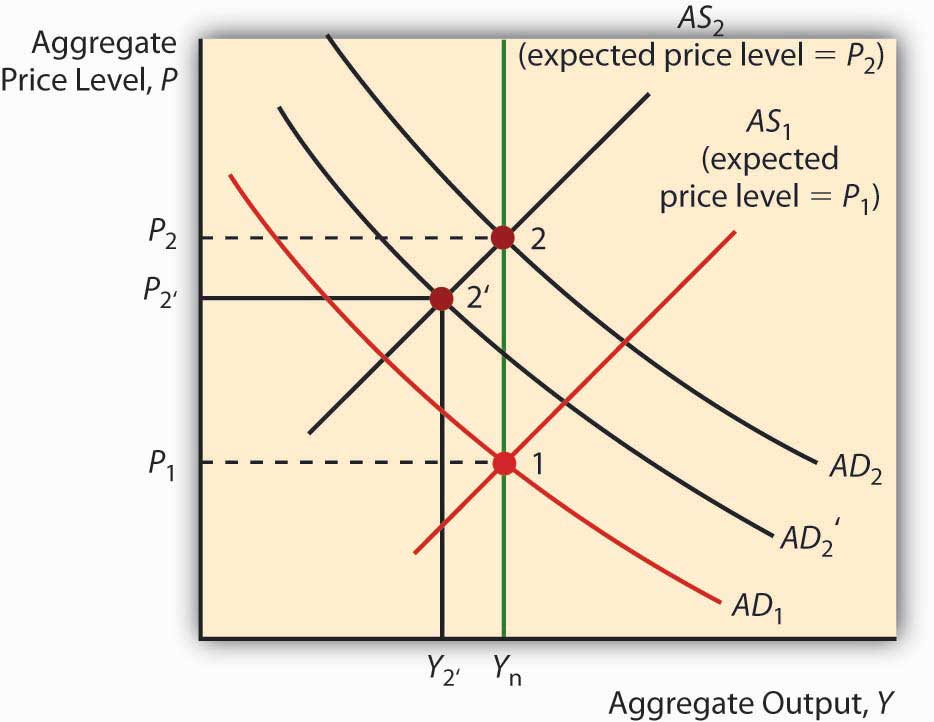

One striking aspect of macroeconomics is how we can often predict economic outcomes merely by understanding human behavior and rational expectations. Consider the 1970s stagflation: traditional economic models failed to explain the phenomenon, but the rational expectations theory offered a fresh lens, suggesting that individuals’ anticipation of inflation affected their actions and contributed to persistent inflation. This theory revolutionized economic policy by emphasizing the forward-looking nature of decision-making.

The rational expectations hypothesis, formulated by John Muth in the 1960s, posits that individuals use all available information to predict future economic variables accurately, influencing their current economic actions. This concept reshaped fiscal and monetary policies, compelling governments and central banks to be transparent and credible in their strategies. For instance, the Volcker disinflation of the early 1980s depended heavily on managing expectations to tame runaway inflation, showcasing the profound impact of rational expectations on macroeconomic stability.

The Core Ideas of Macroeconomics

Macroeconomics focuses on the big picture of an economy. It looks at whole economies, instead of individual markets or people. This branch of economics examines issues like **unemployment**, **inflation**, and **economic growth**.

Economic growth measures how much an economy’s output is increasing. A growing economy indicates that businesses are producing more goods and services, often leading to more jobs. On the other hand, slow growth can signal problems.

Inflation represents how quickly prices for goods and services are rising. While some inflation is normal, **high inflation** can erode purchasing power, making everything more expensive. Conversely, deflation can lead to reduced spending.

Unemployment rates reveal how many people are looking for jobs but can’t find them. High unemployment rates are usually bad for an economy, as they’re often tied to lower consumer spending and decreased economic growth. Governments use different policies to manage these economic factors.

