Think about this: even the most seasoned investors, armed with the best strategies, can falter if they misunderstand their personal risk tolerance. It’s a crucial element often overlooked in the euphoria of potential gains. Understanding one’s risk capacity can spell the difference between long-term success and devastating losses.

Historically, the concept of risk tolerance has evolved, becoming a cornerstone of investment strategy. A 2022 study revealed that 68% of investors who aligned their investments with their risk tolerance saw more consistent returns. This illuminates the vital importance of self-awareness in the high-stakes world of investing.

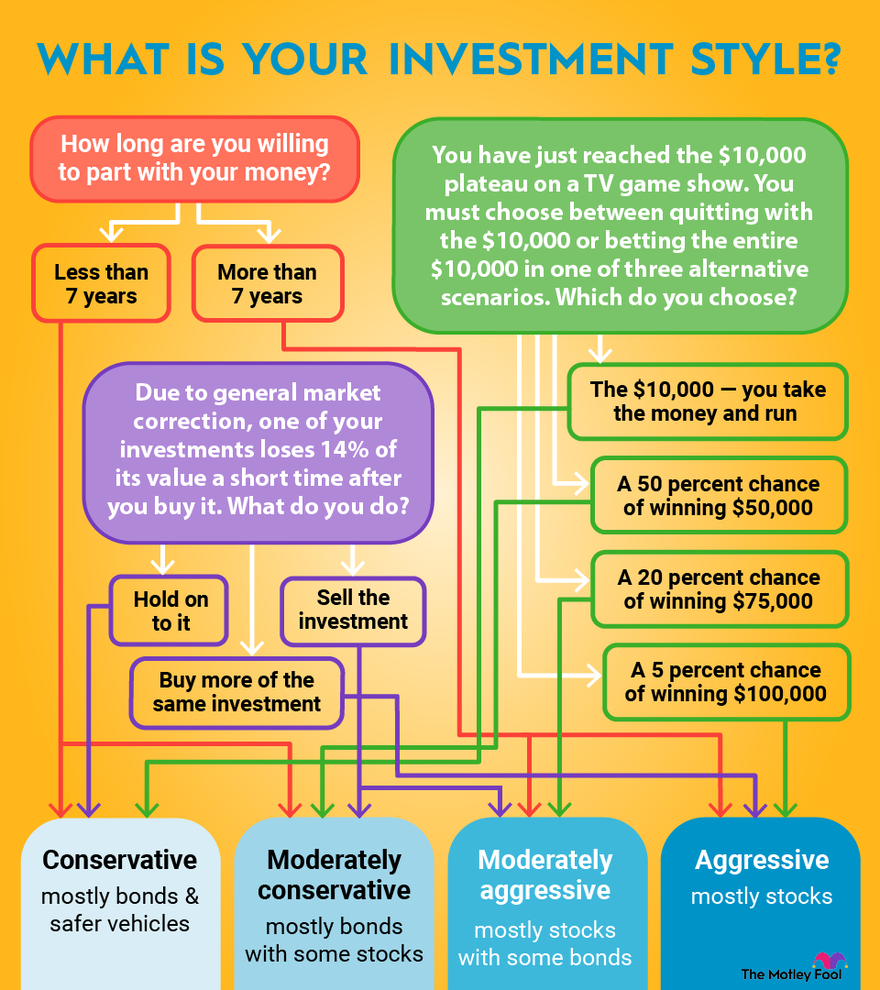

Defining Risk Tolerance in Investment

Risk tolerance in investment is how much uncertainty an investor can handle. It’s personal and varies from person to person. Some people might be comfortable with high risks, while others are more cautious.

Several factors influence risk tolerance, such as age, income, and financial goals. Younger investors often have a higher risk tolerance. They have more time to recover from potential losses.

Investors can evaluate their risk tolerance through various methods. Some use online questionnaires, while others prefer financial advisors. It’s essential to get a clear understanding before making investment choices.

Knowing your risk tolerance helps in building a balanced portfolio. It guides the mix of stocks, bonds, and other assets. This balance can lead to more consistent and satisfying returns.

Key Components of Risk Tolerance

Understanding the key components of risk tolerance helps investors make informed decisions. These components include financial situation, investment goals, and emotional resilience. Each factor plays a crucial role in shaping one’s risk tolerance profile.

Financial Situation

Your financial state affects how much risk you can take. Those with steady income and savings can manage higher risks. Conversely, individuals with unstable finances should be more cautious.

Consider your debts and monthly expenses. High debt levels may limit your risk tolerance. Ensuring your financial stability is key.

Create a budget to understand where your money goes. This will help you see how much you can invest safely. Knowing your finances well reduces the stress of investing.

Investment Goals

Investment goals also impact risk tolerance. Short-term goals usually require lower risk strategies. In contrast, long-term goals can handle more risk.

