In the mid-20th century, the notion that government intervention could potentially stabilize the economy seemed revolutionary. Who could have predicted that ideas developed during the Great Depression would shape policies for decades to come? Such shifts in thought underscore the dynamic nature of macroeconomics, a field continually evolving in response to real-world challenges.

The evolution of macroeconomic thought has traversed from classical theories of self-regulating markets to Keynesian advocacy for fiscal policy intervention. The 1970s introduced the concept of stagflation, challenging existing economic doctrines. Now, modern macroeconomics integrates behavioral insights and considers global interconnectedness, reflecting a progressively nuanced understanding of economic systems.

The Origins of Macroeconomic Thought

Classical Economics and the Invisible Hand

Classical economics began in the 18th century with thinkers like Adam Smith. He introduced the concept of the “invisible hand,” which suggests that individual self-interest can lead to societal benefits. This theory emphasized minimal government intervention.

In classical economics, the market is believed to naturally regulate itself. Prices and wages adjust to achieve equilibrium. Smith’s ideas formed the foundation of economic thought for many years.

Ultimately, this era put a strong focus on the power of free markets. These principles dominated economic policies until the 20th century. It shaped the basis for future economic theories.

Marxist Response to Classical Economics

Karl Marx, in the mid-19th century, critiqued classical economics. He felt that the free market led to inequality and exploitation. His work, “Das Kapital,” introduced a different view.

Marxist economics focuses on the struggles between classes. He argued for a system where resources and power are more evenly distributed. This theory influenced many political movements worldwide.

Marx’s ideas offered an alternative to the classical ways. This led to discussions and debates about the best economic paths. It showed that economics could be approached from many angles.

The Great Depression’s Role in Keynesian Thought

The Great Depression of the 1930s had a massive impact. Traditional economic policies could not address the widespread unemployment and poverty. John Maynard Keynes introduced new ideas to tackle these problems.

Keynes suggested that government intervention was necessary. His theory recommended public spending to boost economic activity. This gave rise to Keynesian economics, shifting away from pure free-market concepts.

Many countries adopted these ideas to stimulate economies. This marked a significant evolution in economic thought. Keynes showed that government could play an active role in stabilizing economies.

Behavioral Economics and the Rational Agent

More recently, behavioral economics emerged. It challenged the idea that individuals always act rationally. Researchers found that emotions and psychology deeply influence economic decisions.

This approach considers more than just numbers and models. It looks at how people really behave in different situations. Behavioral economics aims to make economic theories more realistic.

By understanding human behavior, policies can be more effective. This evolution represents a significant shift in how we view economics. It bridges the gap between theory and real-life human actions.

Classical Economics and the Invisible Hand

Classical economics, one of the earliest economic theories, focuses on free markets and minimal government interference. Adam Smith introduced the idea of the “invisible hand”. This concept argues that individuals’ pursuit of self-interest unintentionally benefits society as a whole.

Adam Smith and His Contributions

Adam Smith, often called the father of economics, published “The Wealth of Nations” in 1776. He proposed that free markets, driven by self-interest, lead to efficient outcomes. Smith’s work established key economic principles still relevant today.

Smith’s invisible hand theory suggests markets regulate themselves. This happens through competition and consumer choices. People acting in their interest inadvertently help others.

Smith’s influence extended beyond economics. His ideas shaped capitalist systems worldwide. This marked a significant shift from earlier economic thought.

Principles of Classical Economics

Classical economics emphasizes laissez-faire policies. This means limited government intervention in markets. The belief is that economies function best when left alone.

Key principles include free trade and competition. Classical economists advocate for open markets. They argue this leads to innovation and growth.

Resource allocation is another principle. It posits that resources are best distributed by market forces. Supply and demand determine prices and production.

Impact on Modern Economic Policies

The ideas from classical economics remain influential. Many modern policies are based on Smith’s theories. For example, free-market capitalism stems from classical principles.

However, real-world challenges sometimes require intervention. Economic crises and inequalities call for balanced approaches. Hence, classical ideas are often blended with new theories.

Governments today still weigh these classical principles. They seek to find the right balance between intervention and free markets. This ongoing dialogue shapes economic policy.

