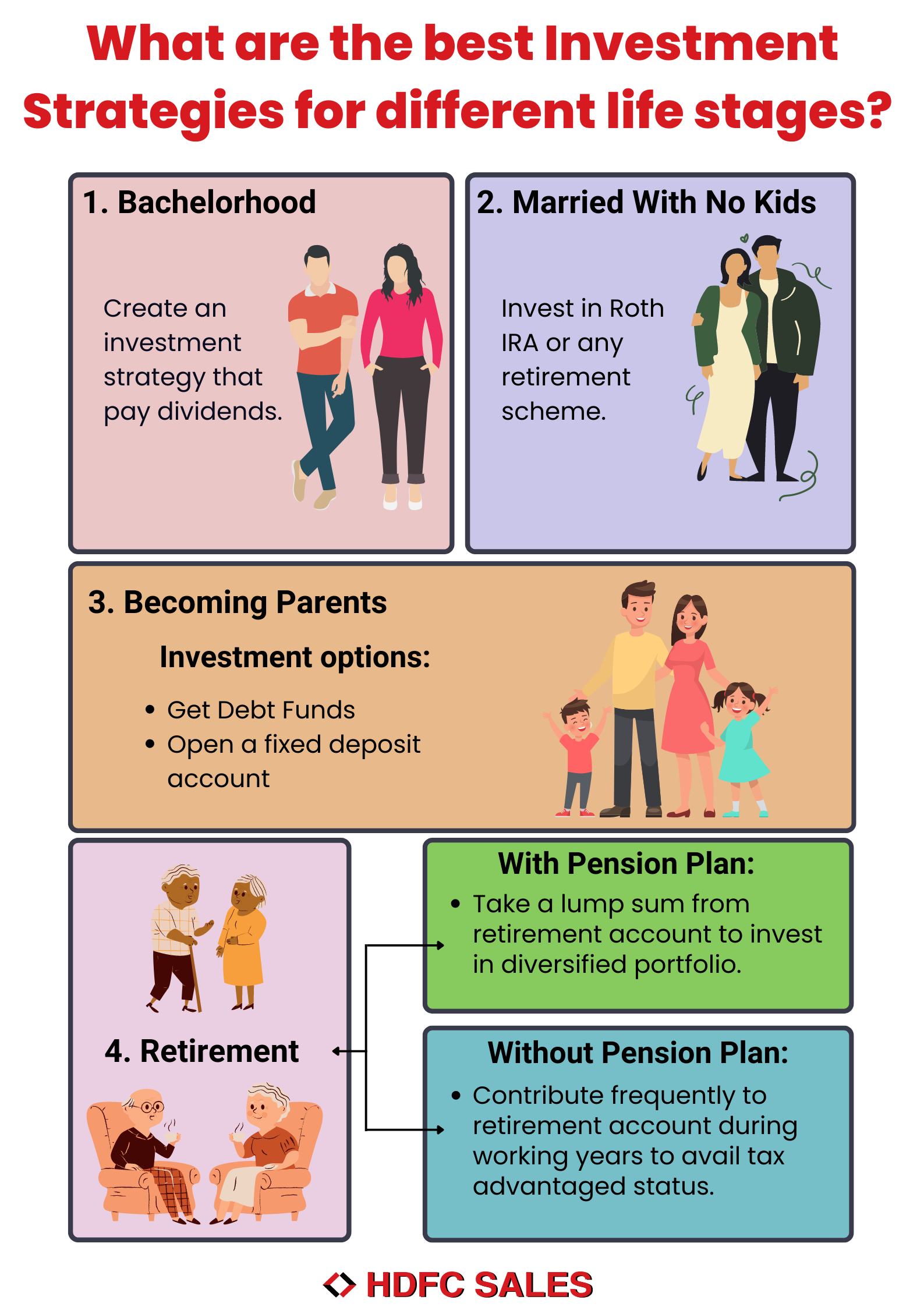

Different Investment Strategies at Various Life Stages

Investment strategies can vary greatly depending on your life stage. In your twenties, focusing on high-growth potential investments like stocks can make sense. That’s because you have time to recover from market downturns.

