With every passing day, around 10,000 Baby Boomers turn 65, preparing to step into retirement. This striking trend has profound implications for the U.S. economy, prompting a wave of considerations in sectors like healthcare and social security. How will the country manage the demands of an aging population?

The aging population is not a new phenomenon in American history, but its current scale is unprecedented. By 2030, all Baby Boomers will have passed the retirement age, representing nearly 20% of the total U.S. population. This demographic shift places immense pressure on social safety nets and challenges the sustainability of economic growth.

The Shift in Demographics: Aging Population in the United States

The U.S. population is getting older rapidly. By 2030, all Baby Boomers will be over 65. This means nearly 20% of the U.S. population will be in retirement age.

This significant demographic shift poses various challenges. With more people retiring, the workforce is shrinking. Fewer workers can lead to slower economic growth.

Healthcare demands are also growing due to this aging population. Older people generally need more medical care, placing stress on hospitals and clinics. This increases healthcare costs for everyone.

Retirement savings and pensions will also be impacted. Many retirees rely on social security and other government programs. These systems must adapt to support the growing number of older adults.

Economic Impact of an Aging Population

The aging population affects the economy in multiple ways. One major issue is the decline in labor force participation. Fewer workers may result in reduced overall productivity.

Moreover, as older people spend their savings, there may be less money available for investment. This can slow down technological advancements and business growth. The economy might face challenges keeping up with global competitors.

However, there are also opportunities. Older adults can contribute as volunteers or part-time workers. Their experience and knowledge can benefit communities and businesses.

Healthcare Challenges and Solutions

Healthcare systems need to adapt to an aging population. One approach is to increase healthcare funding and resources. More doctors and nurses will be necessary to handle the increased demand.

Innovations in medical technology can also help. Telemedicine, for instance, allows older adults to receive care from home. This can reduce hospital visits and lessen the burden on the healthcare system.

Preventive care programs can keep older adults healthy longer. Regular check-ups and healthy lifestyles can reduce the need for extensive medical treatments. This can save costs and improve quality of life.

Social and Cultural Impacts

An aging population can change societal structures. Grandparents may spend more time with grandchildren, providing valuable family support. Communities might develop more senior-friendly infrastructure.

Culturally, the aging population brings a wealth of history and knowledge. This can enrich communities through storytelling and mentorship programs. Younger generations can learn a lot from their elders.

Housing markets may shift to accommodate more senior living facilities. These changes can also spur economic growth in new sectors, creating jobs and opportunities in senior care and services.

The Pressure on Social Safety Nets

The increasing number of retirees places a heavy burden on social safety nets. Social Security and Medicare, key programs supporting the elderly, face significant financial challenges. These systems are straining to keep up with the growing demand.

An aging population means higher costs for healthcare services. Older adults tend to require more medical attention, causing healthcare expenses to rise. This puts immense pressure on public healthcare funding.

Many states struggle to meet the needs of their elderly populations. Budget constraints limit the ability to expand or enhance social services. Consequently, some seniors are not receiving the support they need.

It’s vital to find sustainable solutions to maintain these safety nets. Reforming these programs can help ensure their long-term viability. Policymakers must balance resources effectively to support the aging population.

Impact on Social Security

Social Security is a lifeline for many older Americans. However, the increasing number of beneficiaries risks depleting its funds. The ratio of workers to retirees is shrinking.

This shift puts a financial strain on the Social Security system. Without adjustments, it could face severe shortfalls in the coming years. Potential changes may include raising the retirement age or altering benefit calculations.

Maintaining Social Security’s solvency is crucial. Effective policy measures can help secure its future. This will provide ongoing support for retirees and the disabled.

Healthcare Demands

Medicare is another key program under pressure. With more people living longer, the demand for healthcare services has surged. Older adults typically need more frequent and complex medical care.

Funding Medicare adequately is a pressing concern. To keep up with rising costs, the system may require additional revenue streams. Policymakers may consider options like higher taxes or shifting some costs to beneficiaries.

Innovation in healthcare delivery can also help. Ideas like telemedicine and preventive care programs can reduce costs. These approaches can make healthcare more accessible and efficient for seniors.