Key Macroeconomic Indicators

Key macroeconomic indicators help us understand how an economy is performing. These include **Gross Domestic Product (GDP)**, **Consumer Price Index (CPI)**, and **unemployment rates**. GDP measures the total value of goods and services produced in a country.

The Consumer Price Index tracks changes in the price level of a market basket of consumer goods and services. It helps to measure inflation. An increasing CPI indicates rising prices, while a declining CPI shows falling prices.

Unemployment rates show the percentage of the labor force that is jobless. These rates provide insights into how well an economy can employ its workforce. Lower unemployment rates generally suggest a healthier economy.

Growth, Inflation, and Unemployment in Macroeconomics

Growth, inflation, and unemployment are closely linked. For instance, rapid economic growth can sometimes lead to high inflation. More people earn and spend money, driving up prices.

To keep inflation in check, central banks might raise interest rates. This action can slow down economic growth but helps stabilize prices. On the flip side, low inflation or deflation can lead to increased unemployment.

When prices fall, businesses may cut costs and lay off workers. This can start a cycle of reduced spending and even higher unemployment. Thus, managing these three factors is a delicate balance for policymakers.

Key Macroeconomic Indicators

Macroeconomic indicators are essential for understanding how an economy is doing. They provide insights into various economic activities. These indicators help governments and investors make informed decisions.

Gross Domestic Product (GDP)

Gross Domestic Product (GDP) measures the total value of all goods and services produced in a country over a specific period. It indicates the overall economic health. A rising GDP generally means the economy is growing.

Governments and economists closely monitor GDP. It helps them understand whether the economy is expanding or contracting. A declining GDP might signal a recession, which can have various negative effects on employment and income.

Countries often aim to increase their GDP through policies that promote business and investment. However, rapid GDP growth can sometimes lead to environmental issues. Thus, sustainable growth is crucial.

Consumer Price Index (CPI)

The Consumer Price Index (CPI) tracks changes in the prices of a selected basket of goods and services. It is a primary measure of inflation. Rising CPI indicates increasing prices, while falling CPI shows decreasing prices.

CPI includes items like food, housing, and transportation. People feel the impact of changing CPI in their daily lives. For example, higher CPI might mean spending more on groceries and rent.

Central banks use CPI to make decisions about interest rates. If CPI rises too quickly, a central bank might increase interest rates to cool down inflation. Conversely, if CPI falls, interest rates may be lowered to stimulate spending.

Unemployment Rate

The unemployment rate measures the percentage of the labor force that is jobless and actively seeking employment. High unemployment rates are generally a sign of economic trouble. Lower rates suggest a healthier economy.

An increasing unemployment rate often leads to lower consumer spending. People without jobs have less money to spend, which can slow economic growth. This can create a cycle where reduced spending leads to more job losses.

Governments use various policies to reduce unemployment. These can include job creation programs and training initiatives. The goal is to help people find work and contribute to the economy.

Growth, Inflation, and Unemployment in Macroeconomics

Economic growth, inflation, and unemployment are critical factors in understanding a country’s economic health. Growth measures the increase in a country’s output of goods and services. High growth rates indicate a strong economy, while low growth rates can signal underlying issues.

Inflation reflects the rate at which prices for goods and services rise. Moderate inflation is normal and often expected, but **high inflation** can erode people’s purchasing power. Conversely, deflation, or falling prices, can lead to decreased spending.

Unemployment rates show how many people are without jobs but looking for work. High unemployment often leads to lower consumer spending, which can slow down the economy. **Low unemployment** rates usually suggest that more people are working and spending money, boosting economic growth.

Managing these three elements is crucial for policymakers. When growth is too rapid, it can create inflationary pressures. Conversely, measures to control inflation can sometimes increase unemployment rates, creating a delicate balance.

Introduction to Rational Expectations Theory

Rational Expectations Theory suggests that people use all available information to make economic decisions. This means they try to predict future events as accurately as possible. Predicting inflation or other economic shifts helps them make better choices.