Marxist Response to Classical Economics

Karl Marx offered a strong critique of classical economics in the 19th century. He believed it ignored the struggles of the working class. Marx argued that wealth created by laborers was unfairly distributed, benefiting only the capitalists.

Marx’s main work, “Das Kapital,” highlighted the flaws of capitalism. He felt that it led to exploitation and economic crises. Marx proposed a different approach where resources were shared more equally.

Marx introduced the concept of class struggle. He believed that history was a series of conflicts between different classes. This perspective shifted the focus from individual actions to social structures.

Marxist economics has influenced many political movements. Countries like the Soviet Union tried to implement his ideas. While his theories are controversial, they remain a significant part of economic discussions.

The Emergence of Keynesian Economics

The emergence of Keynesian economics marked a significant shift. During the Great Depression of the 1930s, traditional economic theories failed. Mass unemployment and economic stagnation demanded new approaches.

John Maynard Keynes, a British economist, introduced revolutionary ideas. He argued that free markets alone couldn’t solve economic crises. Keynes believed that **government intervention** was essential.

Keynes proposed that public spending could boost demand. This would, in turn, create jobs and stimulate economic activity. His ideas formed the basis of modern macroeconomics.

Many governments adopted Keynesian policies. They increased spending on infrastructure and other projects. This aimed to reduce unemployment and jumpstart the economy.

Keynesian economics is especially relevant during recessions. Governments often use it to stabilize economies. This theory remains influential in economic policy-making today.

Over time, Keynesian thought has evolved. It now includes concepts like fiscal policy and demand management. These tools help manage economies in times of crisis.

The Great Depression’s Role in Keynesian Thought

The Great Depression severely impacted economies worldwide. Traditional economic theories couldn’t explain the prolonged crisis. During this time, John Maynard Keynes presented his revolutionary ideas.

Keynes observed that the free market was failing. Unemployment was at an all-time high. People weren’t spending, which further worsened the situation.

He proposed that governments should intervene. By increasing public spending, the economy could be stimulated. This, in turn, would create jobs and increase demand.

Keynes argued that investment in infrastructure could help. For instance, building roads and bridges would not only provide jobs but also improve the economy. Public projects became a cornerstone of Keynesian policy.

Governments began adopting his ideas. The U.S. implemented programs like the New Deal to combat the Great Depression. These initiatives mirrored Keynesian principles.

The success of these policies validated Keynes’s theories. His work laid the foundation for modern economic practices. Even today, during recessions, governments use similar strategies.

Government Intervention in Market Economy

Government intervention plays a crucial role in market economies. During economic crises, such as the Great Depression, traditional free-market policies often fail. Keynes proposed that active government involvement could stabilize the economy.

One form of intervention is fiscal policy. Governments can increase public spending on infrastructure, education, and healthcare. This helps create jobs and stimulate economic growth.

Monetary policy is another important tool. Central banks can adjust interest rates and control the money supply. These measures aim to ensure stable economic conditions.

Regulation and oversight are also key. Governments set rules to protect consumers and ensure fair competition. This includes regulations on banking, environment, and labor standards.

While intervention has many benefits, it also faces criticism. Some argue it leads to inefficiency and stifles innovation. Therefore, finding a balance between free markets and regulation is essential.

Overall, government intervention aims to correct market failures. It provides safety nets during downturns and can guide sustainable growth. In times of crisis, intervention becomes even more vital.

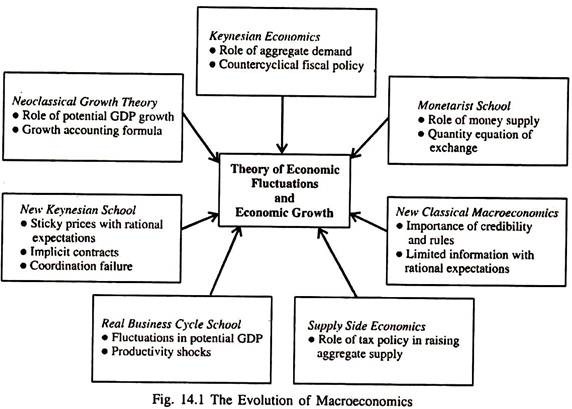

The Neo-Keynesian and Neo-Classical Revolution

The Neo-Keynesian and Neo-Classical revolution spurred new thought waves in economics. After World War II, economists combined ideas from both schools. This fusion aimed to better explain economic behavior.

