Consider this: the global economy grew by a staggering 4.7% in 2021, rebounding sharply after the pandemic-induced recession. Macroeconomics plays a pivotal role in understanding such dynamic shifts. It’s through this lens that policymakers craft strategies aiming for sustainable growth and stability.

Historical economic strategies have evolved considerably since the Great Depression shaped modern macroeconomic principles. For instance, Keynesian economics highlights government intervention, while monetarism focuses on controlling money supply. Modern strategies often blend these theories, integrating data-driven policies to foster resilient economic growth globally.

The Essence of Macroeconomics

Macroeconomics is the study of the economy on a large scale. It looks at national and global economic factors. This includes everything from inflation to unemployment.

Understanding macroeconomics helps governments make better economic decisions. They can create policies that aim to stabilize the economy. This benefits everyone by reducing economic risks.

There are several key principles in macroeconomics. One is the idea of supply and demand. Another important concept is economic growth, which is the increase in the amount of goods and services produced by an economy over time.

Finally, macroeconomics also involves studying government spending and taxation. These actions can influence economic activity. By adjusting these, governments can either stimulate or cool down the economy.

Principles of Macroeconomics

Macroeconomics relies on key principles to understand how economies function. Supply and demand is one of the most basic concepts. It explains how prices and quantities of goods are determined.

Another vital principle is the business cycle. This refers to the fluctuations in economic activity over time. Economies go through periods of expansion and contraction.

Monetary policy is another crucial area. Central banks use tools like interest rates to control money flow. This can impact inflation and employment levels.

Importance of Macroeconomics in National Economy

The importance of macroeconomics can’t be overstated. It helps policymakers understand broad economic trends. This includes everything from inflation rates to GDP growth.

Macroeconomics also aids in predicting economic outcomes. This is useful for long-term planning. For example, knowing potential inflation helps in setting interest rates.

Finally, macroeconomics guides fiscal policy. This involves government spending and taxation. Proper fiscal policy can stabilize the economy during downturns.

The Role of Academic Research in Macroeconomics

Academic research plays a significant role in advancing macroeconomics. Scholars study historical data to understand economic trends. Their findings help inform better policies.

Research also focuses on developing new economic models. These models simulate various economic scenarios. Policymakers use these models to make informed decisions.

Lastly, academic research often identifies emerging economic issues. Early identification allows for proactive measures. This ensures the economy remains resilient and adaptable to changes.

Principles of Macroeconomics

Macroeconomics revolves around several core principles that explain how economies operate on a broad scale. These principles include topics like inflation, unemployment, and GDP. Understanding these principles helps policymakers make informed decisions to boost economic stability and growth.

Supply and Demand

The concept of supply and demand is fundamental to macroeconomics. It explains how the prices of goods and services are determined. When demand increases but supply remains constant, prices usually go up.

Conversely, if supply increases and demand stays the same, prices tend to fall. This balance affects everything from food prices to housing costs. Policymakers monitor these trends to manage inflation.

Supply and demand directly affect consumer behavior. If prices rise too high, consumers may reduce spending. Understanding this interaction helps economists predict market shifts.

The Business Cycle

Another key principle is the business cycle. This refers to the natural ups and downs in economic activity. Periods of rapid growth are often followed by slowdowns or recessions.

During a boom phase, employment rates are high, and businesses prosper. Conversely, a recession features high unemployment and lower economic output. Governments use tools like fiscal policy to try and smooth out these cycles.

The business cycle impacts everyone from workers to investors. Understanding where the economy is in the cycle can guide both personal and business decisions. This knowledge is essential for long-term planning.