John Muth introduced this theory in the early 1960s. His idea changed how economists and policymakers viewed markets and decision-making. The theory assumes that markets are efficient and people act rationally.

One key aspect is how expectations influence real outcomes. If people expect prices to rise, they may buy more now, increasing demand and driving prices up. In this way, **expectations** can become self-fulfilling.

Governments and central banks use Rational Expectations Theory to shape policies. For example, they might provide clear guidance on future interest rates. This helps businesses and consumers plan better.

Transparency is critical in this context. When policymakers are straightforward about their actions, it helps stabilize the economy. Uncertainty, on the other hand, can lead to poor decision-making.

Critics argue that not everyone has access to the same information. This can lead to unequal outcomes. Despite this, Rational Expectations Theory remains a foundational concept in modern economics.

The Evolution of Rational Expectations Hypothesis

The Rational Expectations Hypothesis began with John Muth in the early 1960s. His revolutionary idea posited that people use available information efficiently to forecast economic variables. This notion challenged traditional views in economics.

Initially, many economists were skeptical. However, the concept gained traction in the 1970s. Lucas Critique, introduced by Robert Lucas, strengthened its validity, arguing that traditional models failed to account for policy changes.

During the 1980s, Rational Expectations became central to macroeconomic theory. Policymakers started considering how people’s future expectations impacted current economic actions. This led to more forward-looking economic policies.

Academic research also expanded in this domain. Studies explored how expectations influenced everything from inflation to business cycles. The Rational Expectations Hypothesis helped shape modern economic thought.

Despite its influence, the theory faces criticism. Some argue it assumes individuals have access to all information, which isn’t always the case. Nevertheless, it remains a cornerstone in economics.

Overall, the Rational Expectations Hypothesis has profoundly impacted how we understand and implement economic policy. Its evolution showcases the dynamic nature of economic theories. This continuous development keeps the field robust and relevant.

Key Assumptions and Principles of Rational Expectations Theory

The first key assumption of Rational Expectations Theory is that individuals use all available information efficiently. This means people won’t make systematic errors in their economic forecasts. They adjust their predictions based on the latest data.

Another important principle is that markets are generally clear. Supply and demand balance out because individuals act rationally. This doesn’t mean markets are always perfect, but they are usually efficient.

The theory also assumes that expectations influence actual outcomes. If people expect inflation to rise, they will act in ways that might cause inflation to go up. Expectations become self-fulfilling prophecies in this framework.

Rational Expectations Theory also takes into account that people learn from past mistakes. They don’t repeat the same errors frequently because they update their knowledge. This continuous learning keeps the market adaptable.

According to the theory, government and central bank policies should be transparent and predictable. Clear communication helps shape individuals’ expectations accurately. This, in turn, stabilizes the economy.

Critics argue these assumptions are too idealistic. Not everyone has access to all information, and irrational behavior can occur. Despite these criticisms, Rational Expectations Theory offers valuable insights into economic behavior.

Rational Expectations within The Framework of Macroeconomics

Rational Expectations Theory plays a significant role in macroeconomics. It helps to understand how people make economic decisions. When individuals use all available information, it impacts the broader economy.

One major area is inflation. People’s expectations about future prices can influence current spending and saving behaviors. If they expect higher prices, they might spend more now, boosting demand and raising prices.

This theory also affects how governments set policies. Policymakers need to be clear and predictable with their actions. Clear communication helps shape accurate public expectations, stabilizing economic conditions.

In macroeconomics, the theory suggests that traditional interventionist policies may not always work as intended. For example, stimulus measures might be less effective if people expect them to cause inflation later. Thus, rational expectations alter policy effectiveness.

Rational Expectations Theory also explains some persistent issues like stagflation. This term describes a situation with high inflation and high unemployment simultaneously. Understanding how expectations drive these phenomena helps develop targeted solutions.