State-Level Challenges

States face varying degrees of pressure from aging populations. States with higher proportions of older adults struggle more. The demand for state-funded services such as housing assistance and transportation increases significantly.

Budgets are often tight, limiting the ability to expand these services. States must find creative solutions to meet seniors’ needs. This might involve public-private partnerships or community-based initiatives.

Ensuring seniors receive adequate support is a complex task. Effective state policies are essential. These policies can help address the unique challenges posed by aging populations.

The Economic Repercussions: Growth, Productivity and Innovation

An aging population can slow down economic growth. Fewer workers mean less overall productivity. This can lead to a weaker economy.

Older workers often retire, reducing the available workforce. Fewer workers can mean businesses produce less. This makes it harder to compete on a global scale.

Innovation may suffer as well. Younger workers tend to drive technological advancements. With a smaller pool of younger employees, innovation might slow.

However, there are ways to counter these effects. Investing in automation and technology can boost productivity. Also, tapping into the experience of older workers can provide valuable insights.

The Role of Retirement Savings in the Economy

Retirement savings play a crucial role in the economy. When people save for retirement, they invest money in various financial assets. These investments help fuel economic growth.

As people retire, they begin drawing on their savings. This spending boosts the economy by increasing demand for goods and services. Retirees often spend on healthcare, travel, and housing.

However, there are risks if people don’t save enough for retirement. Insufficient savings can lead to increased dependence on government programs. This puts more pressure on social safety nets.

Encouraging retirement savings is essential. Tax incentives and employer-sponsored plans can help. These measures ensure people are financially secure in their later years.

Financial literacy is also important. Educating people about saving and investing can lead to better financial decisions. This benefits both individuals and the broader economy.

Lastly, retirees’ spending patterns affect different sectors differently. For example, healthcare and leisure industries may see more growth. Understanding these patterns helps forecast economic trends.