Neo-Keynesian theorists expanded on Keynes’s original concepts. They included the role of wages and price adjustments in their models. These theories emphasized the importance of government policies during economic downturns.

Conversely, Neo-Classical economists focused on free markets. They argued that when left alone, these markets naturally find equilibrium. Rational expectations became a focal point in their analysis.

This led to intense debates between the two schools. But it also resulted in more robust economic models. The combination of both perspectives offered a balanced view of modern economies.

The policy mix from this period influenced many countries. For example, governments adopted strategies that included both intervention and market freedom. This approach aims to harness the strengths of each school.

Today, elements of both theories are integrated into economic planning. Policymakers use tools like fiscal stimuli and monetary control to maintain stability. This ongoing evolution continues to shape global economic policies.

Reconsideration of Free Market Principles

The reconsideration of free market principles has been a crucial part of economic thought’s evolution. In the mid-20th century, crises like the Great Depression challenged pure free-market beliefs. Economists started to explore alternative approaches.

One major contributor was John Maynard Keynes. He argued that unchecked free markets couldn’t always self-correct. His ideas led to a greater acceptance of government intervention in economies.

Reconsidering free market principles involves balancing freedom and regulation. While free markets drive innovation, they can also create inequalities. Finding the right mix is challenging but essential.

Modern economic thought integrates both ideas. Regulations ensure fair practices and consumer protection. Meanwhile, market freedom encourages businesses to grow and compete.

Many countries adopt a hybrid approach today. They use a mix of market freedom and government oversight. This helps address flaws while maintaining the benefits of both systems.

This balanced view continues to shape policies. It influences everything from trade laws to environmental regulations. The ongoing reconsideration of free market principles is vital for adapting to new challenges.

Monetarism and the Modern Central Bank

Monetarism emerged as a powerful economic theory in the mid-20th century. Economist Milton Friedman was a leading advocate. He argued that the government should control money supply to manage the economy.

Friedman believed that inflation is always a monetary phenomenon. If the money supply grows too quickly, prices rise. Controlling money supply can help stabilize economies.

Modern central banks play a key role in this theory. They manage interest rates and regulate money supply. This helps to curb inflation and ensure economic stability.

Central banks use various tools to achieve their goals. These include open market operations, reserve requirements, and discount rates. By adjusting these, they influence economic activity.

Monetary policies are crucial during financial crises. For example, during the 2008 recession, central banks worldwide adjusted interest rates. This aimed to support struggling economies.

While monetarism has its critics, its principles remain influential. Central banks today continue to use these methods. Their actions impact everything from loan rates to employment levels.

Modern-Day Macroeconomic Thought

Modern-day macroeconomic thought is a blend of various theories. It incorporates ideas from Keynesian, classical, and monetarist schools. This blend helps address complex economic challenges.

One major focus is on behavioral economics. This field explores how psychological factors affect economic decisions. It challenges the notion that people always act rationally.

Another key element is globalization. The interconnected nature of today’s economies makes global trade and policies crucial. Countries must consider international impacts on their domestic policies.

Sustainability is also a growing concern. Modern economics looks at long-term environmental impacts. Policies now often include measures to combat climate change and promote green technology.

Technology has a significant influence on modern economics. Innovations like artificial intelligence and blockchain are transforming how markets operate. Economists study these changes to understand their effects on the economy.

Modern macroeconomic thought aims to be flexible and adaptive. By incorporating diverse theories, it strives to create balanced and effective policies. This approach helps navigate the complexities of today’s global economy.

Behavioral Economics and the Rational Agent

Behavioral economics challenges the traditional notion of the rational agent. Traditional economics assumes people always make rational decisions. However, real-life decisions often deviate from this idea.