As you move into your thirties and forties, diversifying your portfolio becomes crucial. It might be wise to introduce bonds and real estate. This approach balances risk while still offering growth opportunities.

In your fifties, preparing for retirement takes precedence. Shifting towards more secure, income-generating assets like fixed-income bonds is common. All the while, it is important to safeguard the wealth you’ve accumulated.

Finally, for those in retirement, preserving capital is the priority. Investments should focus on low-risk securities. These include savings accounts and government bonds, providing steady returns without high risks.

Investment Approach in Early Life Stage

During the early years, risk is often more tolerable. This allows for aggressive investment choices. These choices primarily include stocks and mutual funds.

Young investors benefit from the power of compounding. Over time, small investments can grow significantly. Starting early leverages this growth potential.

Moreover, young investors can afford to make and learn from mistakes. Corrections made now pave the way for better financial decisions later. This stage lays a strong foundation for future wealth.

Investment Priorities for Mid-Career Individuals

Mid-career individuals need a balanced approach. Their focus shifts from high risk to stability and growth. Diversifying into bonds and real estate becomes essential.

Many also invest in their children’s education and their own retirement funds. It’s a time to review and adjust. This ensures their portfolio aligns with their changing goals and responsibilities.

Additionally, mid-career might involve more disposable income. This can be redirected into secure investments. Regular reviews help in staying on track with their financial goals.

Investment Strategies for Pre-retirement Period

As retirement approaches, risk tolerance typically decreases. The emphasis shifts to safeguarding existing assets. Investments in fixed-income bonds and secure assets are common.

Pre-retirees often consolidate their investments. This includes rolling over 401(k) accounts. The goal is to ensure easy management and secure growth.

It’s also the time to consider healthcare costs and other post-retirement expenses. Ensuring a reliable income stream becomes crucial. This often involves consultations with financial advisors.

Investment Approach in Early Life Stage

Starting your investment journey early offers a big advantage. It allows you to take on more risk in hopes of greater returns. You have time to recover from any market downturns.

In your twenties, focusing on growth potential is crucial. Stocks and mutual funds usually make up a large part of your portfolio. These options can yield high returns over time.

However, don’t ignore the power of compound interest. Investing small amounts regularly can significantly increase your wealth. Over time, this can turn into a large sum.

Although risky investments dominate, it’s wise to diversify. Consider adding some bonds or real estate to balance risk. Diversification helps protect against market swings.

Importance of Starting Early

Investing early helps build a strong financial foundation. The earlier you start, the more time your money has to grow. This is due to the compounding effect.

Young investors often have fewer financial obligations. This allows for a more aggressive investment strategy. More risk can mean higher returns.

Remember, learning from early mistakes is a growth opportunity. These lessons will improve your financial skills. Experience is a valuable teacher.

Diversification in Early Investments

Diversification is key, even early on. Don’t put all your money into one type of investment. Spread it across different assets to mitigate risk.

This might include a mix of stocks, bonds, and real estate. Each asset type behaves differently. Thus, your overall risk is reduced.

Diversifying also provides multiple income sources. If one investment underperforms, others can compensate. This balance is crucial for long-term stability.

Understanding Compound Interest

Compound interest can significantly grow your investments. When you earn interest on both your initial amount and the interest it earns, the growth multiplies. The longer your investment duration, the greater the benefits.

Start small but be consistent. Regular contributions make a big difference over time. Even minor amounts add up due to compounding.

Utilize tools and calculators to understand potential growth. This can motivate you to invest regularly. Seeing future potential often boosts commitment.

Investment Priorities for Mid-Career Individuals

By mid-career, financial responsibilities have grown, and goals have become clearer. This life stage often includes higher income and more savings potential. It’s also a good time to balance risk and return.