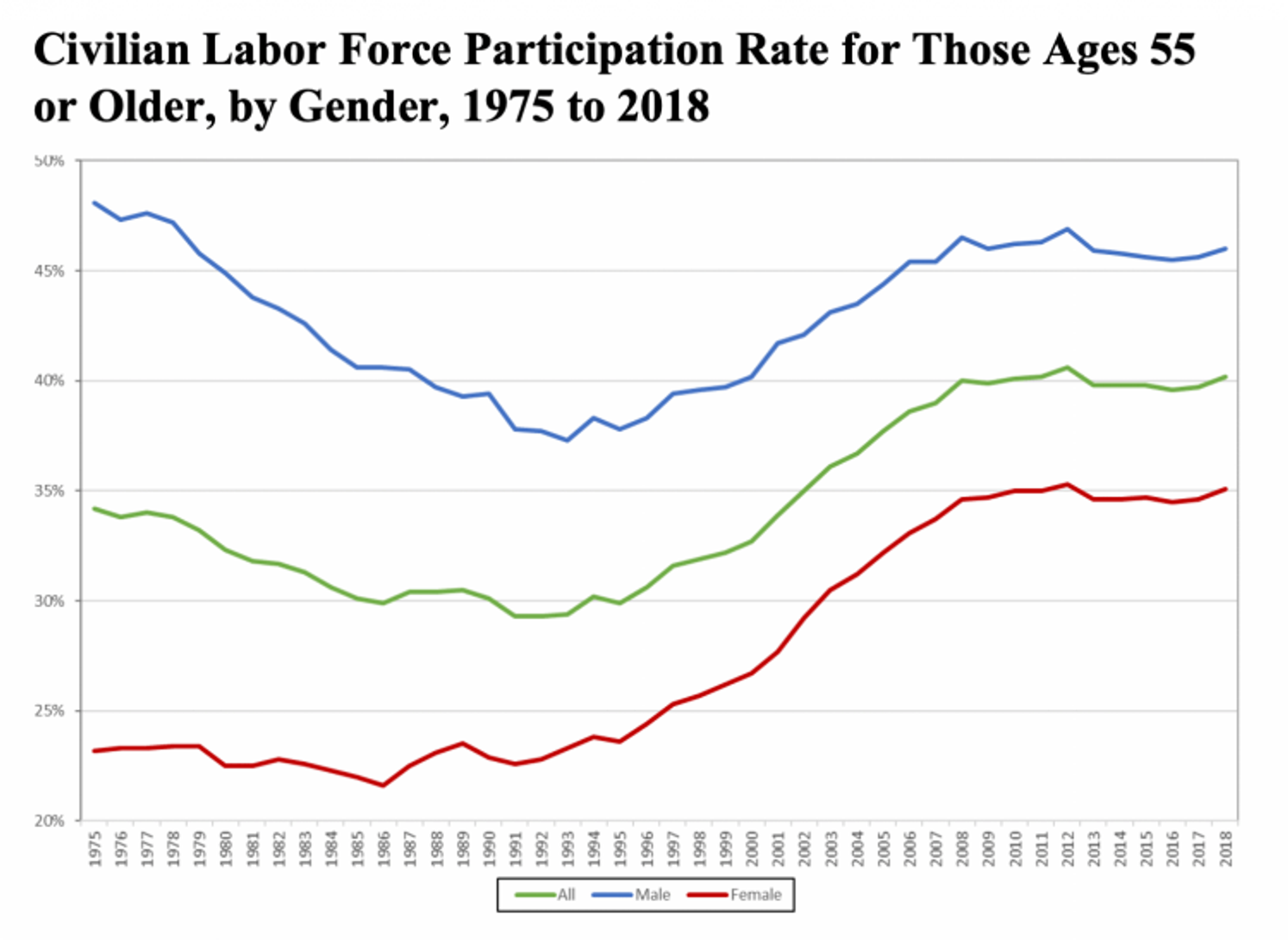

Labor Market Dynamics and Aging Population

An aging population can significantly impact labor market dynamics. As more people retire, the available workforce decreases. This can lead to labor shortages in various sectors.

Older workers often possess valuable skills and experience. However, their retirement creates a gap that younger workers must fill. The challenge is ensuring that younger workers have the necessary training.

Employers may need to adapt to retain older employees longer. Offering flexible work arrangements and part-time opportunities can help. This keeps experienced workers in the labor force.

Automation and technology can also play a role. By integrating new technologies, businesses can maintain productivity despite a smaller workforce. Robotics and AI are becoming increasingly important.

The shift in labor market dynamics can also affect wages. Labor shortages may lead to higher wages as companies compete for qualified workers. This could drive up operational costs.

Governments might need to adjust policies to support the changing workforce. This includes investing in education and retraining programs. Preparing younger generations for a shifting job market is crucial.

Policy Initiatives to Adjust for Aging

Many governments are implementing policy initiatives to manage an aging population. These initiatives aim to ensure that social support systems remain sustainable. One crucial focus is on healthcare.

Investing in healthcare infrastructure is essential. Governments are allocating funds to build more hospitals and clinics. They are also training more healthcare professionals to meet growing demands.

Social security programs need reforms to stay viable. Some countries are gradually increasing the retirement age. This helps balance the ratio of workers to retirees.

Offering tax incentives for retirement savings can encourage individuals to save more. These incentives help reduce the future burden on social security systems. Governments can also promote private pension plans.

Many countries support lifelong learning and retraining programs. These programs help older workers stay active in the labor market. Continuing education benefits both individuals and the economy.

Investing in research and development is also critical. Innovations in healthcare technology can improve efficiency and access. These advances ultimately reduce costs and enhance quality of care for seniors.

The Future Outlook: Population Aging and the U.S. Economy

Population aging will shape the U.S. economy significantly in the coming years. With more people retiring, certain industries will change rapidly. Healthcare and senior services may see the most growth.

Technological advancements can offset some challenges posed by an aging workforce. Automation and AI will help maintain productivity levels despite fewer workers. This could keep some industries competitive on a global scale.

Younger generations might need to shoulder more responsibility. They could face higher taxes to support social security and healthcare systems. Preparing for these changes now is crucial.