Think about why you’re investing. Is it for retirement, buying a house, or funding education? Each goal demands a different risk approach.

Write down your goals to visualize them clearly. Align your investments with these objectives. This ensures your investments serve their purpose.

Emotional Resilience

Emotion plays a significant role in investing. Some people can handle market ups and downs with ease. Others may panic and make poor decisions.

Ask yourself how you react to financial losses. If you stress easily, you might prefer safer investments. Understanding your emotional limits is crucial.

Work on building your emotional resilience. This helps you stay calm during market volatility. Staying composed leads to better long-term results.

Impact of Psychological Factors on Risk Tolerance

Psychological factors heavily influence risk tolerance. People with a risk-averse personality tend to avoid high-risk investments. A person’s experiences and emotions shape their comfort levels with risk.

Fear of loss is a predominant factor. Those who have experienced financial losses may become more cautious. This fear can limit their willingness to take on new opportunities.

Optimism and confidence impact risk tolerance too. Optimistic individuals are more likely to take risks in hopes of higher returns. However, overconfidence can lead to unwise decisions.

Understanding these psychological components can help investors make balanced choices. By acknowledging their emotional responses to risk, they can develop strategies to manage them. This awareness leads to more effective investment decisions.

The Role of Risk Tolerance in Portfolio Construction

Risk tolerance is crucial in portfolio construction. It determines the mix of assets an investor should hold. Understanding this helps build a portfolio that aligns with individual comfort levels.

A balanced portfolio should reflect the investor’s risk tolerance. For those with higher tolerance, more stocks may be suitable. They typically offer higher returns but come with greater risks.

On the other hand, conservative investors may prefer bonds and mutual funds. These have lower risk but also lower potential returns. This balance helps provide stability.

Frequent assessment of risk tolerance is essential. Life circumstances and financial goals can change. Regular reviews ensure that the portfolio remains suitable.

Investors should also diversify their portfolios. Diversification spreads risk across different asset types. This approach can mitigate potential losses.

Consulting with a financial advisor can be helpful. Advisors can offer professional insights on risk tolerance. They assist in building a portfolio tailored to the investor’s needs.

Aligning Investments with Risk Tolerance

Aligning investments with risk tolerance ensures that an investor’s portfolio matches their comfort level. It’s essential to choose assets that fit one’s risk capacity. A mismatch can lead to stress and poor decision-making.

Stock investments may suit those with higher risk tolerance. Stocks tend to be more volatile but offer higher returns. These investors can potentially gain more over the long term.

Conversely, safer investments like bonds or certificates of deposit (CDs) are ideal for conservative investors.

- Bonds provide steady income

- They have lower volatility

These options offer stability and lower risk.

Another option is a balanced mutual fund. It includes a mix of stocks and bonds. This can cater to moderate risk levels, providing a balanced approach.

Regular portfolio reviews are crucial. Market conditions and personal circumstances change over time. Frequent checks ensure investments remain aligned with one’s risk tolerance.

Consulting with a financial advisor can provide personalized advice. Advisors have tools to assess risk tolerance accurately. They help create a tailored investment plan.

Reviewing Portfolio Performance Based on Risk Tolerance

Regularly reviewing your portfolio is vital. It ensures investments stay aligned with your risk tolerance. Changes in life or the market can affect your comfort level with risk.

Start by comparing your portfolio’s performance with your expectations. Are the returns matching your goals? If not, adjustments might be needed.

Use tables to track performance metrics over time.

| Investment | Expected Return | Actual Return |

|---|---|---|

| Stocks | 8% | 7% |

| Bonds | 3% | 3.5% |

Consider your emotional responses during market fluctuations. If you felt uneasy, your risk tolerance might be lower than initially thought. Adjusting asset allocation can help you feel more secure.

Rebalance your portfolio as needed. This involves buying and selling assets to maintain your desired risk level. Regular evaluations keep your investments on track.

Seek advice from a financial advisor for a comprehensive review. They can suggest changes that align with your updated risk tolerance. Professional guidance can lead to better investment outcomes.

Tools and Techniques to Identify Risk Tolerance

Identifying risk tolerance is a critical step in making informed investment decisions. Several tools can help measure this. These tools provide insights into how much risk you’re willing to take.

Online questionnaires are popular for assessing risk tolerance. These quizzes ask about your reactions to different financial scenarios. They then generate a profile based on your answers.

Financial advisors also offer personalized assessments. They use detailed interviews and advanced software to evaluate your comfort with risk. This tailored approach provides a comprehensive understanding.

- The Risk Tolerance Questionnaire (RTQ): A standard tool used by many advisors.

- Personal Interviews: Direct conversations often reveal more nuanced details.

- Behavioral Analysis Software: Tracks past financial decisions to predict future behavior.

Your investment history can be a useful tool as well. Reviewing past decisions helps identify patterns in your risk behavior. This reflection points out strengths and weaknesses in handling uncertainty.