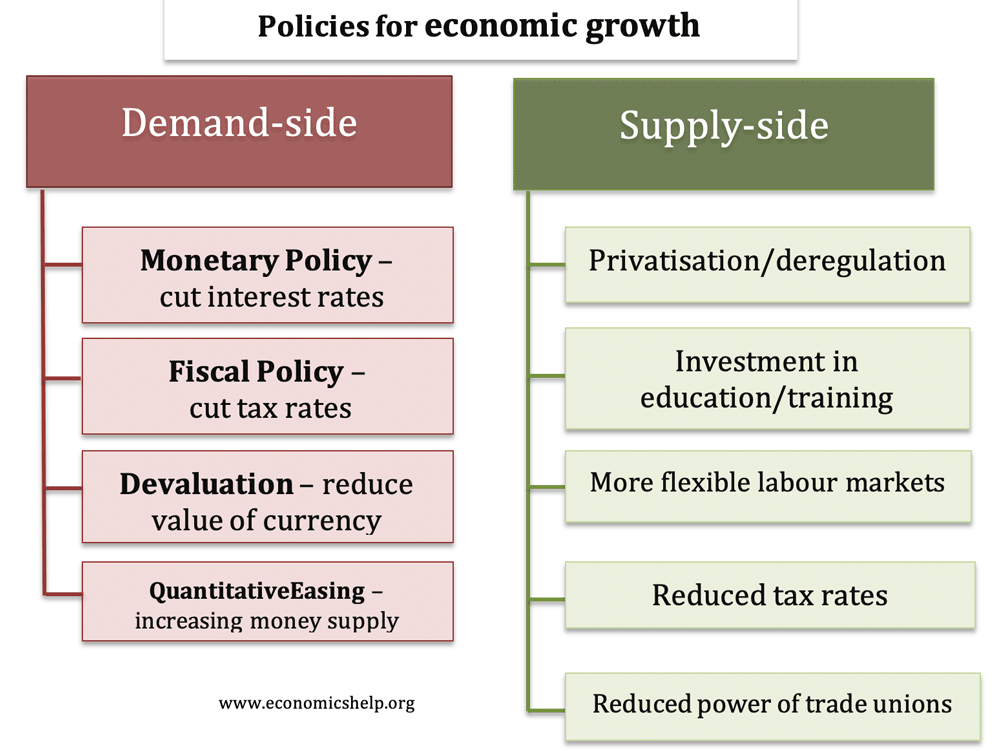

Fiscal and Monetary Policy

Fiscal and monetary policies are crucial for economic stability. Fiscal policy involves government spending and taxation. By adjusting these, governments can influence economic activity.

Monetary policy, on the other hand, is controlled by central banks. They use tools like interest rates and money supply to manage inflation and employment. Both policies aim to achieve stable economic growth.

These policies are implemented based on economic conditions. For example, during a recession, a government might increase spending to stimulate growth. Conversely, if inflation is high, central banks might raise interest rates.

Importance of Macroeconomics in National Economy

Macroeconomics is crucial for understanding how a nation’s economy works. It helps policymakers analyze broad trends like inflation and unemployment. This analysis guides effective economic decisions.

Economic growth is a key aspect examined in macroeconomics. By studying GDP and other indicators, countries can gauge their economic health. This understanding helps in creating policies to boost growth.

Macroeconomics also plays a role in stabilizing the economy during crises. For instance, during a recession, governments use macroeconomic principles to implement stimulus packages. These actions help mitigate negative impacts.

Finally, macroeconomics informs fiscal and monetary policies. Proper management of taxes, government spending, and interest rates promote sustainable development. These policies are essential for maintaining economic stability.

Economic Growth as a Central Aspect of Macroeconomics

Economic growth is a vital part of macroeconomics. It measures how much a country’s economy is expanding. Growth is usually tracked through the Gross Domestic Product (GDP).

Strong economic growth benefits everyone. It creates jobs and increases incomes. This leads to a higher standard of living.

Governments aim for steady and sustainable growth. They use various policies to stimulate the economy. This can include lowering interest rates and increasing public spending.

Increased productivity is another factor that drives growth. When workers can produce more goods and services efficiently, the economy grows. Innovation and technology play a big role in boosting productivity.

Economic growth can be uneven across different sectors. Some industries might grow faster than others. This makes it important for policymakers to support diverse areas of the economy.

Finally, global trade impacts economic growth. Countries that trade more with others tend to grow faster. Open markets and careful trade policies can help sustain economic growth.

The Correlation Between Macroeconomics and Economic Growth

Macroeconomics and economic growth are closely linked. Macroeconomic policies shape the environment in which economies grow. Good policies can lead to sustainable growth, while poor ones can hold an economy back.

Inflation control is a key aspect of this correlation. Stable prices create a favorable environment for businesses. This stability encourages investment and production.

Employment levels also play a role. High employment means more people have money to spend. Increased spending boosts demand for goods and services.

Government interventions, such as stimulus packages, can jumpstart economic growth. These interventions are often based on macroeconomic analysis. They aim to address economic downturns and spur growth.

Fiscal policies like taxation also impact growth. Lower taxes can increase disposable income, leading to higher consumer spending. This can further drive economic expansion.

Lastly, investment in infrastructure and education is critical. Better roads and schools improve productivity. These investments are often guided by macroeconomic insights.