Investing in lifelong learning programs can help older adults stay in the workforce longer. These programs can provide new skills for different job markets. This benefits both individuals and the economy as a whole.

Economic growth may slow due to a smaller working-age population, but strategic investments can mitigate this risk. Governments must focus on sustainable policies that adapt to demographic shifts effectively. This includes boosting funding for research and development.

The housing market might also change as more seniors look for age-friendly living spaces. There could be increased demand for assisted living facilities and accessible homes, which offers opportunities in real estate development.

Case Studies: Lessons from Other Economies

Looking at other countries can offer insights into managing an aging population. Japan, for example, has one of the world’s oldest populations. They have implemented unique solutions to address this.

In Japan, robots are increasingly used in elder care. This helps reduce the workload on human caregivers. Robots assist with daily tasks like lifting and moving patients.

Sweden focuses on preventive healthcare to keep seniors healthy longer. Regular check-ups and wellness programs are emphasized. This reduces the need for extensive medical treatments.

Germany has a well-structured pension system. It combines public and private savings plans. This ensures that retirees have a stable income.

Some European countries have adopted flexible retirement policies. These allow older workers to gradually reduce their hours. This keeps experienced individuals in the workforce longer.

These case studies highlight different strategies. By learning from them, the U.S. can develop effective policies to manage its own aging population. This will help sustain economic growth and improve the quality of life for seniors.

Frequently Asked Questions

The aging population is a significant factor affecting the U.S. economy. Here are some frequently asked questions that delve into various aspects of this topic.

1. How does the aging population affect healthcare costs?

An aging population leads to higher healthcare costs due to increased demand for medical services. Older adults typically require more frequent and intensive healthcare, putting pressure on hospitals and clinics.

This growing demand raises overall healthcare expenses, impacting both public funding and private insurance premiums. Technological innovations and preventive care programs are essential in managing these escalating costs effectively.

2. What changes can be made to Social Security to support an aging population?

Several reforms can help support Social Security amid an aging population, such as raising the retirement age or adjusting benefit calculations. These changes aim to balance the ratio of workers to retirees, ensuring long-term sustainability.

Additionally, increasing payroll taxes or introducing new revenue streams could bolster Social Security funds. Implementing comprehensive policy adjustments ensures that future retirees receive adequate financial support without overburdening younger workers.

3. What role does technology play in addressing challenges posed by an aging workforce?

Technology, including automation and artificial intelligence (AI), plays a crucial role in mitigating labor shortages caused by an aging workforce. By streamlining operations and increasing productivity, these technologies can compensate for a reduced number of workers.

Innovations like telemedicine also improve healthcare accessibility for seniors, reducing strain on physical facilities. Leveraging technology ensures businesses and healthcare systems remain effective despite demographic shifts.

4. How do other countries manage their aging populations?

Countries like Japan use robotic technology in elder care to alleviate caregiver burdens and maintain service quality. Sweden emphasizes preventive healthcare with regular check-ups to keep seniors healthy longer, reducing extensive medical treatments.

Germany combines public and private pension plans for stable retiree income while European countries offer flexible retirement policies allowing older workers gradual reductions in work hours. Learning from these strategies can inform U.S. policy development to handle similar challenges effectively.

5. How can younger generations prepare financially for an aging society?

Younger generations should prioritize saving for retirement through employer-sponsored plans or tax-advantaged accounts like IRAs or 401(k)s early on in their careers. Financial literacy education helps them make informed decisions about savings and investments.

Diversifying investments across various asset classes ensures financial resilience amidst economic shifts caused by demographic changes. Proactive preparation helps reduce future reliance on government programs while promoting personal financial stability during retirement years.

Conclusion

The aging population in the U.S. presents both challenges and opportunities for the economy. Addressing healthcare costs, labor market shifts, and social security sustainability is crucial. Strategic policies and technological advancements offer promising solutions.

By learning from other countries and implementing effective reforms, the U.S. can better manage the economic impacts of an aging population. Proactive measures today will ensure a stable and prosperous future. Collaboration across sectors is key to success.