Researchers have found that emotions play a big role. Factors like fear, joy, and even fatigue can affect choices. This research helps make economic models more realistic.

One famous example is the concept of “loss aversion”. People tend to prefer avoiding losses over acquiring gains. This insight helps explain why people sometimes make seemingly irrational decisions.

- Loss Aversion: Prefer avoiding losses.

- Anchoring: Relying heavily on the first piece of information.

- Overconfidence: Overestimating one’s abilities.

Behavioral economics also explores financial decisions. Studies show that people often save less than they should. By understanding behavior, policies can be designed to encourage better saving habits.

This field has practical applications too. Businesses use these insights for marketing strategies. Policymakers can design better interventions based on this understanding.

Behavioral economics thus bridges the gap between theory and real life. It enriches our understanding of how people actually behave. This makes it a vital part of modern economic thought.

The Role of Globalization in Macroeconomics

Globalization has a significant impact on macroeconomics. It connects economies worldwide through trade, investment, and communication. This increased interdependence shapes economic policies and outcomes.

One primary effect is on international trade. Countries export and import goods more freely. This creates more competition and can drive innovation and efficiency.

Exchange rates are another critical aspect. Fluctuations can affect a country’s economic stability. Central banks often intervene to manage these changes and stabilize their economies.

Labor markets are also influenced by globalization. Workers can move across borders more easily. This provides opportunities for employment but also challenges in terms of wages and job security.

| Impact | Examples |

|---|---|

| Trade | Increased exports and imports |

| Exchange Rates | Currency value fluctuations |

| Labor Markets | Cross-border employment |

Foreign investments are boosted by globalization. Companies invest in other countries to expand their reach. This can grow economies but also increase risks.

Global financial crises are another consequence. Economic problems in one country can spread. Policymakers must work together to address these global challenges effectively.

Overall, globalization deeply affects macroeconomic strategies. Countries must navigate the benefits and drawbacks. It’s a key factor in shaping today’s interconnected world economy.

Frequently Asked Questions

This section covers some common questions related to the evolution of macroeconomic thought. Understanding these answers will help clarify key concepts.

1. What is classical economics?

Classical economics is a theory that promotes free markets with minimal government intervention. Adam Smith introduced ideas like the “invisible hand” that suggest individual actions can benefit society as a whole.

This theory dominated economic thought until the early 20th century. Key principles include laissez-faire policies and self-regulating markets based on supply and demand.

2. How did Keynesian economics change economic policies?

Keynesian economics shifted focus towards active government intervention during economic downturns. John Maynard Keynes argued that public spending could boost demand, create jobs, and stabilize economies.

During the Great Depression, many governments adopted Keynesian policies. These measures helped mitigate unemployment and encouraged economic recovery through infrastructure projects.

3. What is monetarism?

Monetarism is an economic theory emphasizing the control of money supply to manage the economy. Milton Friedman was a key proponent who believed inflation is always linked to monetary factors.

This theory argues that controlling money supply can stabilize prices and growth. Central banks use tools like interest rate adjustments to influence the economy under this framework.

4. How does behavioral economics differ from traditional theories?

Behavioral economics challenges traditional views by incorporating psychological aspects into economic models. It suggests that people often make irrational decisions based on emotions and cognitive biases.

Examples include concepts like loss aversion, where individuals prefer avoiding losses over acquiring gains. This field provides a more realistic view of human decision-making compared to classical rational-agent models.

5. How has globalization impacted modern macroeconomics?

Globalization connects economies worldwide through trade, investment, and technology transfer. This interconnectedness affects everything from exchange rates to labor markets, making global coordination essential for stability.

Countries must consider international impacts when forming domestic policies. Global financial crises exemplify how economic issues in one nation can quickly spread across borders, requiring unified global strategies.

Conclusion

The evolution of macroeconomic thought reflects the dynamic nature of economies. From classical theories to modern behavioral insights, each stage has contributed valuable perspectives. This continuous development helps policymakers navigate complex economic landscapes.

Understanding these changes is crucial for effective economic policies. By blending different theories, we can address both traditional and contemporary challenges. This holistic approach ensures a more stable and resilient global economy.