The interplay between rational expectations and macroeconomic variables like GDP growth or unemployment provides deeper insights into economic health. Analysts use this framework to predict market behavior better and make informed decisions.

Rational Expectations and Inflation

Rational Expectations Theory greatly influences how we understand inflation. When individuals expect prices to rise, they often act in ways that make this expectation a reality. For example, people might buy more goods now to avoid higher prices later, increasing current demand and driving up prices.

Inflation expectations also impact wage negotiations. Employees might demand higher wages if they expect future inflation. Businesses, in turn, raise prices to cover the increased wage costs, leading to more inflation.

Central banks monitor these expectations closely. By influencing public perception, they attempt to control inflation. One common method is setting interest rates; raising rates can cool down an overheated economy.

Rational Expectations Theory suggests that central banks need to be transparent. Clear and predictable policies help anchor expectations, preventing erratic inflation. Unexpected policy changes can lead to economic instability.

To keep inflation in check, central banks might use tools like inflation targeting. This involves setting a publicly announced target for the inflation rate. If the public trusts this target, their behavior will align with it, helping to stabilize prices.

Understanding the role of expectations in inflation management highlights how interconnected economic variables are. It emphasizes the importance of clear communication and informed decision-making in economic policy.

Rational Expectations and Monetary Policy

Rational Expectations Theory greatly impacts monetary policy. People base their economic decisions on what they expect from central banks. If they expect interest rates to rise, they might save more and spend less.

Central banks like the Federal Reserve use these expectations to set policies. They might announce future interest rate changes to guide public behavior. Clear communication from the central bank helps stabilize the economy.

Predictability is crucial for effective monetary policy. When people trust that the central bank will act as stated, their expectations align with those policies. This reduces uncertainty and helps achieve economic goals.

Rational expectations also explain why unexpected monetary policy changes can cause problems. If people are caught off guard, it can lead to economic instability. Transparency minimizes these risks by setting clear expectations.

Inflation targeting is a tool that benefits from rational expectations. When a central bank commits to keeping inflation at a certain level, people’s behavior aligns with that target. This helps control inflation and supports economic stability.

Overall, Rational Expectations Theory shows the importance of clear, predictable, and transparent monetary policies. It highlights how public expectations shape real economic outcomes, making them vital for effective monetary policy.

Implication of Rational Expectations on Economic Policies

Rational Expectations Theory affects how governments and central banks create economic policies. People base their decisions on what they think will happen in the future. This makes policy predictability crucial for stabilizing the economy.

One major implication is that traditional policies might not work as planned. For example, fiscal stimulus may be less effective if people expect it to cause future inflation. Their anticipation could lead them to save rather than spend.

Clear communication from policymakers helps shape accurate public expectations. When people understand the government’s actions, they can make better financial decisions. This reduces economic uncertainty.

Transparency in policy-making is key. If central banks and governments are open about their actions, it helps align public expectations with actual policy goals. This alignment leads to more effective economic management.

Sometimes, unexpected policies can create instability. People might react unpredictably, causing market fluctuations. Consistent and transparent policies minimize these risks.

The theory also suggests that continuous learning and adapting are essential. As new information becomes available, both policymakers and the public must adjust their expectations. This dynamic process helps maintain economic stability.

Policy Implications of Rational Expectations

The Rational Expectations Theory changes how policymakers approach their tasks. It implies that individuals use all available information to predict future policies. This makes transparent communication essential for effective policy-making.

Monetary policy is highly influenced by this theory. Central banks need to clearly convey their future actions to shape the expectations accurately. This helps stabilize the economy, avoiding sudden market disruptions.

Fiscal policy also adapts to Rational Expectations. Governments must consider how people will react to spending and tax changes. If people expect higher future taxes, they may start saving more now, reducing the immediate impact of fiscal measures.

Another implication is the credibility of policymakers. If the public trusts the government’s promises, their expectations will align with the announced policies. This trust leads to more predictable and stable economic outcomes.