Components of Economic Growth in Macroeconomics

Economic growth relies on several key components. These elements work together to boost a nation’s economic output. Understanding these components helps policymakers create effective growth strategies.

One major component is capital. Investment in machinery, buildings, and infrastructure increases production capacity. More capital means businesses can produce more goods and services.

Labor is another critical factor. A skilled and educated workforce is essential for economic growth. Training and education programs can enhance the quality of labor.

Technological innovation drives economic growth significantly. Advancements in technology increase efficiency and create new products. This can lead to higher productivity and economic expansion.

Natural resources also play a role. Countries with abundant resources like oil, minerals, and fertile land can grow faster. However, sustainable management of these resources is crucial.

Entrepreneurial activity fosters economic growth as well. Entrepreneurs create new businesses and jobs. They bring fresh ideas and innovations to the market, stimulating economic development.

Lastly, political and economic stability is essential. Stable environments attract investment, both domestic and foreign. This stability builds confidence, which is vital for sustained growth.

Formulating Economic Growth Strategies

Formulating economic growth strategies requires a multifaceted approach. Policymakers must consider various factors to create effective plans. Understanding these factors is key to promoting sustainable growth.

One essential element is infrastructure development. Investment in roads, bridges, and public transportation boosts economic activities. It makes it easier for businesses to operate efficiently.

Education and skills training are also vital components. A well-educated workforce can adapt to new technologies and market demands. This enhances productivity and drives economic expansion.

The role of technology cannot be ignored. Encouraging innovation leads to more efficient production methods. Governments can support this by funding research and development.

- Diversifying the economy is another strategy.

- This reduces reliance on a single industry.

- Diverse economies are usually more resilient during downturns.

Sustainable resource management is crucial as well. Ensuring that natural resources are used wisely guarantees long-term benefits. Policies must balance exploitation with conservation efforts.

Finally, fostering international trade opens up new markets for goods and services. Trade agreements can lower barriers, making it easier for countries to export their products. Greater access to global markets accelerates economic growth.

Key Considerations in Strategy Formulation

When creating strategies for economic growth, various factors must be considered. These factors help ensure that the strategies are effective and sustainable. Understanding these key elements is crucial for successful planning.

One important consideration is the current economic environment. Analyzing factors like inflation, unemployment, and GDP growth provides a clear picture. This analysis helps tailor strategies to specific economic conditions.

Public opinion and political stability also play a significant role. Strategies are more likely to succeed if they have public support. Political stability fosters a favorable environment for economic initiatives.

- Resource availability is another key factor.

- Strategies should leverage the country’s strengths.

- This includes natural resources, labor, and technology.

Global economic trends can impact national strategies. Keeping an eye on these trends helps align domestic policies with international markets. This ensures that strategies remain relevant and competitive.

Finally, it’s essential to set measurable goals. Objectives should be clear and achievable. This helps track progress and make necessary adjustments.

Impact of Economic Policies on Effective Strategies

Economic policies play a crucial role in formulating effective growth strategies. These policies guide how resources are allocated and utilized. Proper policies can boost economic performance and stability.

Fiscal policy is one key area. Government spending and taxation influence economic activity. Increased public spending can stimulate growth, while higher taxes might slow it down.

- Monetary policy is equally significant.

- Central banks adjust interest rates and control money supply.

- This affects inflation, borrowing, and investments.

Effective economic policies also promote innovation. Funding for research and development leads to new technologies. This drives productivity and economic expansion.

Trade policies impact international economic relationships. Lower tariffs can increase exports and imports. This opens up new markets and opportunities for growth.

Social policies can’t be overlooked. Investment in healthcare and education builds a skilled workforce. This supports long-term economic development.

Finally, environmental policies contribute to sustainable growth. Regulations on pollution and resource use ensure that growth doesn’t come at the expense of future generations. Sustainable practices are essential for long-term prosperity.

Application of Macroeconomic Concepts in Strategy Execution

Applying macroeconomic concepts is vital for successful strategy execution. These concepts provide a framework for understanding economic dynamics. Effective use of these ideas can lead to robust economic policies.

One key concept is fiscal policy. Governments utilize spending and taxation to influence economic activity. For example, increased public spending can stimulate economic growth during downturns.

- Monetary policy is another important tool.

- Central banks adjust interest rates to manage inflation.

- Lower rates can boost borrowing and investment.