A clear picture of your risk tolerance directs better investment choices. It aligns investments with both your financial goals and personal comfort levels. Regularly revisiting these tools keeps you on track, ensuring peace of mind along the way.

Evaluation of Financial Risk Tolerance

Evaluating financial risk tolerance is essential for making smart investment choices. One way to assess this is through self-assessment. Consider your comfort level with loss and uncertainty.

Another method involves using score-based questionnaires. These ask about your reactions to market changes and financial losses. The results give a numeric value to your risk tolerance.

Consulting a financial advisor offers a more detailed evaluation. Advisors can provide personalized assessments using advanced tools and techniques. This tailored approach can be more accurate.

| Method | Description | Pros | Cons |

|---|---|---|---|

| Self-Assessment | Personal reflection on risk comfort levels | Simple and cost-free | May lack objectivity |

| Score-Based Questionnaires | Online or paper-based surveys | Quick and user-friendly | Standardized, less personalized |

| Financial Advisor | Professional analysis and advice | Customized and thorough | Costly and time-consuming |

Reviewing past investment experiences can also shed light on your risk tolerance. Analyze how you felt during market ups and downs. This helps to fine-tune your risk profile.

Regularly reassessing your risk tolerance is vital. Life changes and market conditions can alter your comfort levels. Keeping your evaluation current ensures your investments remain suitable.

Finding the Balance: Risk Tolerance and Investment Goals

Balancing risk tolerance and investment goals is key for financial success. Your personal comfort with risk should align with what you want to achieve. This balance ensures your investments serve their purpose.

Short-term goals typically require safer investments. If you need money in the next few years, consider low-risk options. These provide more stability.

Long-term goals often allow for higher risk. Investing in stocks can yield higher returns if you don’t need the money right away. This approach suits retirement plans or saving for a child’s education.

- Short-Term Goals: Emergency funds, vacation savings

- Long-Term Goals: Retirement, college funds

Matching your risk tolerance with your goals helps maintain peace of mind. It prevents unnecessary stress during market fluctuations. You stay focused on your financial objectives.

Regularly review both your risk tolerance and your goals. Life changes can impact both. Keeping them aligned ensures that your investment strategy remains effective.

Frequently Asked Questions

Here are some common questions about risk tolerance in investing. These answers help clarify important aspects to consider.

1. How does age influence risk tolerance?

Age is a significant factor in determining risk tolerance. Younger investors usually have higher risk tolerance because they have more time to recover from losses. They can be more aggressive with their investments, aiming for higher returns over a longer period.

In contrast, older investors may prefer safer investments like bonds or money market funds. As individuals get closer to retirement, protecting capital becomes more crucial than seeking high returns. Adjusting investment strategies over time aligns with evolving financial needs and goals.

2. What role does income play in risk tolerance?

Your income level impacts your ability to handle financial risks. Higher income often allows for more flexibility and a greater capacity to endure potential losses, enabling bolder investment choices.

However, if your income is limited, you might lean towards safer investments to protect what you have. Understanding this balance helps create a sustainable investment strategy that fits your financial situation and long-term objectives.

3. Can emotional resilience affect investment decisions?

Emotional resilience significantly influences how investors manage risk and make decisions during market volatility. Individuals who stay calm under pressure may be better equipped to handle high-risk investments and are less likely to panic-sell during downturns.

Conversely, those prone to anxiety might experience stress when faced with investment losses, leading them to choose safer options. Recognizing one’s emotional limits ensures a balanced approach tailored to personal comfort levels and better long-term outcomes.

4. Is consulting with a financial advisor beneficial for evaluating risk tolerance?

A financial advisor provides valuable insights into assessing your risk tolerance accurately. They use various tools and personalized questionnaires that offer detailed evaluations of your comfort level with different types of investments.

This professional guidance helps align your portfolio with both short-term needs and long-term goals efficiently. Leveraging an advisor’s expertise can enhance decision-making processes and optimize investment strategies tailored to individual circumstances.

5. How do changing life circumstances impact risk tolerance?

Life events such as marriage, having children, or nearing retirement can alter your risk tolerance significantly. New responsibilities often necessitate adjustments in investment strategies to meet evolving financial obligations securely.

An ongoing review of your portfolio ensures it stays aligned with current life stages and goals. Adapting investments proactively helps mitigate risks while striving toward achieving personal and family-oriented objectives effectively.

Understanding Risk Tolerance | Fidelity Investments

Conclusion

Understanding and evaluating risk tolerance is fundamental for informed investing. It aids in aligning investments with individual comfort levels and long-term goals. Recognizing personal factors like age, income, and emotional resilience is crucial for this alignment.

Regular reviews and professional guidance can enhance investment decisions. Life changes and market conditions are inevitable, making ongoing adjustments vital. By continuously monitoring and adapting, investors can optimize their portfolios for better financial outcomes.