Rational Expectations also promote continuous learning. Both policymakers and the public must adapt their actions based on new information. This dynamic approach ensures that policies remain effective over time.

This theory encourages forward-thinking strategies. By considering how policies will influence expectations, governments can better manage economic stability. This proactive approach is crucial for sustained economic health.

The Impact of Rational Expectations on Fiscal and Monetary Strategies

Rational Expectations Theory plays a crucial role in shaping fiscal and monetary strategies. It suggests that people’s decisions are based on what they predict will happen in the future. This theory changes how governments and central banks approach policy-making.

In terms of fiscal policy, governments need to consider how their actions will be perceived. For instance, if they announce a big spending program, people might expect future tax hikes to pay for it. This could lead to lower current consumption and saving behavior changes.

The theory also affects monetary policy. Central banks must be transparent about their future plans for interest rates and inflation. Clear guidance helps people make better financial decisions, stabilizing the economy.

One tool influenced by this theory is inflation targeting. By committing to a specific inflation rate, central banks manage public expectations. If people trust the target, their behavior aligns with policy goals, helping maintain stable prices.

Effective communication is key. When central banks and governments are clear about their intentions, it helps to reduce uncertainty. This leads to more stable economic conditions.

However, unexpected policy changes can disrupt the economy. If people are caught by surprise, it can lead to erratic behavior. Consistent and predictable policies are essential for minimizing these risks.

Frequently Asked Questions

Here are some frequently asked questions related to macroeconomics and rational expectations. These responses aim to clarify key concepts and their implications in an engaging manner.

1. How does Rational Expectations Theory affect inflation?

Rational Expectations Theory affects inflation by influencing how people respond to predicted price changes. If people expect prices to rise, they might buy more goods now, increasing current demand and driving up prices.

This self-fulfilling nature means that people’s expectations directly impact real economic outcomes. Central banks use this understanding to communicate future policies clearly, aiming to stabilize inflation by shaping public expectations effectively.

2. Why is transparent communication important in Rational Expectations Theory?

Transparent communication is essential because it helps shape accurate public expectations. When central banks make their policies clear, individuals can plan accordingly, leading to more stable economic behavior.

This reduces uncertainty and prevents erratic actions that could destabilize the economy. Transparency ensures that the actions of policymakers align closely with the informed decisions of businesses and consumers.

3. What role does Rational Expectations play in monetary policy?

In monetary policy, Rational Expectations Theory suggests that individuals use all available information when making financial decisions. This means central banks must clearly communicate their plans for interest rates and inflation.

If people know what to expect, they can make better financial choices, stabilizing the economy. Predictable policies help maintain economic stability by aligning public behavior with policy objectives.

4. How do Rational Expectations influence fiscal policy?

Rational Expectations also affect fiscal policy by shaping how people react to government spending and taxation announcements. If they expect higher taxes in the future due to increased spending today, they might save more now instead of spending.

This behavioral response can dampen the intended stimulative effects of fiscal policies designed to boost consumption or investment, demonstrating the need for credible and well-communicated government strategies.

5. Can unexpected economic policies create instability?

Yes, unexpected policy changes can lead to economic instability as individuals struggle to adjust quickly to new information. Sudden shifts can cause confusion and erratic decision-making among businesses and consumers.

This is why consistent and predictable policies are crucial for maintaining economic stability. A clear framework helps manage expectations effectively, reducing the risk of unpredictable market behaviors.

Conclusion

Rational Expectations Theory has significantly reshaped macroeconomic policies and thought. By emphasizing the importance of transparent communication and predictable policies, it offers critical tools for economic stability. Central banks and governments can better manage inflation, growth, and unemployment by aligning public expectations with policy objectives.

Despite criticisms, the theory continues to provide valuable insights. Its impact on both fiscal and monetary strategies highlights the interconnectedness of modern economies. As the field evolves, the principles of Rational Expectations will remain a cornerstone of effective economic policy-making.