Macroeconomic models help in forecasting economic outcomes. These models consider various factors like GDP, employment, and inflation. Forecasting helps in planning and making informed decisions.

Trade policies also come into play. Policies that encourage exports can lead to economic growth. Reducing trade barriers opens up international markets for domestic producers.

Economic indicators like unemployment rates are crucial for strategy execution. High unemployment signals economic distress, prompting targeted interventions. Employment programs and training can help alleviate this issue.

Lastly, long-term sustainability is a key consideration. Environmental policies ensure that economic growth does not deplete resources. Sustainable practices guarantee that growth benefits future generations.

The Role of Policymakers in Implementing Economic Growth Strategies

Policymakers play a crucial role in implementing economic growth strategies. Their decisions affect the overall health of the economy. Effective policies can lead to sustainable growth and improved living standards.

One of their key responsibilities is to set fiscal policies. This involves decisions about government spending and taxation. Well-planned fiscal policies can stimulate economic activity.

- Policymakers also shape monetary policy.

- They work with central banks to control money supply and interest rates.

- This helps manage inflation and economic stability.

Regulating trade is another important duty. Trade policies can open new markets and boost exports. Reducing trade barriers fosters international economic relationships.

Building infrastructure is essential for growth. Policymakers allocate funds for roads, schools, and hospitals. These investments provide the backbone for economic activities.

Lastly, they must ensure environmental sustainability. Policies that balance growth with resource conservation are vital. This approach ensures long-term benefits for future generations.

Evaluating the Success of Growth Strategies

Evaluating the success of growth strategies is essential for continuous improvement. It helps identify what works and what doesn’t. Effective evaluation can lead to better future planning.

One key method is to measure GDP growth. An increase in GDP indicates a growing economy. Stable or increased GDP often signals successful strategies.

- Employment rates are another vital indicator.

- Higher employment means more people have jobs.

- This usually points to effective growth policies.

Inflation rates also matter. Low and stable inflation suggests a healthy economy. High inflation can undermine growth, showing the need for policy adjustments.

Public opinion provides valuable insights. Surveys and polls can gauge how people feel about economic conditions. Positive feedback often reflects successful strategies.

Finally, international trade balances are important. A favorable trade balance means a country exports more than it imports. This is a sign of strong economic health and effective policies.

Frequently Asked Questions

This section addresses common questions related to macroeconomics and economic growth strategies. Dive in to understand how these critical concepts shape our economies.

1. How does inflation impact economic growth?

Inflation, when moderate, can signify a growing economy by increasing prices and wages. However, high inflation erodes purchasing power and savings, leading to decreased consumer spending and investment.

On the other hand, deflation (falling prices) can slow economic growth as consumers delay purchases. Policymakers aim for stable inflation rates to balance these effects.

2. What role does fiscal policy play in economic growth?

Fiscal policy involves government spending and taxation decisions that influence economic activity. Increased public spending on infrastructure or education can stimulate growth by creating jobs and enhancing productivity.

Conversely, higher taxes might reduce disposable income and lower consumer spending. Well-crafted fiscal policies aim to boost long-term economic growth while maintaining budgetary balance.

3. How do technological advancements contribute to economic growth?

Technological advancements drive efficiency and innovation, boosting productivity across various sectors. For instance, automation increases manufacturing output while reducing costs.

This leads to higher-quality goods at lower prices, benefiting consumers and businesses alike. By fostering an environment that supports tech development, governments can ensure sustained economic advancement.

4. Why is investment in education crucial for economic growth?

A well-educated workforce is essential for innovation and productivity improvements. Higher education levels equip individuals with skills needed for technologically advanced industries.

This enhances a country’s competitive edge globally and attracts foreign investments. Investment in education increases employability and drives long-term sustainable economic development.

5. How do international trade policies affect national economies?

Liberal trade policies open up markets for exports, boosting domestic production and employment. Lower tariffs make imported goods cheaper, increasing consumer choice and lowering costs of raw materials for businesses.

However, protectionist measures like high tariffs can lead to trade wars affecting global supply chains negatively. Balanced trade policies encourage fair competition while protecting domestic interests.

Conclusion

Understanding macroeconomics and implementing effective economic growth strategies are crucial for national prosperity. By analyzing key factors such as inflation, fiscal policies, and technological advancements, policymakers can create environments that foster sustainable growth.

Investment in infrastructure, education, and innovation drives economic development. Balanced trade policies further enhance growth by opening markets and encouraging competition. Together, these elements ensure a stable and thriving economy.