Diversification plays a crucial role. A balanced portfolio might include stocks, bonds, and real estate. This approach spreads risk and enhances stability.

Retirement planning becomes more significant. Increasing contributions to retirement accounts like 401(k)s and IRAs is essential. Early preparation ensures a comfortable post-retirement life.

Financial security is also linked to emergency funds. Setting aside money for unexpected events can prevent financial setbacks. This fund offers peace of mind and stability.

Adjusting Investment Strategies with Marital Status

Getting married often means merging finances. Couples should revisit their investment strategies. Joint financial planning helps align long-term goals.

Dual incomes can lead to higher savings. This allows for diversifying investments further. Both partners should discuss risk tolerance openly.

Creating a shared budget is also vital. This helps track expenses and savings. Agreeing on a budget fosters financial harmony.

When kids enter the picture, priorities shift. Investments may focus more on future education costs. 529 plans are popular for saving tuition money.

Divorce impacts finances significantly. Assets and debts are divided. It’s crucial to reassess one’s investment portfolio during this transition.

Communication remains key throughout these changes. Regular financial meetings benefit both parties. Staying informed helps manage investments better.

The Impact of Matrimony on Investment Decisions

Marriage significantly affects financial planning. Combining two incomes creates new opportunities for investment. Couples often have greater financial resources to allocate.

However, dual incomes also come with shared responsibilities. Mortgages, children’s education, and healthcare need to be accounted for. These expenses require careful planning.

Investment decisions should align with joint goals. Open communication about risk tolerance helps in selecting suitable investments. Both partners should contribute to the decision-making process.

Creating an emergency fund becomes even more important. This fund safeguards against unexpected events like job loss or health issues. It provides a financial safety net.

Regular financial meetings can be helpful. These discussions allow for adjustments based on life changes. Review your investment portfolio periodically.

Married couples often need to balance long-term and short-term goals. Investments for retirement should be planned alongside immediate needs. This balance ensures financial stability.

Effect of Parenthood on Investment Strategies

Parenthood introduces new financial responsibilities. Suddenly, costs related to raising a child become significant. These include education, healthcare, and daily expenses.

One key strategy is starting a college fund early. Using plans like a 529 can provide tax advantages. Regular contributions ensure the fund grows over time.

Revising your budget is also crucial. Allocating funds for childcare, school supplies, and extra-curricular activities is essential. This might require cutting back on non-essential expenses.

Insurance needs often change with parenthood. Health and life insurance become even more important. These policies protect the family’s financial well-being.

Long-term financial planning should include an updated will. Planning for your children’s future in case of unexpected events is critical. This helps ensure their financial security.

Lastly, consider balancing aggressive and conservative investments. While saving for your child’s future, it’s important to diversify your portfolio. This helps manage risks effectively.

Investment Strategies for Pre-retirement Period

The pre-retirement period is crucial for securing your financial future. This phase focuses on reducing risk and safeguarding assets. It involves adjusting your portfolio to ensure steady income post-retirement.

Shifting investments towards lower-risk options is a key move. Consider increasing holdings in bonds and fixed-income securities. These provide more stability compared to stocks.

It’s also wise to boost contributions to retirement accounts. Maximizing your 401(k) and IRA contributions can significantly enhance your nest egg. These accounts offer tax advantages that benefit long-term savings.

Healthcare should not be overlooked either. Setting aside funds for potential medical expenses becomes important as you age. Health Savings Accounts (HSAs) can be beneficial here.

Another strategy involves downsizing or paying off debt. Reducing mortgage balances or eliminating credit card debts provides more financial freedom. This makes managing retirement income easier.

Lastly, consider consulting a financial advisor. They can help optimize your investment strategy before retirement. Personalized advice ensures you’re on the right track.

Risk Management and Asset Reallocation in Pre-retirement

As you approach retirement, managing risk becomes a priority. The goal is to protect your accumulated wealth. This often means reallocating assets to more stable investments.

Shifting a portion of your portfolio to bonds is a common strategy. Bonds typically offer lower risk compared to stocks. They provide a fixed income, ensuring steady returns.

Another approach is diversifying into annuities. Annuities can offer guaranteed income for life. This adds a level of financial security.

Reviewing and adjusting your portfolio regularly is essential. Market conditions change, and your investments should reflect that. Regular reviews help maintain a balanced risk.

Don’t forget about liquidity needs. Keeping a portion of your assets in cash or cash equivalents is wise. This ensures you have funds available for any sudden expenses.

Consider working with a financial advisor. They can offer personalized advice on asset reallocation. Having expert guidance can make a big difference.

Strategic Investment for Retirees

For retirees, the primary goal is often preserving capital. Low-risk investments become more appealing. These include government bonds and savings accounts.

Generating a steady income stream is crucial. Dividend-paying stocks and annuities can provide this. They offer regular payouts that help cover living expenses.

Maintaining liquidity is also essential. Keeping a portion of assets in cash or liquid funds ensures availability for emergencies. This can prevent the need to sell investments at a loss.

Healthcare costs can rise during retirement. Investing in Health Savings Accounts (HSAs) can be beneficial. These accounts offer tax advantages and can be used for medical expenses.

Downsizing might also be a consideration. Selling a larger family home and moving to a smaller one can free up capital. This capital can then be reinvested for additional income.

Consulting with a financial advisor is recommended. They can provide a tailored investment strategy. Expert advice ensures that retirees make informed financial decisions.

Frequently Asked Questions

Discover key insights about investment strategies across different life stages. These questions address common concerns and offer practical advice for investors.

1. How can young investors benefit from high-risk investments?

Young investors often have a longer time horizon, allowing them to take on more risk. High-risk investments, such as stocks, can potentially yield higher returns over the long term.

This strategy leverages the power of compounding interest, which can significantly grow their initial investment. Learning from mistakes at this age also helps build better financial habits for the future.

2. What should mid-career individuals consider when diversifying their portfolio?

Mid-career individuals should balance growth and stability by including a mix of assets like stocks, bonds, and real estate in their portfolio. Diversification helps manage risk while still providing opportunities for growth.

This stage often involves planning for children’s education and retirement savings, so it’s essential to regularly review and adjust investments. Being flexible ensures that financial goals are met as responsibilities evolve.

3. Why is it important to adjust investment strategies before retirement?

If retirement approaches, reducing risk becomes crucial to preserving accumulated wealth. Shifting assets to lower-risk options like bonds or fixed-income securities helps ensure stable returns.

Maximizing contributions to retirement accounts during this period is advisable for enhancing long-term savings. This prepares you financially for a comfortable post-retirement life by securing additional income streams.

4. How does parenthood change investment priorities?

When you have children, new financial responsibilities emerge, making it essential to plan ahead for educational expenses through college funds like 529 plans or educational savings accounts.

In addition, adjusting budgets to account for your child-related needs may be necessary along with revisiting insurance coverage requirements due to increased family reliance.

5 .

What are some strategic tips retirees can use even if they’re just starting?

<

p >

A s retiree begins its journey focusing on capital preservation became focal;

Having regular payout streams lets an easy handling of essentials assured with some well-placed low – exposure elements like Health Savings Account HSA catering mainly medical necessities lessening stress unforeseen payouts alongside consulting externally brings ease aligning easily secured path boosting confidence in times future.

Investment Strategies for different Life Stages!

Conclusion

Investment strategies must adapt to life changes to maximize their effectiveness. From taking high risks early on to securing stable returns in retirement, each stage demands specific approaches. Flexibility and regular reviews are crucial to staying on track.

Whether planning for a child’s education or managing retirement funds, tailored strategies ensure financial stability. By understanding and implementing these tailored strategies, individuals can confidently navigate their financial journeys and achieve their long-term goals.